Have recent events - the US-Iran “War”, strength of the Brazilian real, etc. - broken the sugar market out of its long-term downtrend?

If sugar is to see a change in trend it will likely be due to funds starting to cover some of the record large short futures position.

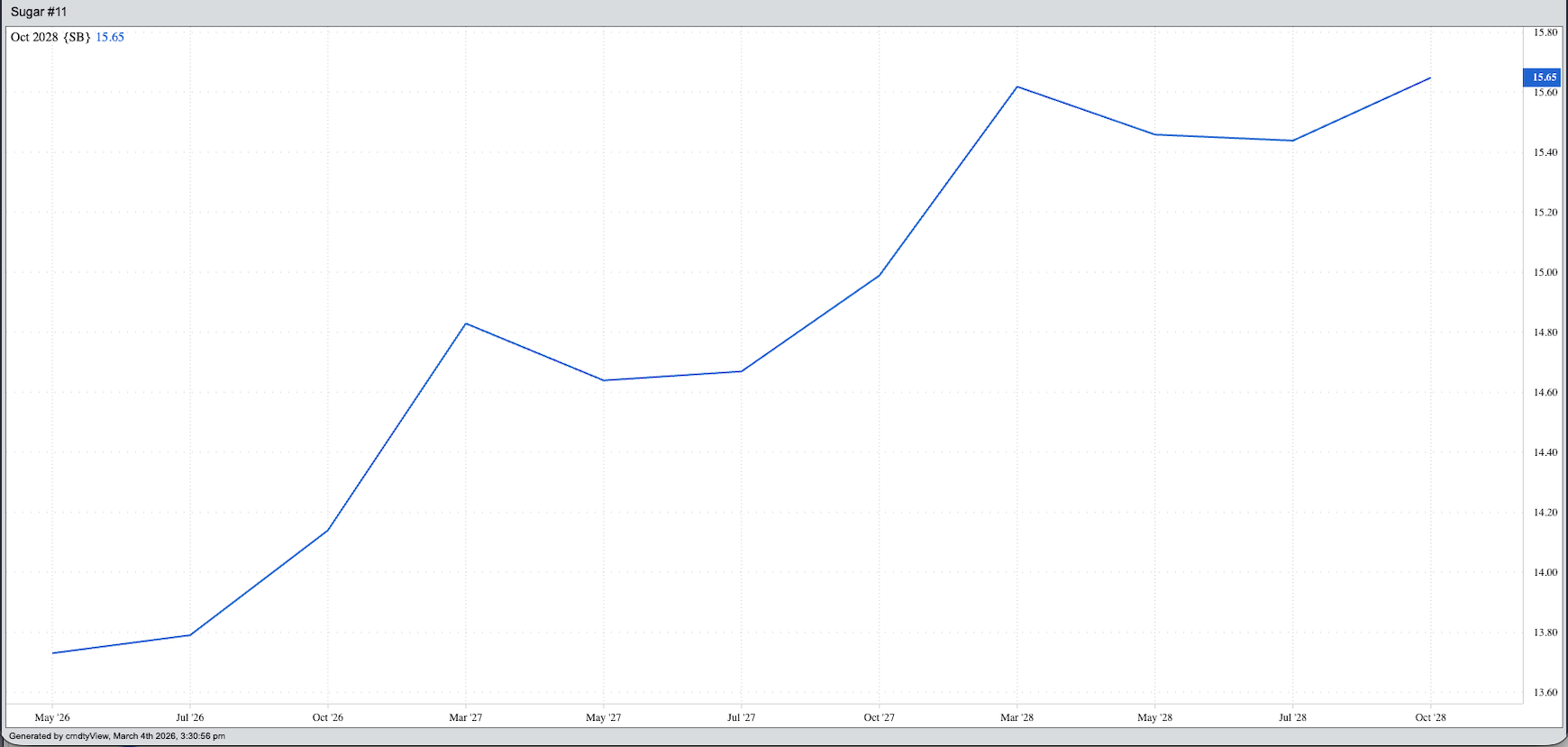

Fundamentally, the market's forward curve remains in contango, indicating no short supply scare at this time.

Earlier this week, a long-time friend in the media reached out with an email asking about markets tied to the US-Iran War. Knowing my friend, I could read the fatigue in her email, “I haven’t had time to look at much else besides oil and gold, but what’s all this I’m hearing about sugar prices going up because of the US-Iran conflict?” She followed with, “Do you have any insight into why sugar prices have rallied? Is there a supply shortage? Or is the Middle East of particular concern when it comes to sugar supply and demand?”

As always, I thanked my friend for breaking me out of the rut I get myself in with corn/soybeans and gold/silver. It’s refreshing to think about other markets occasionally, even if gold and crude oil are the two main stories in commodities at this point.

