Regional banking company Glacier Bancorp (NYSE:GBCI) met Wall Streets revenue expectations in Q4 CY2025, with sales up 35% year on year to $306.5 million. Its GAAP profit of $0.49 per share was in line with analysts’ consensus estimates.

Is now the time to buy Glacier Bancorp? Find out by accessing our full research report, it’s free.

Glacier Bancorp (GBCI) Q4 CY2025 Highlights:

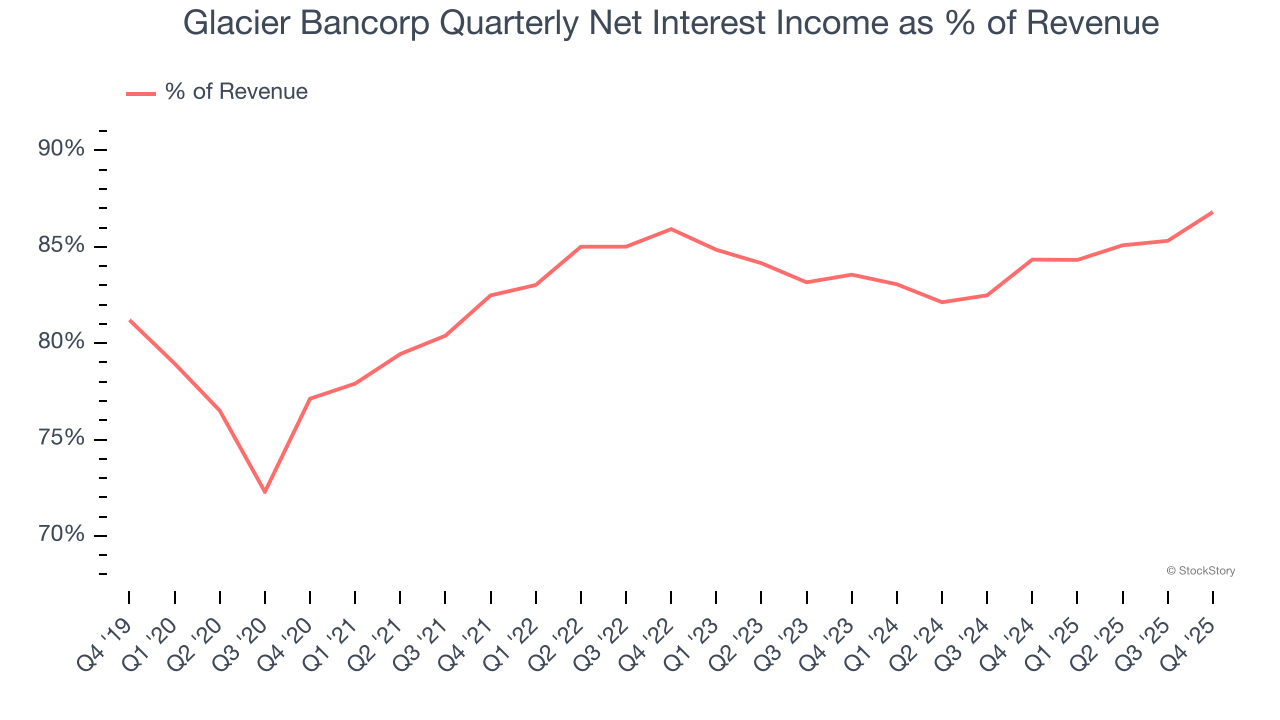

- Net Interest Income: $266.1 million vs analyst estimates of $267.1 million (39% year-on-year growth, in line)

- Net Interest Margin: 3.6% vs analyst estimates of 3.6% (in line)

