Volatile markets often make investors seek reliable investment opportunities. And what is more reliable than a dividend stock, particularly those that consistently pay dividends regardless of market cycles? This consistency reveals a business' stability and commitment to reward shareholders over the long run.

Let’s look at three such dividend stocks investors can confidently add to their portfolio in March.

Dividend Stock #1: Verizon Communications (VZ)

Verizon Communications (VZ) is a telecom giant, valued at roughly $206.2 billion. It is one of the largest wireless carriers in the U.S., providing mobile services, broadband connectivity, and enterprise networking solutions. Its massive scale ensures stable earnings and cash flows, allowing it to be a reliable dividend payer. This reliability is depicted in its 20-year track record of paying and increasing dividends consistently. In fact, it is closer to joining the “Dividend Aristocrats,” which are companies that have hiked dividends for 25 years in a row. Management boasted about the company’s “ironclad” commitment to shareholder returns. Recently, it increased its annual dividend by 2.5%

Additionally, it offers an appealing yield of 5.5%, higher than the S&P 500 ($SPX) average. But more importantly, its payout ratio measures how much of its earnings the company decides to distribute to shareholders. This ratio sits comfortably at 57%, which is neither very high nor low, giving Verizon enough breathing room to pay debts, reinvest in the business, and potentially continue modest annual dividend increases.

Management has guided for an annual free cash flow of $21.5 billion in 2026, which also marks the highest free cash flow Verizon has generated since 2020. This is more than enough to comfortably fund dividend payments while maintaining operational flexibility. While Verizon may not be a high-growth story, it remains a reliable and high-yield source of passive income.

