Investors seeking dependable passive income that keeps growing over time could consider high-yield dividend stocks with the ability to increase their distributions year after year. The reliable dividend payers and growers are backed by resilient business models generating steady earnings and cash flows across economic cycles.

In this context, Enbridge (ENB) is a top choice for passive income investors. The company has a proven history of dividend payments and growth. Moreover, its forward annual dividend of $2.85 per share yields 5.4%. Further, Enbridge is well-positioned to continue growing its dividends year after year.

Enbridge Raised Its Dividend for 31 Years

Enbridge is an attractive stock offering a high yield and a stress-free dividend. It is a diversified energy infrastructure company that has increased its dividend for decades. It operates oil pipelines and terminals across Canada and the U.S., transports and stores natural gas, operates gas utilities serving homes and businesses, and invests in renewable energy projects, including wind, solar, and geothermal facilities in North America and Europe.

Supporting Enbridge’s payouts are its high-quality assets backed by long-term contracts, regulated cost-of-service tolling structures, power purchase agreements (PPAs), and other low-risk commercial arrangements. This defensive operating structure has enabled Enbridge to generate consistent, resilient cash flow across multiple commodity cycles, economic conditions, and geopolitical conditions. As a result, Enbridge generates steady earnings and distributable cash flow and has increased its dividend for 31 consecutive years.

Enbridge’s Dividend to Grow By 5% Annually

Looking ahead, Enbridge’s diversified, high-quality assets position it well to continue growing its dividend. Notably, in Liquids Pipelines, the company’s network remains a critical link between production basins and refinery hubs, supporting high system utilization. In Gas Transmission, Enbridge is expanding pipelines and storage capacity to meet structural demand drivers, including LNG export growth, gas-fired power generation, data center expansion, coal-to-gas switching, electrification, and the reshoring of industrial activity. These investments are backed by regulated or contracted frameworks, supporting the predictable returns.

The Gas Distribution and Storage segment is similarly positioned to benefit from rising power demand and infrastructure modernization. As electricity consumption increases, natural gas remains an essential reliability backstop for power generation. Enbridge’s regulated utility model in this segment offers secured growth opportunities with comparatively low business risk.

Meanwhile, the Renewable Power Generation business provides exposure to long-term decarbonization trends. Through disciplined capital allocation and selective development in supportive jurisdictions, Enbridge continues to add renewable capacity under contract, complementing its conventional infrastructure footprint without materially increasing risk.

Over the next five years, Enbridge expects to return approximately $40 billion to $45 billion (in Canadian dollars) to shareholders through dividends. ENB’s targeted payout ratio of 60% to 70% of DCF is sustainable and will help the company to pay dividends and retain capital for growth. With a multi-billion dollar secure backlog supporting its growth in the coming years, management anticipates annual dividend growth of about 5% through 2030.

The Bottom Line on ENB Stock

Enbridge is a reliable dividend grower offering a high and sustainable yield. Its 5.4% forward yield is supported by a diversified portfolio of regulated and contracted energy infrastructure assets that generate predictable DCF across commodity cycles. The company’s 31-year track record of consecutive dividend increases shows the resilience of its business model and disciplined capital allocation.

Looking ahead, structural demand drivers across liquids pipelines, natural gas transmission, regulated utilities, and renewables offer growth opportunities without materially increasing risk. A solid secured capital backlog, a targeted 60%–70% DCF payout ratio, and projected annual dividend growth of approximately 5% through 2030 make ENB a must-have stock for income that will keep growing.

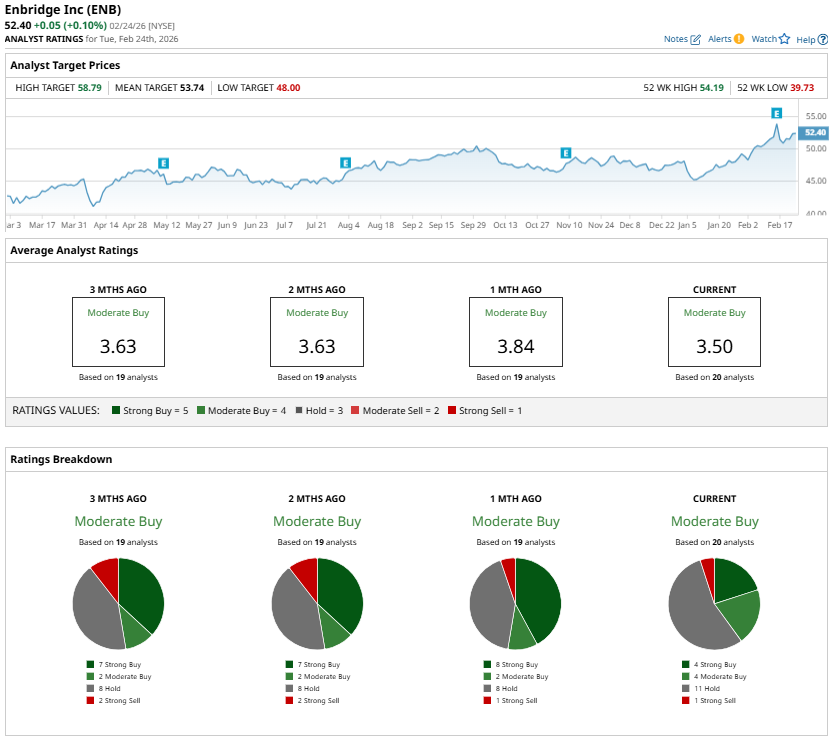

Wall Street analysts currently maintain a “Moderate Buy” consensus rating on ENB stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)