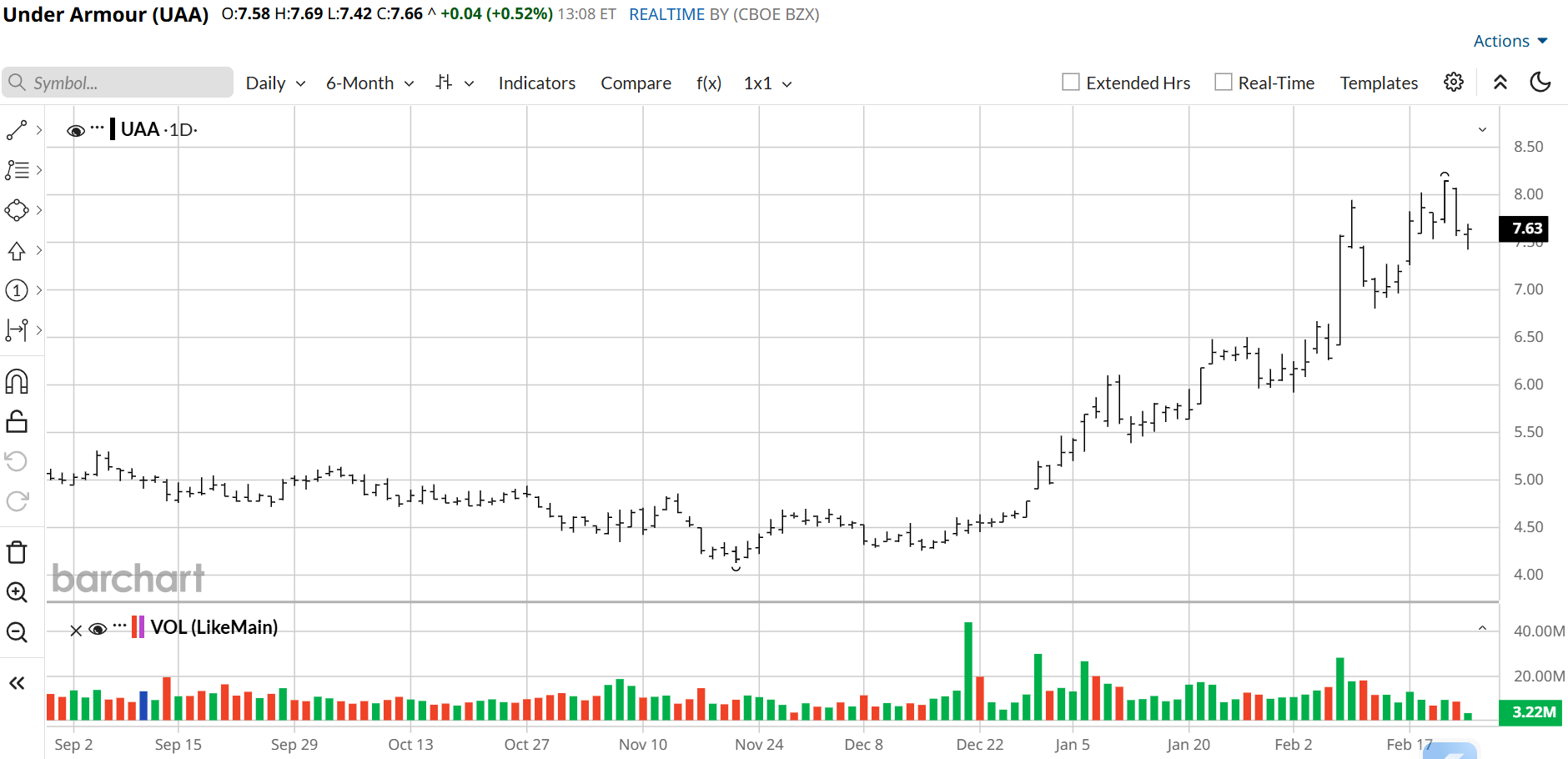

Under Armour (UAA) (UA) has quietly gone from a market afterthought to a market talking point. The stock is up more than 50% over the last six months, upending analyst expectations amid a still-developing corporate turnaround.

Behind that move is a powerful tell: insider conviction. Over the last 12 months, insiders have accumulated more than 44 million shares, leaning in while much of Wall Street remains cautious. Today, we outline why a revamped corporate strategy, improved cost discipline, and easing trade policy headwinds could unlock further upside in Under Armour.

What Under Armour Does—And Why It Still Matters

Under Armour is no longer the hypergrowth disruptor it was in the early 2010s—but it remains one of the most recognizable performance brands in global athletic apparel. With deep roots in training, team sports, and performance gear, Under Armour still commands strong consumer awareness, particularly in North America, even after years of market share erosion and strategic missteps.

What’s changed is how the company is positioning itself. Under Armour has exited non-core businesses, including fitness technology platforms like MyFitnessPal and MapMyFitness, and is now focused squarely on simplifying its product portfolio, reducing discounting, and elevating brand storytelling. The current strategy is deliberately narrower: fewer product lines, higher average selling prices, and a renewed emphasis on performance credibility rather than chasing lifestyle trends.

That reset matters because Under Armour is operating from a much smaller base than peers like Nike (NKE) or Adidas (ADDYY). With roughly 2% of market share in the global sportswear industry, the company doesn’t need to reclaim past dominance to generate upside. Instead, it only needs to stabilize its core categories and improve profitability.