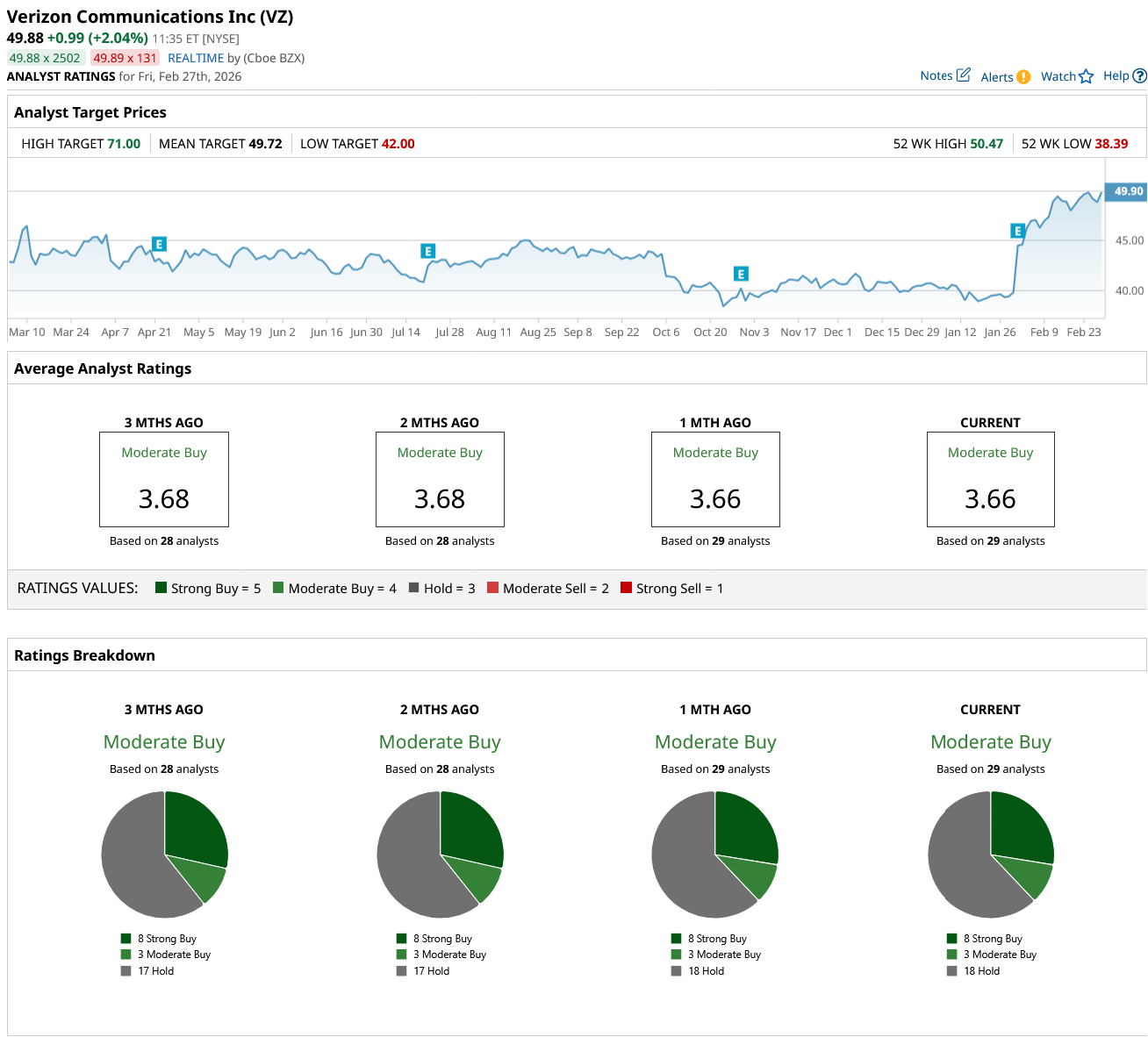

Overall, VZ stock has earned a “Moderate Buy” recommendation on Wall Street. Of the 29 analysts that cover the stock, eight rate it a “Strong Buy,” three recommend a “Moderate Buy,” and 18 suggest a “Hold.” The stock is currently trading almost exactly at its average target price of $49.72. But its Street-high estimate of $71 implies VZ stock can go as high as 42% in the next 12 months.

Dividend Stock #2: NextEra Energy (NEE)

Florida-based NextEra Energy (NEE) is one of North America’s largest electricity providers, serving millions of customers through regulated utilities and a growing clean-energy business. It pays a forward dividend yield of 2.7%, lower than the utilities sector average of 3.7%. But NextEra Energy has a long history of rewarding shareholders with regular dividends. It has already earned the title of a Dividend Aristocrat by paying and increasing dividends for the past three decades.

Its forward dividend payout ratio of 61% is backed by consistent cash flows. It is also sustainable, as the company has committed to increasing its dividends at approximately 10% annually through 2026 and then 6% each year until 2028. NextEra Energy's diverse business offers stability from regulated electricity distribution as well as growth possibilities from the renewable energy segment. This dynamic has enabled the company to generate consistent cash flows that sustain its dividends.

