With a market cap of $34.8 billion, Kimberly-Clark Corporation (KMB) is a U.S.-based manufacturer and marketer of personal care and household products. The company operates through two main segments: North America and International Personal Care, offering products such as diapers, baby wipes, feminine and incontinence care items, and tissue products under brands like Huggies, Kleenex, Kotex, and Scott.

Companies valued at $10 billion or more are generally classified as “large-cap” stocks, and Kimberly-Clark fits this criterion perfectly. It sells its products to retailers, distributors, businesses, and e-commerce channels, serving both household consumers and professional facilities worldwide.

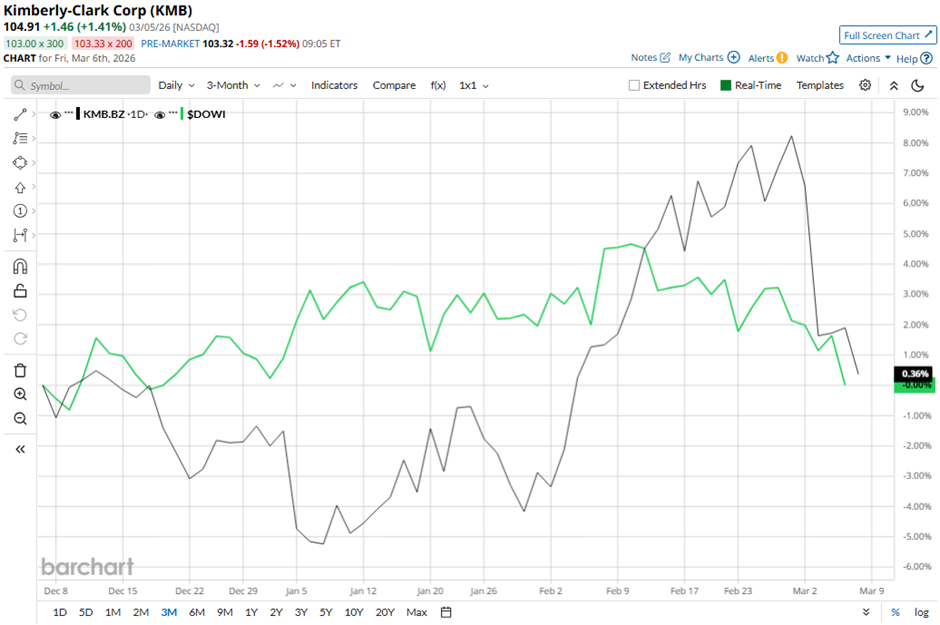

Shares of the Dallas, Texas-based company pulled back 32.2% from its 52-week high of $150.45. Shares of Kimberly-Clark have risen marginally over the past three months, outpacing the Dow Jones Industrials Average's ($DOWI) unchanged performance over the same time frame.

KMB stock is up 2.5% on a YTD basis, outperforming DOWI’s marginal decline. However, in the longer term, shares of the consumer products company have dipped 27.4% over the past 52 weeks, lagging behind Dow Jones' 11.5% increase over the same time frame.

Despite a few fluctuations, the stock has been trading below its 50-day and 200-day moving averages since late April 2025.

Kimberly-Clark reported strong Q4 2025 results on Jan. 27, including adjusted EPS of $1.86, up 24% year-over-year, and adjusted operating profit of $629 million, up 13.1%. The company also posted organic sales growth of 2.1% in the quarter, driven by 3% volume-plus-mix growth, highlighting solid demand for its products. Additionally, management issued a positive 2026 outlook, expecting mid-to-high single-digit adjusted operating profit growth and double-digit adjusted EPS growth from continuing operations. However, the stock fell marginally on that day.

In comparison, rival The Procter & Gamble Company (PG) has outpaced KMB stock. Shares of Procter & Gamble have gained 7.4% on a YTD basis and decreased 11.9% over the past 52 weeks.

Despite the stock’s weak performance over the past year, analysts are moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 17 analysts covering the stock, and the mean price target of $119.12 is a premium of 13.5% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)