/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

Oracle (ORCL) just made a bold move that’s sending mixed signals to investors. The software giant announced a $20 billion equity distribution agreement, effectively allowing itself the flexibility to sell shares into the market over time. The move comes at a pivotal moment for Oracle, as it ramps up spending to expand the capacity of its cloud infrastructure business while facing heightened scrutiny over leverage and execution risk.

On the one hand, the announcement can be read as a vote of confidence. Oracle is sitting on a staggering cloud backlog and has already signed contracts with some of the world’s largest AI and technology players, creating an urgent need to expand data center capacity. Raising equity alongside debt could help the company fund that growth while preserving balance sheet flexibility. On the other hand, equity issuance is never painless for shareholders.

Let's break down what Oracle’s $20 billion common stock sale really means and whether investors should consider buying ORCL shares right now.

About Oracle Stock

Oracle Corporation is a global technology leader specializing in cloud infrastructure, software, and hardware. The company is one of the world’s largest software providers and is primarily known for its flagship product, the Oracle Database, the first commercially available SQL-based relational database management system. It also provides a comprehensive suite of Infrastructure-as-a-Service (IaaS) and Platform-as-a-Service solutions (PaaS), including the world’s first autonomous database. In addition, the company offers a deep suite of AI-powered enterprise applications, including Enterprise Resource Planning, Human Capital Management, Customer Relationship Management, and Supply Chain Management. It has a market cap of $463.1 billion.

Shares of the database software maker have slumped 28% so far this year, pressured by a bondholder lawsuit, a series of analyst downgrades and price target cuts, and a macro backdrop that has turned less favorable for AI infrastructure spending.

Oracle Is Selling $20 Billion in Common Stock to Fund AI Infrastructure Expansion

On Feb. 2, Oracle said it had entered into an equity distribution agreement to sell up to $20 billion of its common stock. The common share sales will be conducted through an at-the-market offering. This means the company will sell shares “from time to time” at prevailing market prices, rather than a sudden, one-time dump of shares. Still, ORCL stock closed down 2.8% on Monday amid those sales. The stock also fell 3.4% on Tuesday and 5.2% on Wednesday, though those declines were mostly driven by investors rotating out of tech stocks. Bloomberg reported that the company also looks to raise roughly $5 billion through mandatory convertible preferred bonds. Notably, a mandatory convertible preferred bond is a hybrid security that pays regular dividends/coupons but is legally required to convert into a predetermined amount of common stock on a set future date.

The common equity issuance is part of the company’s recently announced Equity and Debt Financing plan for calendar year 2026, under which it aims to raise between $45 billion and $50 billion to support the expansion of its fast-growing Oracle Cloud Infrastructure business. Doing simple math, it’s clear that roughly half of the total amount is expected to be raised through debt. And the company moved rapidly on the bond offering and completed it on Monday.

Oracle attracted record demand for its $25 billion bond offering on Monday. The software giant issued debt across eight tranches, with maturities spanning from three to 40 years. Investors submitted orders totaling up to $129 billion for Oracle’s bonds, surpassing the previous record of $125 billion set when Meta Platforms (META) sold $30 billion in bonds last October. What stands out is that the bond offering went off without a hitch, even as the tech firm has become a barometer for concerns over debt-funded AI spending.

Before Monday, Oracle had roughly $100 billion in long-term debt, according to FactSet. Its debt has been trading more like junk for weeks, reflecting concerns that its AI investments may take years to pay off or may not pay off at all. However, the tech firm’s long-dated bonds surged in the secondary market, and a key measure of its credit risk declined by the most since April 2021 following the announcement of the bond offering. This suggests the company has reassured bond investors that it wouldn’t strain its balance sheet too much.

Analysts said tapping the equity market was the right move, essentially allowing the company to limit additional borrowing and ease investor concerns about its debt. “Oracle’s decision to tap the equity market should help alleviate pressure from the recent widening of Oracle [credit default swap] spreads and reduce fears of over-reliance on debt financing,” according to Mizuho analyst Siti Panigrahi. Moreover, the company said it does not expect to issue additional debt in 2026, offering further reassurance to investors concerned about its borrowing. By combining this $20 billion equity raise, along with a reported $5 billion from mandatory convertible preferred bonds, with roughly $25 billion in debt financing, Oracle aims to preserve balance sheet health while funding massive capital expenditures. Oracle needs all that money to build capacity for its cloud infrastructure business so it can fulfill already contracted demand from customers such as Nvidia (NVDA), Meta Platforms, OpenAI, xAI, and Advanced Micro Devices (AMD).

It’s also worth noting a key drawback of the equity approach, which is, of course, shareholder dilution. Analysts estimate the program could add over 100 million new shares to the market. Still, management appears confident in its $523 billion cloud backlog, arguing that the dilution today is worth a larger share of a much bigger revenue base in the future.

