Headquartered in Houston, Texas, APA Corporation (APA) is an independent energy producer focused on natural gas, oil, and natural gas liquids. With a market cap of roughly $9.4 billion, the company runs diversified assets across the United States, Egypt’s Western Desert, the U.K. North Sea, and offshore exploration acreage in Suriname.

Over the past 52 weeks, APA Corporation’s shares jumped 14.9%, narrowly beating the S&P 500 Index’s ($SPX) 14.3% gain. The stock also strengthened its relative performance in 2026, rising nearly 8% year-to-date (YTD) compared with just a 1.4% increase for the broader benchmark, signaling consistent outperformance across timeframes.

Within the energy landscape, APA stock outpaced the State Street Energy Select Sector SPDR ETF (XLE) over the last year. While XLE climbed 13.2% during the same 52-week period, it trailed APA’s stronger advance. However, momentum flipped YTD, with XLE up 14.2%, highlighting a short-term rotation away from energy leadership.

The price performance saw a boost on Wednesday, Jan. 21, when APA shares jumped nearly 4.7%. The rally came a day after the release of supplemental Q4 2025 operational and financial details, offered ahead of the Feb. 26 earnings call.

In Egypt, tax barrels averaged 34 MBoe/d, while dry-hole costs reached $20 million pre-tax. Oil and gas transactions, including derivatives, delivered a strong $193 million in pre-tax net profit. Offsetting that strength, transaction and reorganization costs doubled sequentially to $36 million from $18 million.

U.S. operations felt the sting of weak Waha pricing. APA responded by trimming output, cutting 91 MMcf/d of natural gas and 7,600 barrels per day of natural gas liquids. These cuts underline disciplined capital management, but they also reflect near-term revenue sensitivity to regional price dislocations.

Looking at earnings, analysts project diluted EPS of $3.48 for fiscal year 2025, which ended in December, marking a 7.7% year-over-year decline. Even so, APA Corporation’s recent track record lends credibility, as the company beat EPS estimates in three of the past four quarters, missing only once.

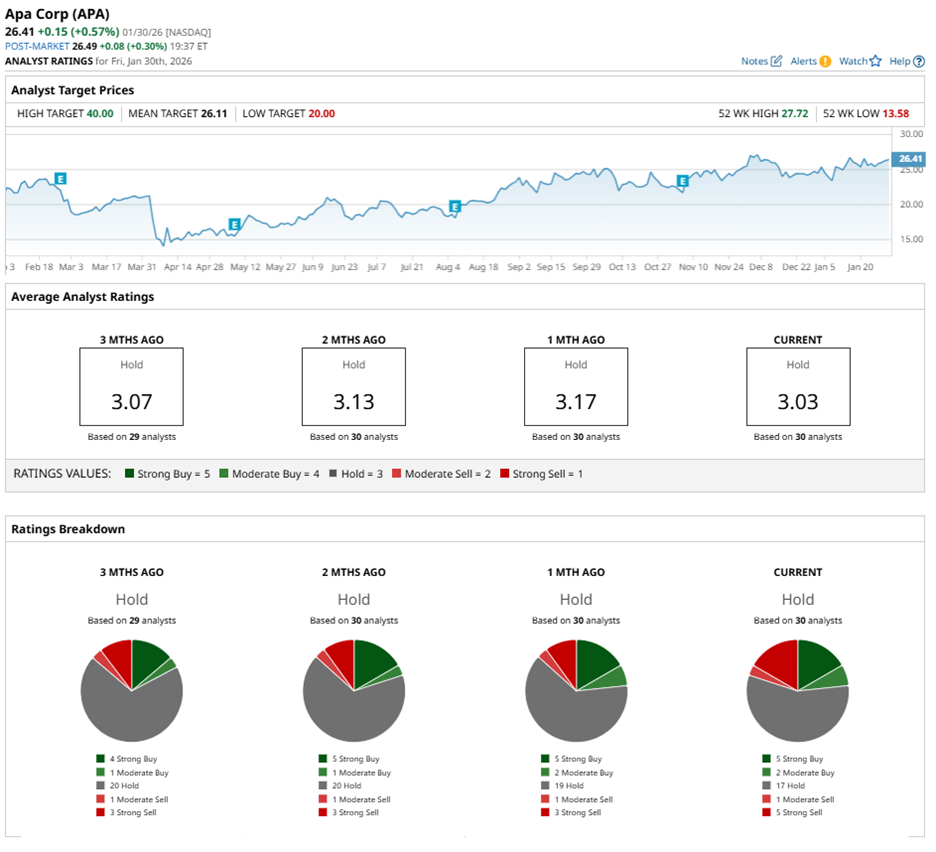

Wall Street, however, remains measured rather than convinced. Among 30 analysts, the consensus rating sits at “Hold,” comprising five “Strong Buy,” two “Moderate Buy,” 17 “Hold,” one “Moderate Sell,” and five “Strong Sell” ratings.

The current analyst sentiment has not budged much over the past three months, when four analysts also rated the stock a “Strong Buy.”

On Jan. 5, Bernstein analyst Bob Brackett trimmed his price target to $25 from $26 while maintaining a “Market Perform” rating. Bernstein expects 2026 oil markets to remain volatile and range-bound near term, yet sees a more constructive long-term setup, anchoring its balanced outlook on the stock.

At current levels, APA stock is already trading above its mean price target of $26.11, implying limited near-term rerating. Still, the Street-high target of $40 suggests a gain of 51.5% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)