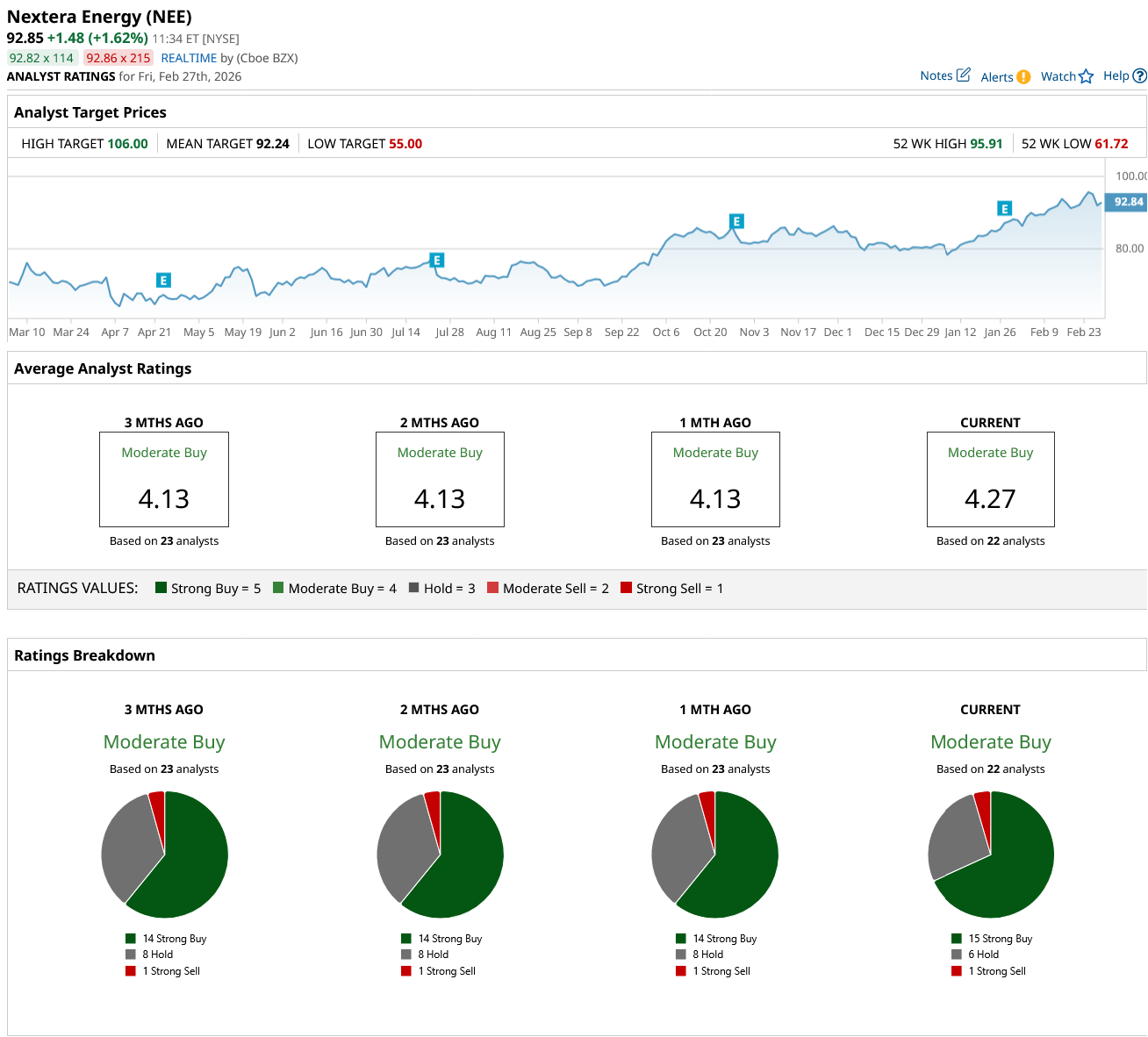

Overall, Wall Street rates NEE stock as a “Moderate Buy.” Of the 22 analysts that cover the stock, 15 rate it a “Strong Buy,” six suggest a “Hold,” and one suggests a “Strong Sell.” The stock is trading close to its average target price of $92.24. But its Street-high estimate of $106 further implies NEE stock can go as high as 14% in the next 12 months.

Dividend Stock #3: Rexford Industrial (REXR)

Rexford Industrial (REXR) is a Los Angeles-based real estate investment trust (REIT) that specializes in owning and managing industrial properties across Southern California’s high-demand infill markets. Rexford pays a slightly higher yield of 4.6%, compared to the real estate sector average of 4.4%. For a REIT, funds from operations (FFO) play a similar role as net earnings for non-REITs and can be used to determine how much of the FFO can be paid out as dividends. And REITs are legally bound to distribute 90% of their taxable income to shareholders.

As long as Rexford consistently increases its FFO, it should be able to maintain its FFO payout ratio of 73%, which is slightly on the higher side. In 2025, FFO increased by 9.2% to $558.6 million and paid out $103 million in dividends. Rexford also increased its quarterly dividends by 1.2% for 2026 to $0.435 per share. The company has increased its dividends for the last 12 years in a row.

Rexford’s footprint is focused on Southern California, which is one of the nation’s most supply-constrained industrial regions, giving it pricing power. This has helped Rexford maintain consistent occupancy and rent growth trends, which are critical for long-term cash flow and dividend payouts.

