Cava Group (CAVA) is a fast-casual restaurant chain specializing in Mediterranean cuisine, offering customizable bowls, pitas, salads, dips, spreads, and dressings that blend bold flavors with healthy ingredients. Guests build meals from fresh proteins, grains, veggies, and sauces via digital ordering or in-store. It also sells packaged dips in grocery stores. With over 340 locations, Cava emphasizes hospitality, sustainability, and quick service, competing with Chipotle in the health-focused segment.

Founded in 2006, Cava Group went public in 2023 and is headquartered in Washington, D.C. It operates exclusively in the United States across 25+ states and D.C., with no international presence yet.

Cava Group Stock

Cava's stock has rallied sharply, trading near $80 after strong Q4 results. It's up 5% over the past five days, soaring 18% in the last month from $61 lows, 53% in three months, and 25% in six months. Year-to-date (YTD) gains stand at 38%, with 52-week returns at 1% from $43 lows despite a 20% pullback from $101 highs.

Versus the Russell 1000 (IWB), flat in five days and down 2% monthly, down 1% in six months but up 24% in 52 weeks. CAVA stock has handily outperformed across all periods (except for the 52-week period), driven by traffic growth and expansion in fast-casual dining.

Cava Group Results

Cava's Q4 revenue hit $272.8 million (+21.2% year-over-year, beating the $268 million estimate by 1.8%), driven by 87 net new restaurants, modest 0.5% same-store sales (traffic down 1.4%, offset by pricing/mix), and digital mix at 38.9%. GAAP EPS $0.04 (net income $4.9 million), adjusted EPS $0.22 (+29% vs. $0.17 est.). Full-year revenue topped $1.17 billion (+22.5% YoY, first $1 billion milestone), same-store +4%.

Margins are resilient, with restaurant-level profit at $58.3 million (21.4% margin, +15.7% YoY), adj. EBITDA $25.8 million (9.4% margin, +2.6% YoY). Full-year: restaurant margin 24.4% (-60 bps YoY on food costs), adj. EBITDA $152.8 million (+21% YoY, 13.1% margin). AUV $2.9 million (+1%), cash $483 million, FCF $26.1 million yearly (adj. net income $63.7 million). And opened 52 stores in the Q4 period.

Outlook is also strong: Q1 revenue $305-310 million (~12% YoY, beat est.), comps 6-8%, restaurant margin ~24.5%. FY2026: comps 7%, 64-68 new stores, adj. EBITDA margin expansion. CEO Brett Schulman highlighted traffic momentum and digital scale.

Cava Soars on Results

CAVA stock soared 26% after surprise Q4 same-store sales growth, powered largely by menu price hikes. The Mediterranean fast-casual chain exceeded earnings forecasts and guided for 2026 sales growth, achieving $1 billion in full-year revenue for the first time.

CFO Tricia Tolivar highlighted Cava's "bridge" in the K-shaped economy, staying accessible with minimal price increases while boosting value perception. Younger consumer traffic firmed up in Q4, with top performance in lower-income markets. CEO Brett Schulman credited bold flavors, healthy options, and hospitality for resonating with discerning diners.

For 2026, Cava plans 74-76 new restaurants and 3-5% same-store sales growth, eyeing strong results from new menu items like salmon.

Should You Bet on CAVA Stock?

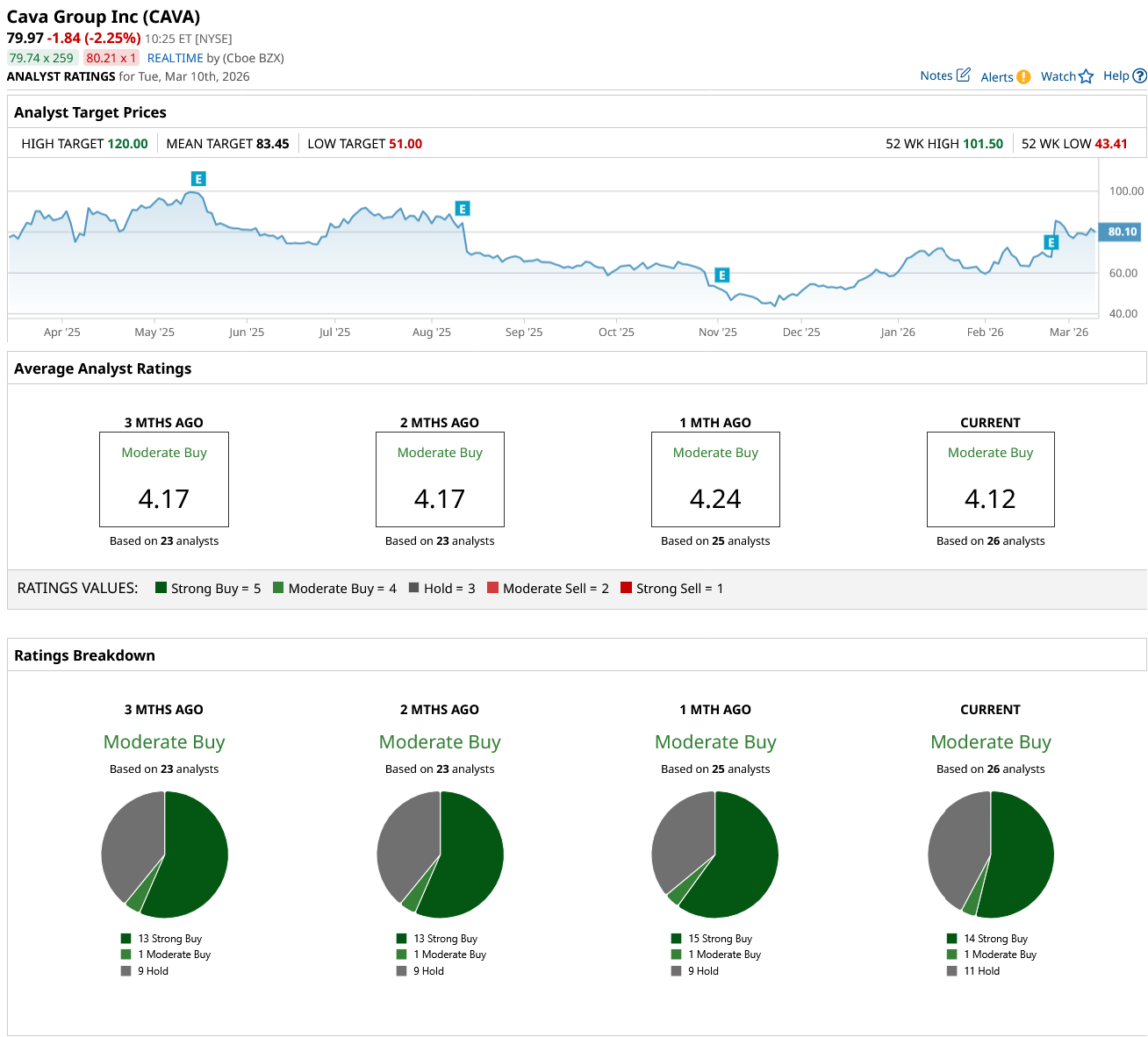

Cava Group has market support with a consensus “Moderate Buy” rating and a mean price target of $83.45, reflecting an upside potential of 4% from the current market rate.

CAVA stock has been rated by 26 analysts with 14 “Strong Buy” ratings, one “Moderate Buy” rating, and 11 “Hold” ratings for the restaurant chain.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)