/United%20Parcel%20Service%2C%20Inc_%20logo%20magnified-by%20Casimiro%20PT%20via%20Shutterstock.jpg)

United Parcel Service (UPS) shares have tanked in recent sessions as the Iran war pushed oil prices to a high of roughly $120, directly impacting the shipping firm’s substantial fuel costs for both ground and air operations. Following this decline, UPS has its relative strength index (14-day) hovering in the high 20s, indicating oversold conditions that often spark buying momentum in the near term.

At the time of writing, UPS stock is down nearly 18% versus its year-to-date high in mid-February.

Should You Invest in UPS Stock Today?

Long-term investors should consider buying the dip in UPS shares since their fundamental thesis remains intact despite near-term margin pressures.

The company executed a deliberate strategic decision to reduce Amazon (AMZN) volumes by roughly 50% over an 18-month period, which has already resulted in $3.5 billion in cost savings and closure of 93 facilities.

This restructuring demonstrates management discipline and execution capability, evidenced by Q4 results that beat consensus expectations by 2% on revenue and a much larger 8% on earnings.

A lucrative 6.56% dividend yield makes United Parcel Service even more attractive to own in 2026.

UPS Shares Are Inexpensive to Own

The oil-price shock represents a material but temporary headwind rather than a structural threat to the investment thesis.

While every $10 increase in crude adds material costs to UPS’s operating structure, the company has fuel surcharge mechanisms in place that help pass higher costs to customers.

Moreover, at roughly 14x forward earnings, UPS shares remain significantly cheaper than peer FedEx (FDX) as well as their own historical multiple.

It;s also worth mentioning that Atlanta-headquartered United Parcel Service bounced off its 200-day moving average (MA) this week, suggesting bulls haven’t thrown in the towel yet.

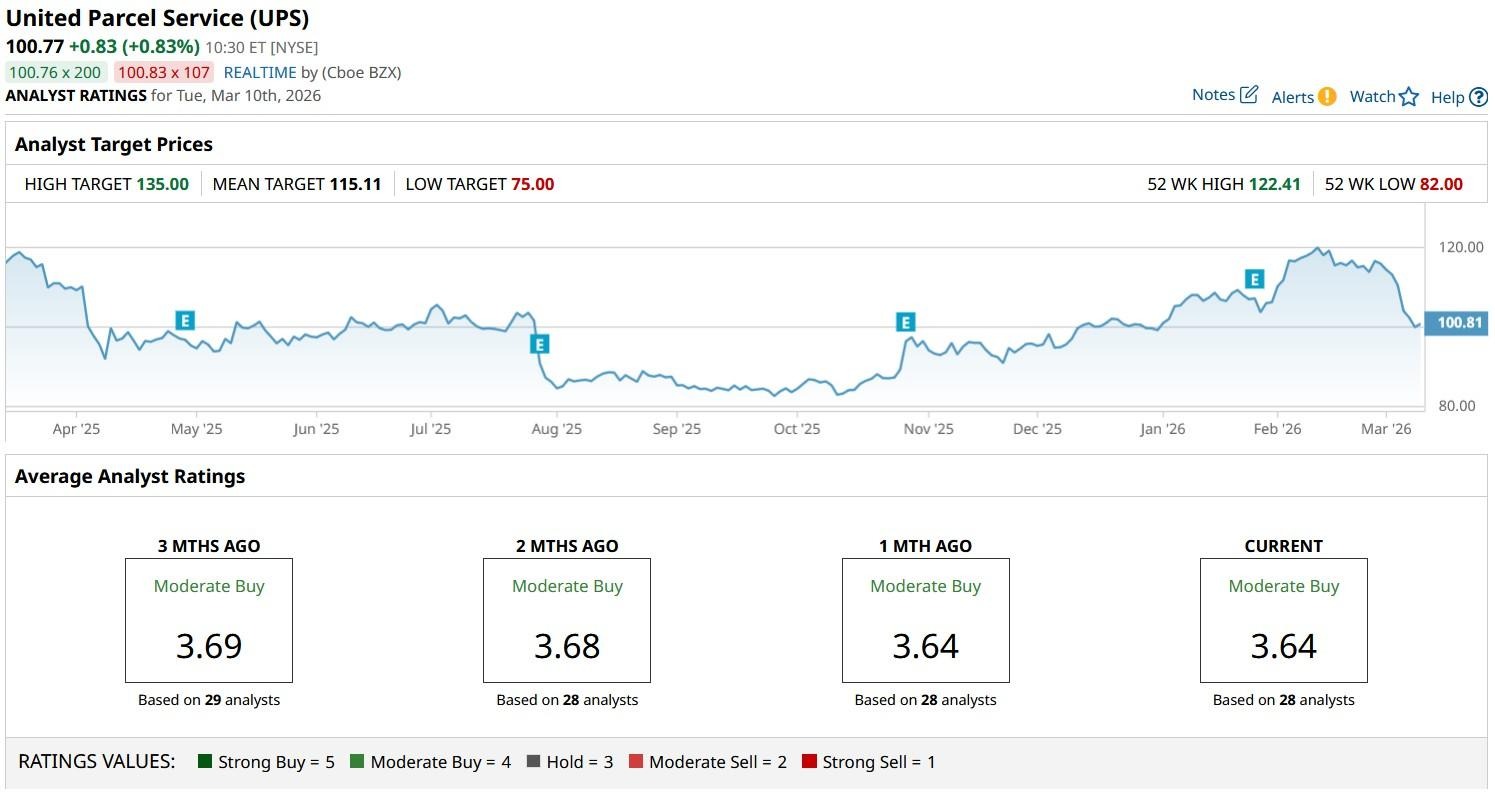

What’s the Consensus Rating on UPS?

Wall Street analysts also recommend buying UPS stock at its current price particularly for the firm’s healthcare logistics segment that’s expected to double the revenue run rate to about $20 billion by late fiscal 2026.

The consensus rating on United Parcel Service sits at “Moderate Buy” currently, with the mean price target of about $115 suggesting potential upside of roughly 15% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)