/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

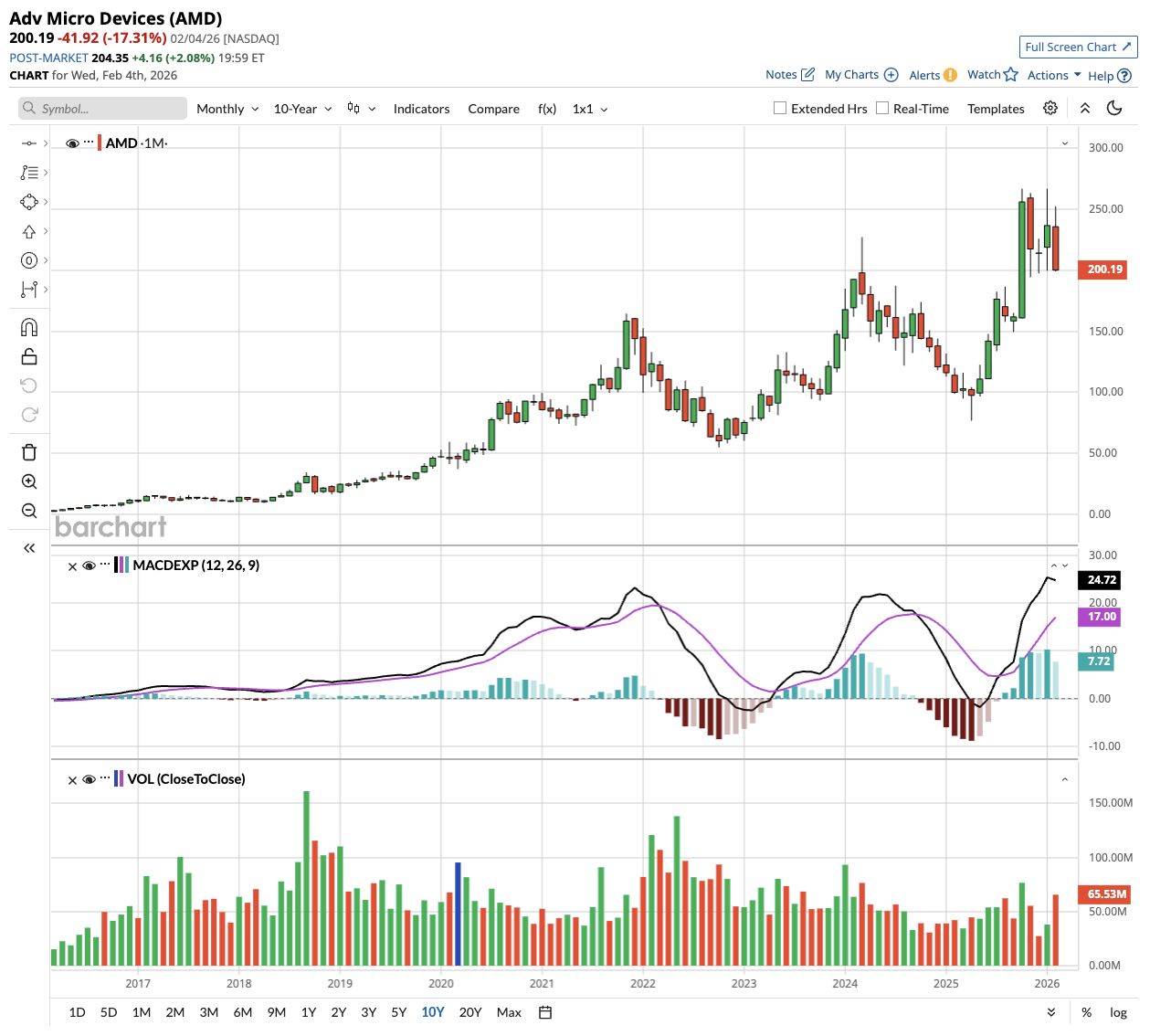

AMD's (AMD) stock just took a beating, dropping 17% in its worst session since 2017. But CEO Lisa Su says the pullback doesn't reflect the company’s widening AI moat.