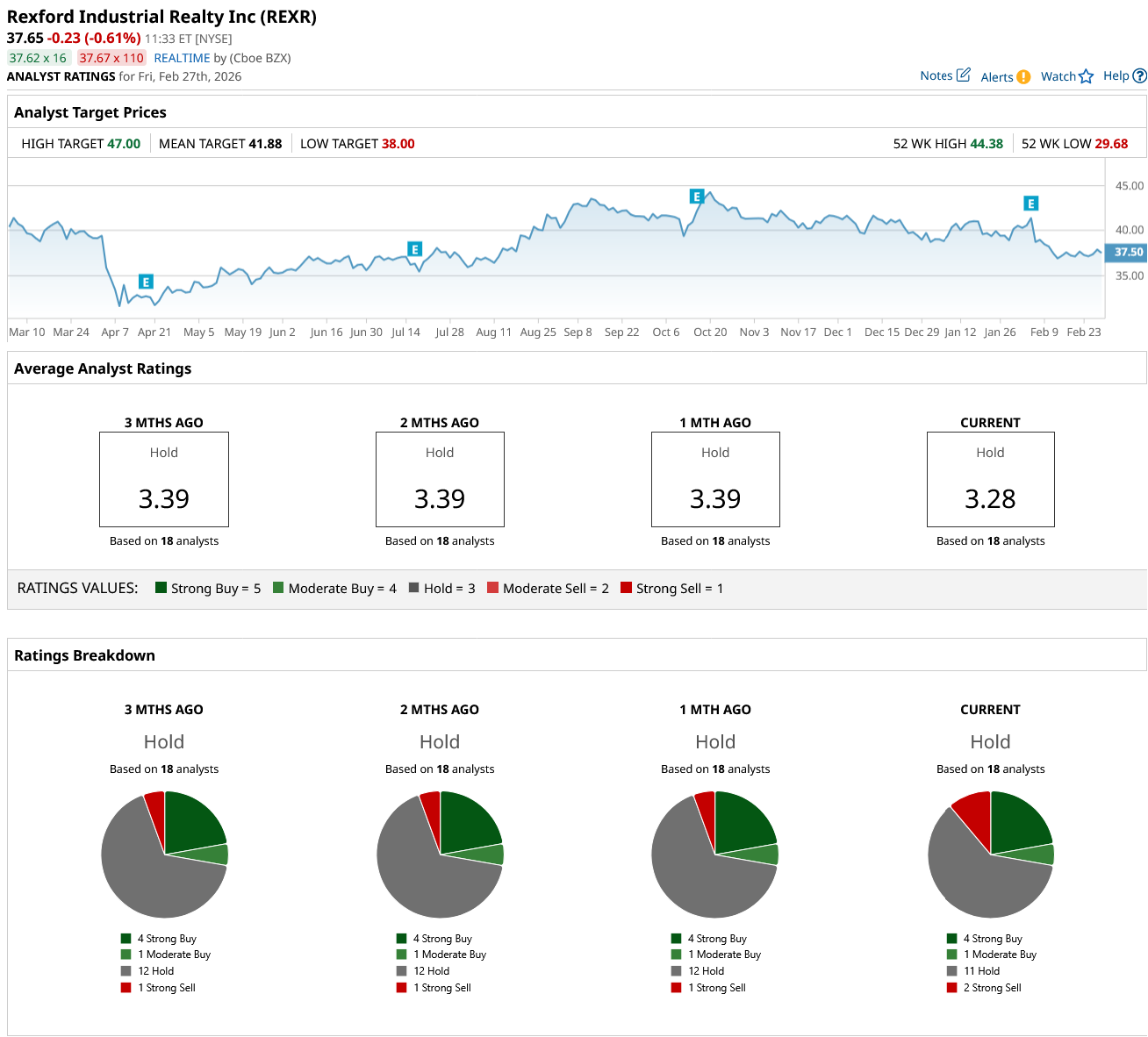

On Wall Street, overall REXR stock is rated as a “Moderate Buy.” Out of the 18 analysts who cover REXR stock, four rate it a "Strong Buy," one recommends a “Moderate Buy,” 11 rate it a “Hold,” and two suggest a “Strong Sell.” Its average price target of $41.88 suggests that the stock can increase by 11% over current levels. However, its high target price of $52 implies an upside potential of 38% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)