Should You Buy ORCL Shares Now?

While Oracle managed to ease some investor concerns around its AI-related borrowing, worries about its ability to convert a substantial backlog into revenue and the concentration of future revenue among only a few customers remain. I discussed this more in-depth in my previous article on ORCL. On the other hand, the further ORCL shares decline, the more they start to look “too cheap to ignore.” If the stock can stabilize around the $150 support level and show some signs of bullish momentum, it could present an attractive opportunity to add a small position. If the stock continues to fall, I would look to the $100-$130 range as a potential buying zone.

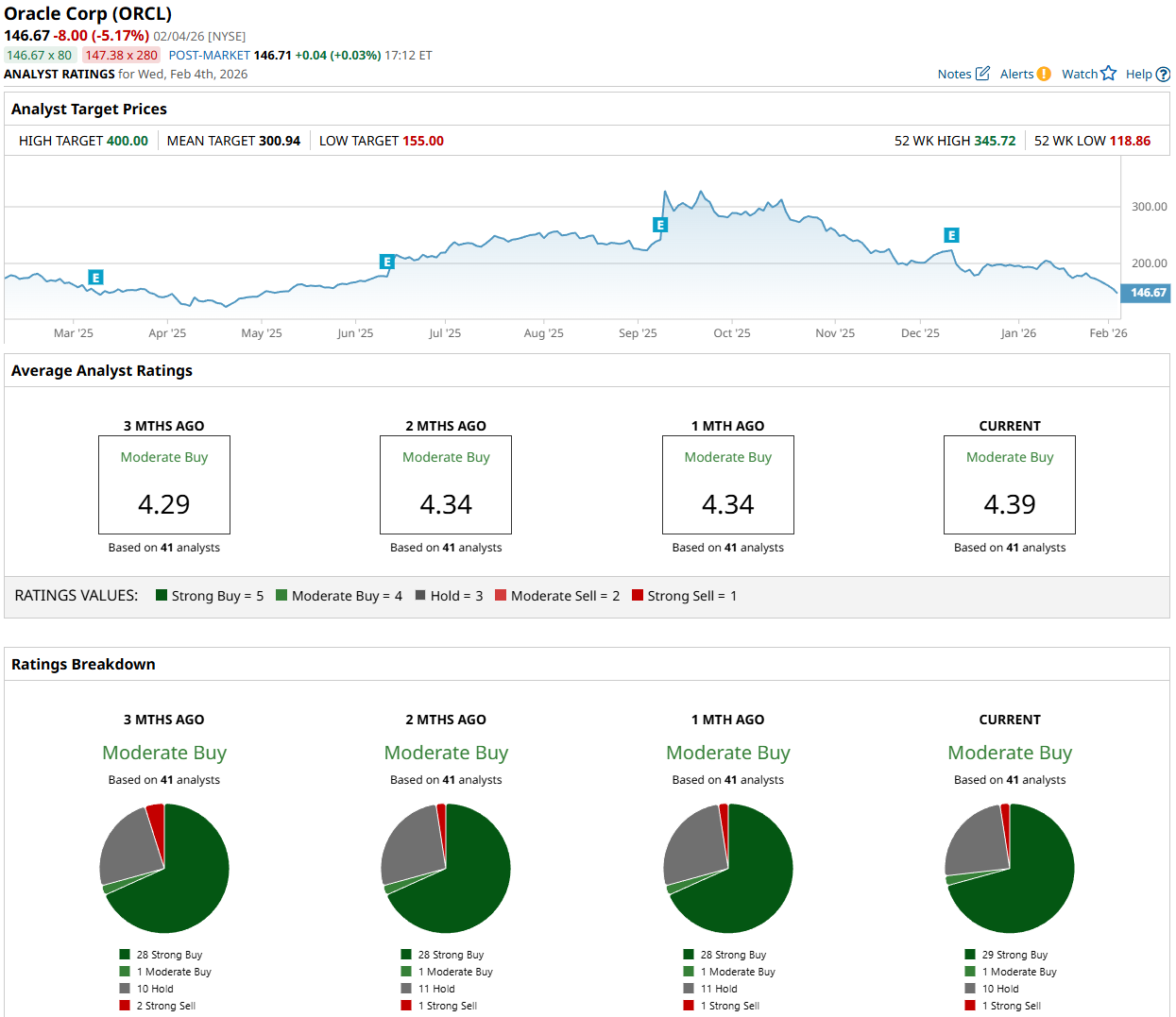

Meanwhile, Wall Street analysts remain largely bullish on ORCL stock, as reflected in its consensus “Moderate Buy” rating. Of the 41 analysts covering the stock, 29 rate it a “Strong Buy,” one recommends a “Moderate Buy,” 10 suggest holding, and one gives it a “Strong Sell” rating. The average price target for ORCL stock is $300.94, implying the stock could more than double from current levels.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)