The chipmaker posted strong fourth-quarter results, with revenue of $10.27 billion and earnings per share of $1.53, both beating Wall Street expectations. Yet investors sold off AMD stock after Q1 guidance of $9.8 billion fell short of some analysts' sky-high expectations.

So what's really going on here, and should investors view this dip as a buying opportunity ahead of the crucial MI400 launch?

The China Revenue Wildcard

Part of the disappointment stems from an unexpected twist in AMD's numbers. The company disclosed $390 million in fourth-quarter sales to China from its MI308 chips, revenue that wasn't baked into Street estimates.

Strip that out, and the beat looks a lot less impressive. AMD expects another $100 million from China in the current quarter but isn't forecasting additional revenue beyond that. It's a cautious stance given the unpredictable nature of U.S. export controls, but it also means the company's underlying growth drivers need to carry more weight.

Data Center Growth Remains the Real Story

Despite the stock selloff, AMD's data center segment delivered impressive results. Revenue jumped 39% year-over-year (YoY) to $5.4 billion, driven by both EPYC server processors and Instinct AI GPUs.

What's interesting is the strength in server CPUs, which Su says are "going gangbusters." Hyperscalers are expanding their infrastructure to meet surging demand for cloud services and AI, while enterprises are modernizing their data centers to support new AI workflows.

The AI boom isn't just about graphics processors anymore. As AI models and agentic workflows proliferate, high-performance CPUs will soon become critical components of infrastructure. AMD's EPYC processors are gaining serious traction here, with server CPU revenue actually growing sequentially from Q4 into Q1 despite typical seasonal weakness.

The MI400 Series: AMD's Critical Inflection Point

Su called 2026 "a very important year" for AMD, describing the upcoming MI400 launch as a genuine inflection point for the business.

The MI355, which ramped up in the fourth quarter, performed well and will continue to grow in the first half of 2026. But the real game-changer is the MI450, which begins shipping in the third quarter and ramps up significantly in the fourth quarter heading into 2027.

AMD has locked in some major commitments here:

- The company's partnership with OpenAI calls for deploying 6 gigawatts of Instinct GPUs over multiple years, starting with a 1-gigawatt rollout in the second half of 2026.

- Oracle also plans to deploy 50,000 AMD AI chips beginning later this year.

Su emphasized that AMD is in "active discussions" with multiple customers beyond OpenAI for multi-gigawatt, multi-year deployments, starting with the Helios platform and MI450 later this year.

Expanding the Portfolio for Different Workloads

AMD isn't putting all its eggs in one basket. The MI400 series includes multiple variants designed for different use cases:

- MI455X and Helios for AI superclusters.

- MI430X for high-performance computing and sovereign AI.

- MI440X servers for enterprise customers needing leadership training and inference in a more compact eight-GPU solution.

This approach addresses a crucial reality: there's no one-size-fits-all solution in AI infrastructure. Different customers have different requirements, and AMD is positioning itself to serve the full spectrum.

The Long-Term Growth Path Looks Solid

AMD reiterated its ambitious long-term targets at its November Financial Analyst Day, including revenue growth exceeding 35% annually over the next three to five years.

The company expects to scale its data center AI business to tens of billions in annual revenue by 2027, with data center segment revenue growing more than 60% annually over the next three to five years.

Susquehanna analyst Chris Rolland noted that while expectations were "sky high" going into the quarter, the underlying fundamentals remain strong. The company is hinting at multi-gigawatt contracts in the pipeline, and data center demand continues to accelerate.