In that sense, the story is no longer about growth leadership, but about whether a leaner, more focused Under Armour can rebuild earnings power against a backdrop of muted expectations.

Signs of Stabilization Are Emerging Amid Turnaround Effort

Under Armour’s most recent earnings update offered cautious but notable progress. In early February, the company reported better-than-expected third-quarter results, with revenue of roughly $1.33 billion, ahead of consensus expectations near $1.31 billion, and profitability coming in above forecasts.

As part of the earnings release, management also raised its full-year adjusted earnings outlook, prompting a double-digit rally in the stock. Importantly, executives described the December quarter as the likely “bottom of the reset,” particularly in North America, where demand trends have been under pressure for some time.

Revenue is still declining, and the company expects full-year sales to fall about 4%. But the trajectory is improving. Adjusted earnings guidance was lifted meaningfully, inventory has been reduced, discounting has been pulled back, and roughly 25% of product lines have been eliminated to concentrate on higher-margin categories like training, running, and team sports.

Margins remain constrained by tariff costs and a deliberate pullback from promotions, but the direction of travel is starting to improve. Importantly, management’s commentary around the fall order book in North America was more constructive than in prior quarters, pointing to early traction from the reset strategy. This is not a growth inflection yet, but it is a meaningful signal that the business may be stabilizing after several years of decline.

That emerging stabilization thesis is beginning to find external support. In early February, UBS reaffirmed its “buy” rating on Under Armour and raised its price target from $8 to $11, citing survey data that suggests the brand’s consumer relevance remains stronger than the stock’s valuation implies. From recent trading levels near $7.50 per share, that target implies roughly 45% upside.

Insider Buying, Trade Policy Tailwinds, and an Underappreciated Valuation

In an apparel market where investors remain cautious, Under Armour is beginning to stand out for a different reason. The story is no longer centered on hype or rapid growth, but on conviction—most notably from those closest to the business. After years of restructuring, brand simplification, and declining revenue, the stock is priced for skepticism. Yet beneath that pessimism, several emerging signals suggest the risk-reward profile may be quietly shifting.

The most striking of those signals is insider activity. Over the past 12 months, Under Armour has seen 70 insider buys versus just 16 sells. More importantly, insiders have purchased over 44 million shares, compared with just over 300,000 shares sold during the same period. That imbalance is hard to ignore. It points to sustained, broad-based conviction rather than a single symbolic trade.

Adding important context to that narrative, a 10% owner recently purchased 13.2 million shares of Under Armour in open-market transactions, committing approximately $67 million at just over $5 per share. The stock has since rallied above $7.50. For a long-term holder, this scale of buying functions as a clear vote of confidence in the reset underway and suggests that perceived downside risk may be increasingly constrained.

Insider buying of this scale tends to matter less as a timing tool and more as a statement about downside risk. It often reflects improving internal visibility before stabilization becomes obvious in reported results. In Under Armour’s case, the consistency and magnitude of buying suggest a growing belief that expectations have fallen too far relative to the company’s underlying brand value and early signs of operational traction.

That insider conviction is surfacing alongside a valuation that remains skewed to the downside. Under Armour trades at roughly 0.7x trailing sales, below industry averages, while its 2.4x price-to-book multiple sits closer to peer norms. At those levels, the market appears to be discounting revenue durability and margin recovery, while assigning limited credit to the potential for continued operational improvement.

On top of the above, there’s also the potential for policy-related upside that’s not fully reflected in current estimates. Tariffs are expected to add roughly $100 million in costs this fiscal year, weighing on margins just as Under Armour is pulling back on discounting and narrowing its product focus.

However, a recent Supreme Court ruling clarified that the Trump administration’s ability to impose tariffs is no longer unlimited. While tariffs can still be pursued through alternative mechanisms, the decision underscores that trade policy now faces clearer constraints. That shift modestly improves the risk backdrop, and any easing or delay in tariff pressure would provide incremental margin support at a time when Under Armour is already making progress on cost reduction.

Bottom Line

Under Armour hasn’t suddenly turned into a high-growth story, but it doesn’t need to be, at least not yet. What matters more at this stage is stabilization, and on that front the company appears to be making progress. Management has tightened the product portfolio, reduced discounting, lowered inventory levels, and refocused the brand on higher-margin categories where it has historically performed best.

That improving backdrop is reinforced by other positive signals. Insider buying has been unusually heavy over the past year, with roughly 70 open-market purchases compared with just 16 sales. In total, insiders have acquired more than 44 million shares while selling just over 300,000, an imbalance that is notable even for a turnaround situation.

External validation has added to the improving narrative. UBS recently upgraded Under Armour to a “buy,” citing consumer survey data that suggests brand relevance and purchase intent remain stronger than the stock’s valuation implies. UBS also raised its price target from $8 to $11, reinforcing the view that expectations may have swung too far to the downside.

To be clear, Under Armour has not resolved all of its challenges. Still, with cost discipline improving, insider conviction rising, and early signs that the core business is stabilizing, the setup is becoming more constructive. From here, even incremental progress through margin stabilization or a better revenue mix could support a higher valuation. And with shares up more than 50% over the past six months, investors appear to be warming to the bull case.

Disclosure: The author holds a long position in Under Armour at the time of publication.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)