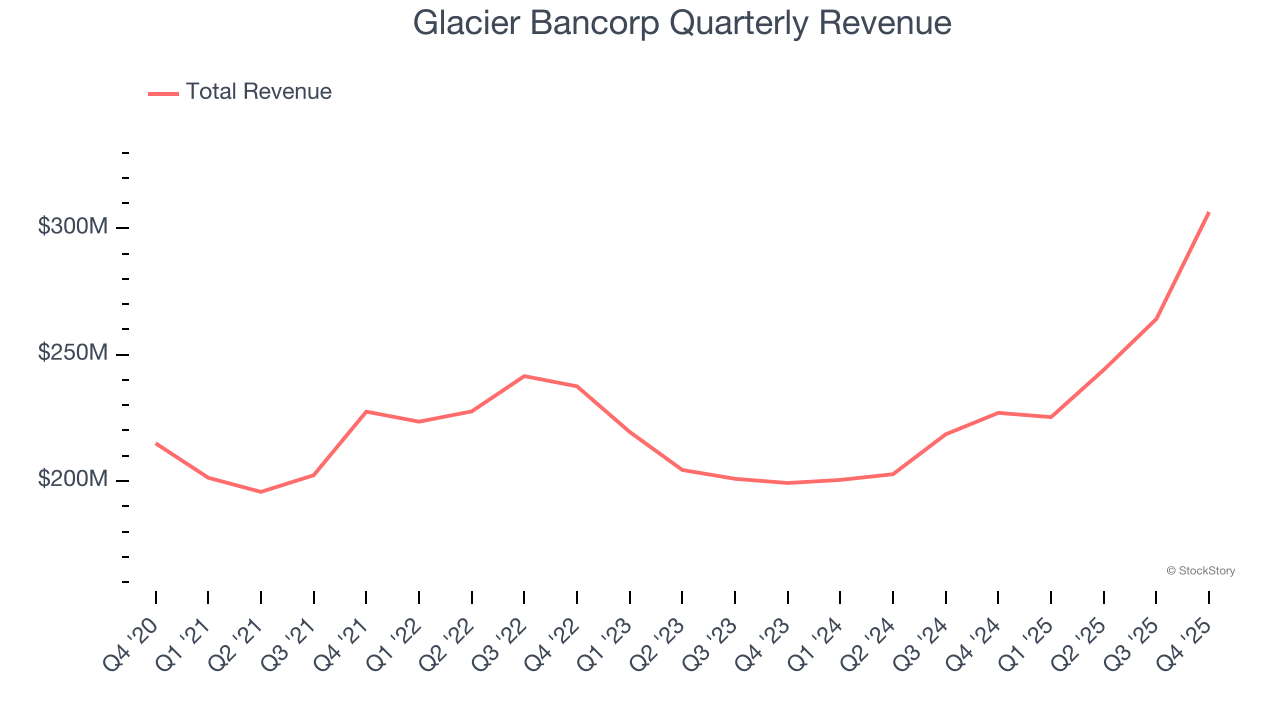

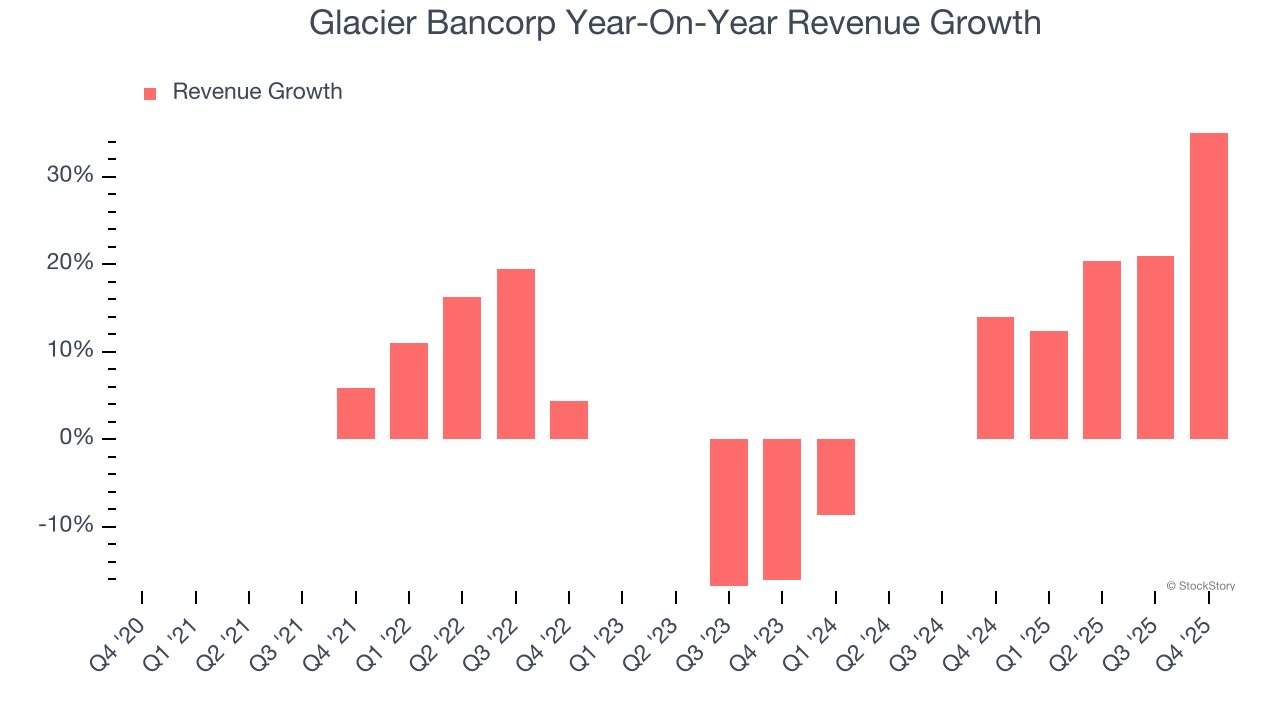

- Revenue: $306.5 million vs analyst estimates of $308 million (35% year-on-year growth, in line)

- Efficiency Ratio: 61% vs analyst estimates of 60.9% (13.8 basis point miss)

- EPS (GAAP): $0.49 vs analyst estimates of $0.49 (in line)

