Morgan Stanley downgraded Affirm (AFRM) from “Overweight” to “Equal Weight” on June 25, simultaneously removing the stock from its Top Pick list.

Analyst James Faucette characterized the move as a “valuation call” rather than a structural one — emphasizing that the firm’s long-term conviction on AFRM’s positioning remains fully intact.

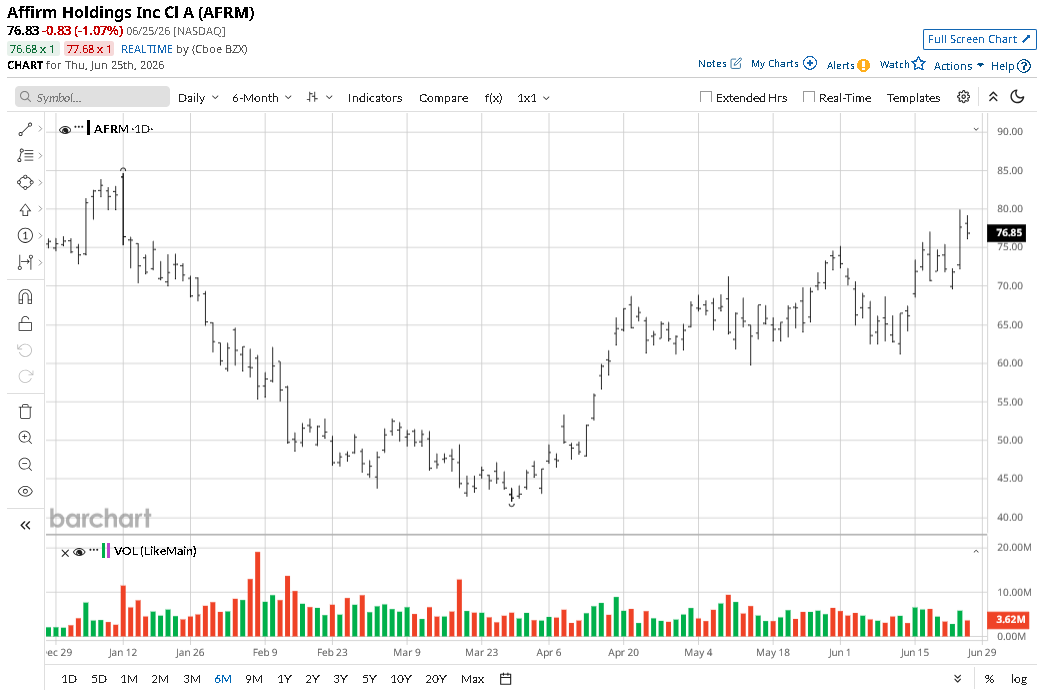

At the time of writing, Affirm stock is trading just 4% above its price at the start of this year.

Why Morgan Stanley Downgraded AFRM Shares

The downgrade comes after AFRM shares surged more than 80% from their March 27 close, a rally that Morgan Stanley believes has brought the stock to fair value.

The bank noted that three key concerns underpinning its original bullish thesis — GMV durability, funding execution, and credit performance — have largely been resolved, with the fintech company demonstrating best-in-class execution across asset-backed securities and forward flow channels.

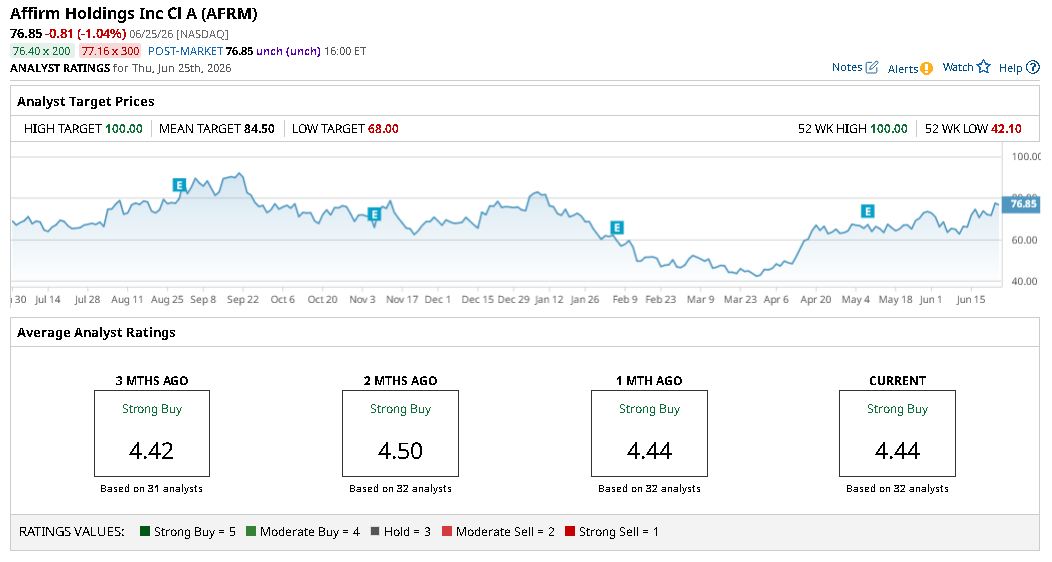

Morgan Stanley’s fiscal 2028 earnings per share (GAAP) estimate for Affirm Holdings has risen to $3.37 from $2.95 in early February, well above the street consensus of $2.50.

However, the bank argued that further significant upward revisions toward $4.50 to $5.00 in FY28 GAAP EPS would be needed to justify continued active sponsorship at current levels.

This sets a high bar for re-engagement with the name.

Long-Term Thesis for Affirm Stock Remains Intact

On June 25, Morgan Stanley left its $79 price target unchanged, describing its posture as stepping to the sidelines while awaiting a more attractive entry point.

Faucette continued to describe Affirm shares as one of the highest quality fintech assets in the bank coverage, citing best-in-class management, differentiated product capabilities, and direct exposure to secular buy-now-pay-later (BNPL) category share gains.

A separate research firm recently highlighted BNPL companies as a widely overlooked investment theme, pushing back against narratives that the sector represents systemic risk and pointing to fundamental misunderstandings of the business model’s accounting mechanics under GAAP.

That more constructive structural view aligns with Morgan Stanley’s continued positive long-term assessment of Affirm shares, even as its near-term tactical stance has shifted to neutral.

What’s the Consensus Rating on Affirm?

In summary, this downgrade represents a classic case of a sell-side firm banking profits after a thesis plays out successfully rather than signaling deterioration in fundamentals.

The message to investors is clear: Affirm’s operational execution has validated the original bull case, but the stock price now reflects that improvement, leaving limited asymmetric upside without a new catalyst or meaningful earnings surprise.

Other Wall Street analysts, however, remain bullish on AFRM stock, with price targets as high as $100 indicating potential upside of 35% from current levels.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)