PepsiCo (PEP) is hardly an unknown name in the market. Recognized mostly for its beverages since 1965, the company has now evolved into a food and beverage giant, owning some of the world’s most recognizable brands, from Pepsi and Gatorade to Lay’s, Doritos, and Quaker.

But for many investors, PepsiCo's biggest appeal is not just its brands but its status as a Dividend King. This is a rare title reserved for businesses that have raised their dividends for at least 50-straight years. PepsiCo has now increased its payout for 54 consecutive years, placing it among the top income stocks.

This dividend track record is precisely why PEP stock deserves a closer look ahead of its July 9 earnings report.

PepsiCo’s International Business Remains the Stabilizer

In a market where plenty of hyped companies deliver short bursts of growth, PepsiCo stands out as a proven cash-return machine. This has been possible because of consumers' loyalty to the brand, which has kept earnings and cash flow stable enough to cover its dividend payouts.

In the first quarter, organic sales increased 2.6% year-over-year (YOY) while net revenue rose 8.5% to $19.4 billion. Core EPS increased 9% to $1.61 per share. CEO Ramon Laguarta highlighted progress across the business, particularly in international markets, beverages, and North Americn Foods. Notably, PepsiCo Foods North America (PFNA), comprising of the Frito-Lay U.S. snack business, showed real improvement. The business has been under pressure over the last few quarters due to weaker demand, affordability concerns, and uneven category performance. However, it delivered 2% volume growth in Q1 as well as 4% unit growth over the prior-year period.

The improvement happened because PepsiCo added more consumer value in core brands, gained shelf space, restaged brands like Lay's and Tostitos, and shifted funds to away-from-home channels. PepsiCo’s international business continues to do a lot of heavy lifting to compensate for the other segments. Management stated that despite the Iran war, there wasn’t much impact on demand. In fact, PepsiCo is even benefiting from having a stronger supply chain than competitors, particularly in the food business in some global markets.

Dividends Are the Heart of the Buy Case

The Q1 numbers show a business that is still growing, maintaining profitability, and still generating enough cash flow to keep investing in its brands while returning to shareholders. Amid geopolitical uncertainty, potential inflation pressure, and ever-changing competitive dynamics in snacks and beverages, this is a positive sign. Management expects organic revenue growth of 2% to 4% and core EPS growth of 4% to 6% in 2026. The company even expects to generate 80% of net income as free cash flow and return $8.9 billion to shareholders in the form of dividends ($7.9 billion) and share buybacks ($1 billion).

Interestingly, PepsiCo is not promising a record-breaking year of strong growth but rather a manageable one, supported by scale, hedging, supply-chain redundancy, and productivity gains. This is what makes PEP stock attractive as a defensive stock. Plus, PepsiCo pays an attractive forward yield of 4.17%, much higher than the consumer staples sector and market average. While slightly high, its forward payout ratio of 68.56% remains manageable.

Is PepsiCo a Buy Before July 9?

The upcoming Q2 report may not reveal some outstanding numbers, but it may justify PepsiCo’s place as a reliable income stock with steady operating momentum. For long-term investors who look at PepsiCo mostly as a dividend compounder rather than a hyper-growth tech story, PEP stock remains a buy-and-hold.

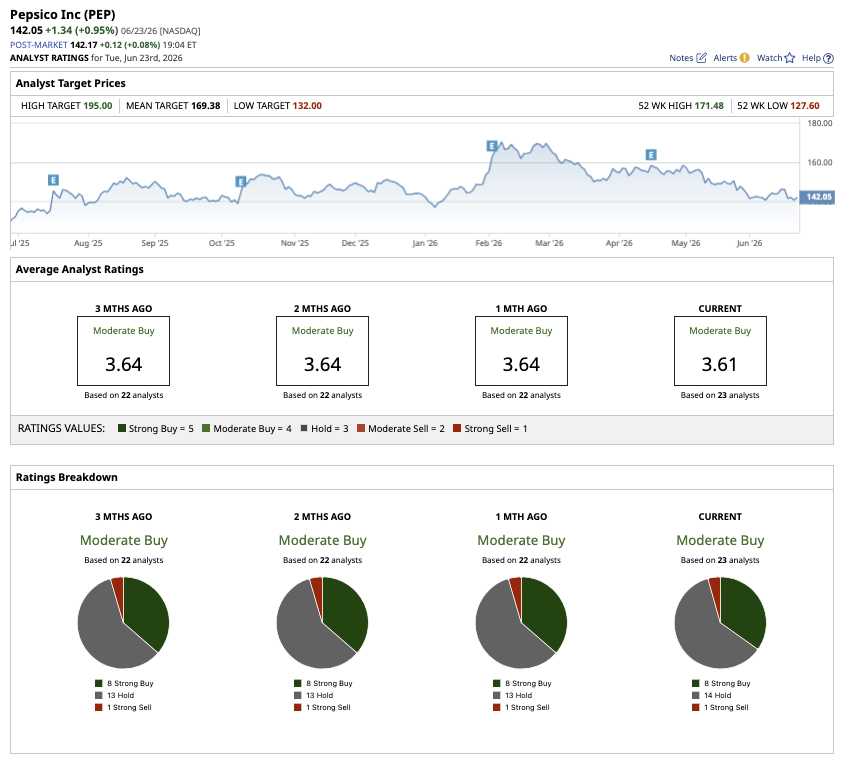

Analysts overall give the stock a consensus “Moderate Buy" rating. Out of the 23 analysts covering PEP stock, eight have a “Strong Buy" rating, 14 suggest a “Hold,” and one rates it as a “Strong Sell." The mean target price of $169.38 implies potential upside of 21% from current levels. The Street-high price estimate for PEP stock is $195, implying potential upside of 39% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)