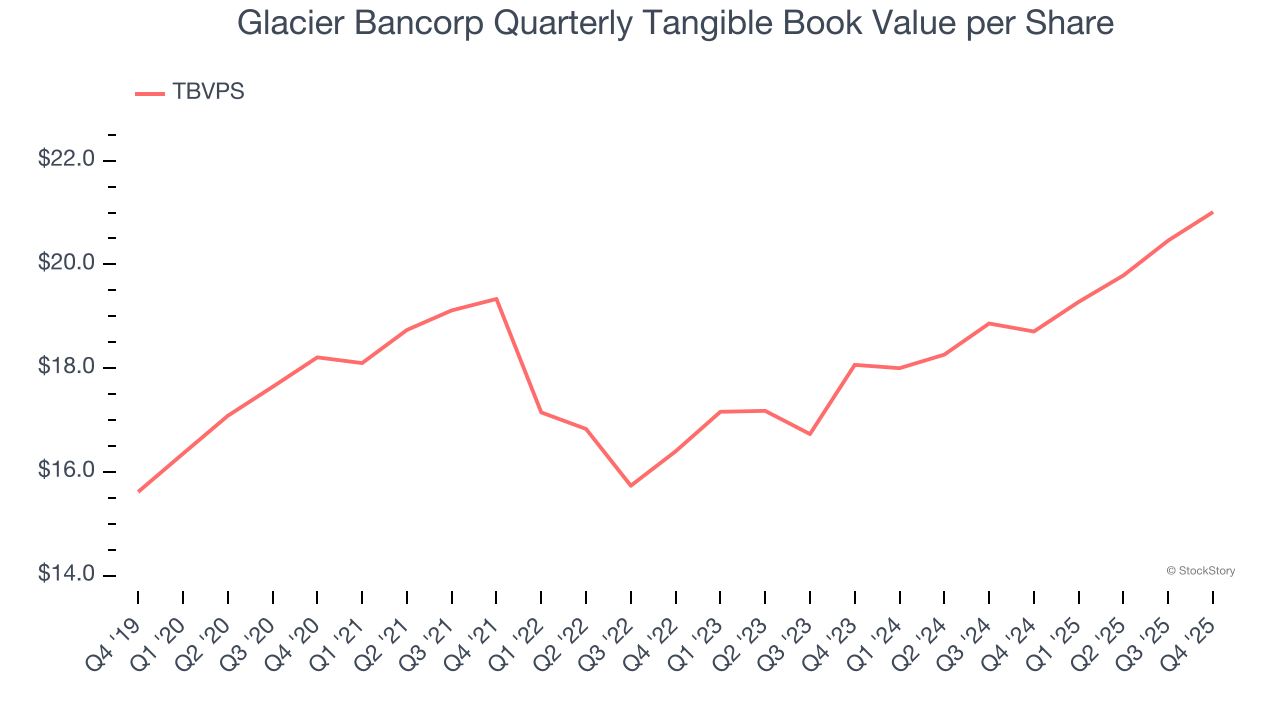

- Tangible Book Value per Share: $21.01 vs analyst estimates of $20.73 (12.3% year-on-year growth, 1.4% beat)

- Market Capitalization: $6.45 billion

KALISPELL, Mont., Jan. 22, 2026 (GLOBE NEWSWIRE) -- Glacier Bancorp, Inc. (NYSE: GBCI) reported net income of $63.8 million for the current quarter, a decrease of $4.1 million, or 6 percent from the prior quarter net income of $67.9 million and an increase of $2.0 million, or 3 percent, from the $61.8 million of net income for the prior year fourth quarter. Diluted earnings per share for the current quarter was $0.49 per share, a decrease of $0.08 per share, or 14 percent, from the prior quarter diluted earnings per share of $0.57 and a decrease of $0.05 per share, or 9 percent, from the prior year fourth quarter diluted earnings per share of $0.54. The current quarter included $27.2 million of credit loss expense from the acquisition of Guaranty, $5.8 million in acquisition-related expenses, $3.0 million of expenses related to vacating branch locations, $1.4 million of income related to bank owned life insurance proceeds and $827 thousand of reduction of expense related to a prior year FDIC special assessment. “Glacier Bancorp delivered another year of strong performance, marked by a 26 percent increase in earnings and significant strategic progress. In 2025, we expanded our footprint with the acquisitions of Bank of Idaho and Guaranty Bank & Trust, strengthening our presence in high-growth markets and positioning us for continued success,” said Randy Chesler, President and Chief Executive Officer.

Company Overview

Operating through seventeen distinct bank divisions with local brands and management teams, Glacier Bancorp (NYSE:GBCI) is a bank holding company that provides various banking services to individuals and businesses across eight western states.

Sales Growth

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Over the last five years, Glacier Bancorp grew its revenue at a sluggish 5.7% compounded annual growth rate. This was below our standard for the banking sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Glacier Bancorp’s annualized revenue growth of 12.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Glacier Bancorp’s year-on-year revenue growth of 35% was wonderful, and its $306.5 million of revenue was in line with Wall Street’s estimates.

Net interest income made up 83.4% of the company’s total revenue during the last five years, meaning Glacier Bancorp barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Glacier Bancorp’s TBVPS grew at a sluggish 2.9% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 7.8% annually over the last two years from $18.06 to $21.01 per share.

Over the next 12 months, Consensus estimates call for Glacier Bancorp’s TBVPS to grow by 8.8% to $22.86, paltry growth rate.

Key Takeaways from Glacier Bancorp’s Q4 Results

It was good to see Glacier Bancorp narrowly top analysts’ tangible book value per share expectations this quarter. On the other hand, its EPS was in line and its revenue was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $49.86 immediately following the results.

So should you invest in Glacier Bancorp right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20logo%20on%20phone%20and%20site-by%20Majahid%20Mottakin%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)