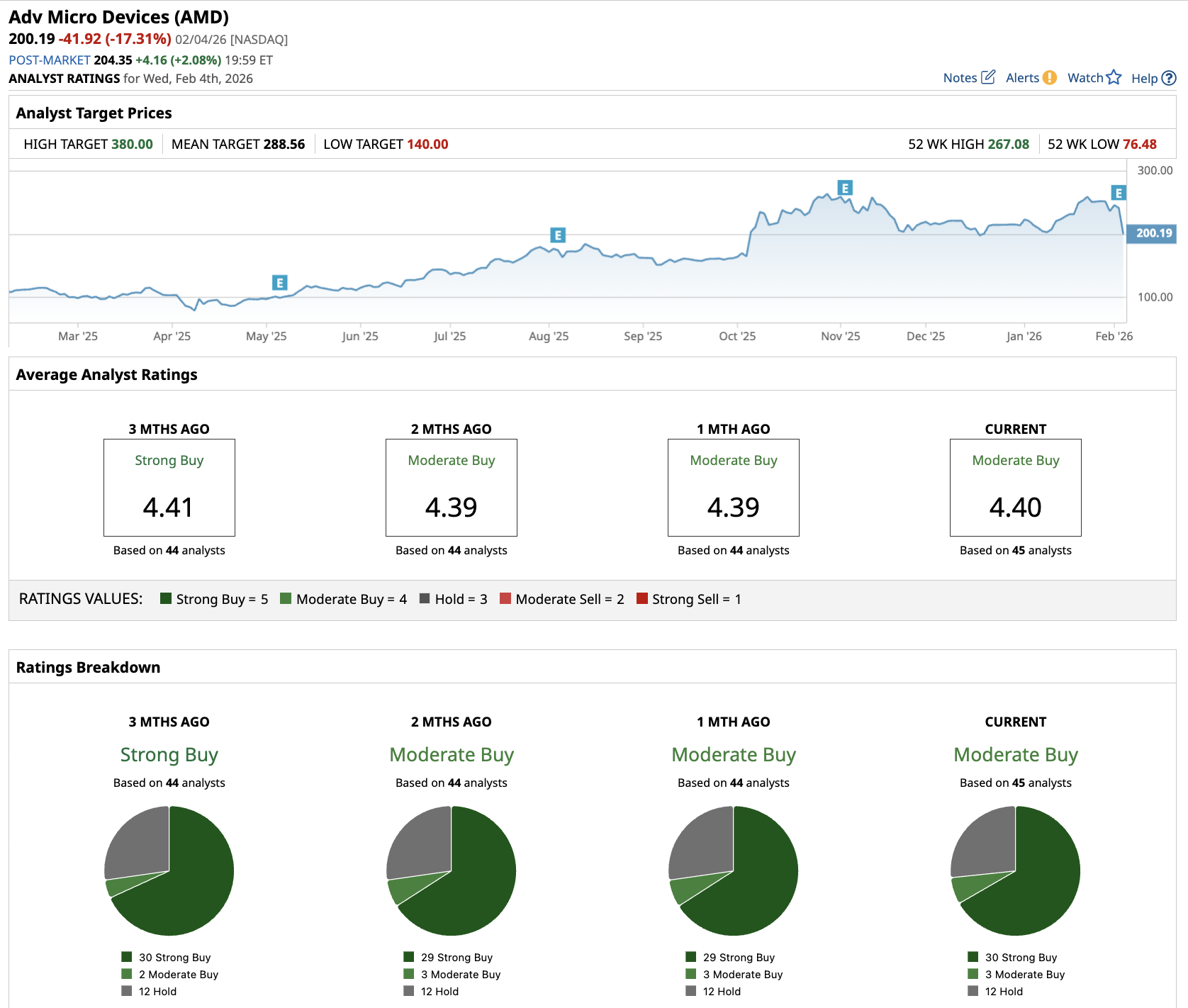

Out of the 45 analysts covering AMD stock, 30 recommend “Strong Buy,” three recommend “Moderate Buy,” and 12 recommend “Hold.” The average AMD stock price target is $289, above the current price of about $200.

The Bottom Line on AMD Stock

AMD's stock reaction appears to be a classic case of short-term disappointment obscuring longer-term potential. Yes, the first-quarter guide came in below some aggressive estimates. But the company is executing well across its product portfolio, gaining server CPU share, and positioning itself for a major ramp in the second half with the MI400 series.

For investors willing to look past near-term volatility, the current pullback might offer an attractive entry point ahead of what Su describes as an inflection point for the business. The MI400 launch represents AMD's best shot yet at capturing meaningful share in the booming AI chip market, and the groundwork appears to be in place for a strong second-half ramp.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)