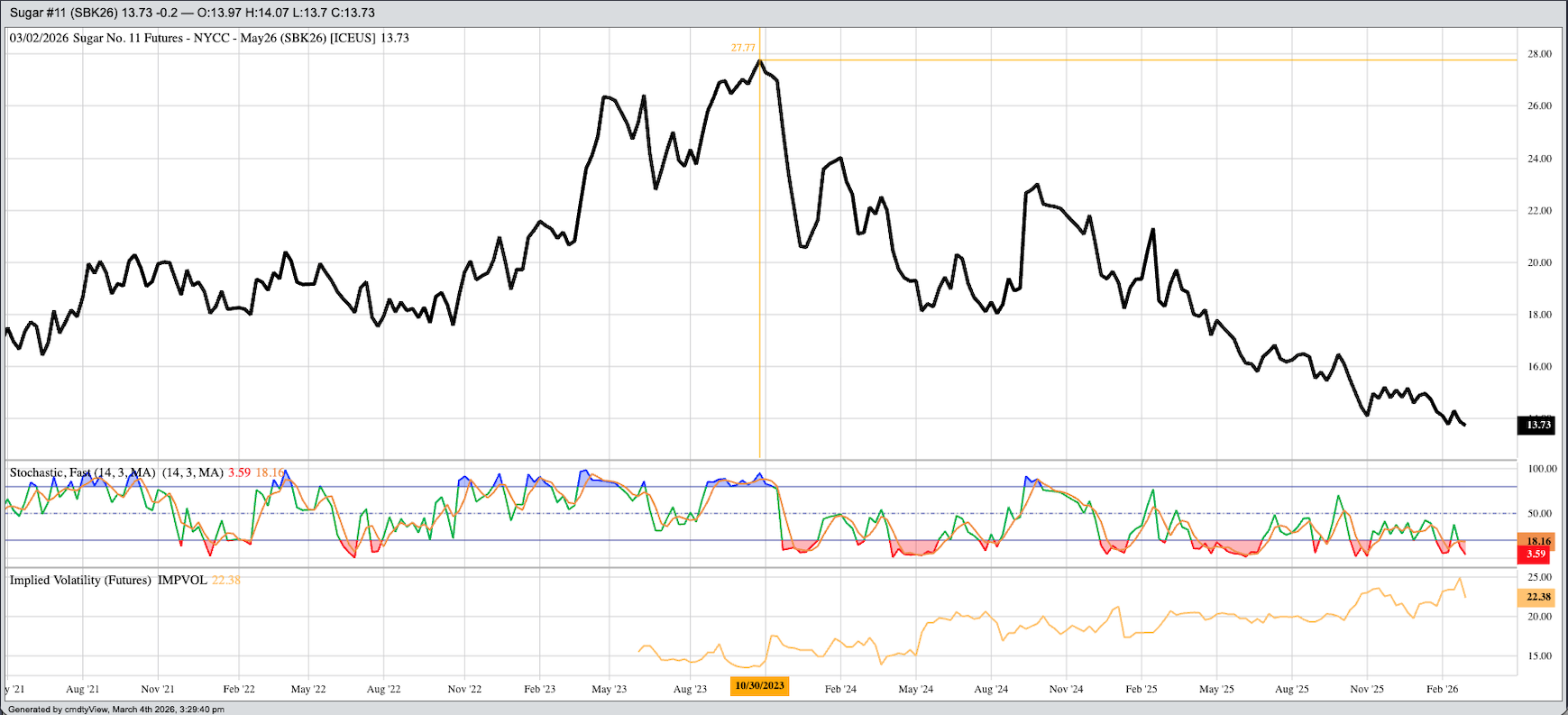

Let’s put the pieces of the sugar market together and see what we see, staring with the weekly close-only chart for the nearby No. 11 futures (SBK26) chart. Let’s block out all the noise and focus on one thing: The trend – price direction over time. What I see is as clear of a downtrend as we will find almost anywhere. It’s interesting to note the market posted a high weekly close the week of Halloween 2023, the nearby futures contract priced at 27.77 (cents per pound). As of the close on Wednesday, March 4, 2026, the nearby contract is priced at 13.73 meaning the market has lost just over 50% of its value.

Has the market rallied since the US launched its against Iran at the end of February? For the week the nearby May contract is down 0.16. As far as I’m concerned, the trend of the market is still down, fitting with Newton’s First Law of Motion applied to markets: A trending market will stay in that trend until acted upon by an outside force. And that force is usually the flow of noncommercial money.

The most recent CFTC Commitments of Traders report (legacy, futures only) showed a noncommercial net-short futures position of 246,123 contracts as of Tuesday, February 24. This was a decrease of 7,469 contracts from the previous week record net-short futures position of 253,592 contracts. For the record, the noncommercial futures position the week of October 30, 2023, was a net-long of 213,589 contracts meaning funds have flipped their position by 467,181 contracts. Almost a half-million contracts. That is substantial.

Within these numbers, funds built a new record large short futures position of 429,569 as of February 24. This opens the gates to a possible Poseidon Predicament – when everyone is on the same side of the boat, the boat tends to roll over. If the sugar market starts to rally, I don’t think it is going to be based on fundamentals but rather funds closing out positions and looking for other opportunities.

Since I mentioned it, what is the fundamental situation of sugar? First and foremost, Brazil is the world’s largest sugar producer and exporter. We know by watching three other markets that Brazil plays a key role in – coffee, orange juice, and of course soybeans – weather across much of the main growing areas was fine during 2025 and early 2026. The price of coffee has plunged since the latest harvest, as is usual with a short-supply market, and orange juice tanked from September 2024 through November 2025. And while the jury is still out on the soybean market, the price of Brazilian soybeans at port are $47.25 cents per metric ton less than US soybeans at the Port of New Orleans.

But what about sugar’s fundamentals? The market’s forward curve is showing a general contango from the May 2026 contract through the March 2027 issue, then through the March 2028 contract and so on. (Trade volume gets a bit light in the far deferred contracts.) Given the forward curve, I do not see a sudden supply scare in relation to demand. Could it happen? Of course. That’s what makes markets fun.

The bottom line is sugar has not seen a rally, due to the US-Iran conflict or other factors. But it could if funds start covering the short futures position. Again, as Newton told us, that will be the change in force that sets a new trend. How far it might go will depend on if a change occurs in real fundamentals.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)