/International%20Paper%20Co_%20magnified%20by-%20Casimiro%20PT%20via%20Shutterstock.jpg)

International Paper Company (IP) transforms renewable resources into essential, everyday products that sustain the global economy. As a global leader in fiber-based solutions, the company designs packaging that protects and showcases goods, supports worldwide commerce, and helps keep consumers safe. It also produces renewable materials such as pulp used in diapers, tissue, and other personal care products, while advancing circular solutions that promote recycling, cut waste, and support a more sustainable future.

The Tennessee-based company currently carries a market capitalization of about $20.4 billion, placing it firmly in “large-cap” territory, well above the $10 billion benchmark. Strengthening its global footprint, International Paper made a transformative move in 2025 with the acquisition of DS Smith, creating an industry heavyweight with a strong focus on the fast-growing North American and EMEA markets.

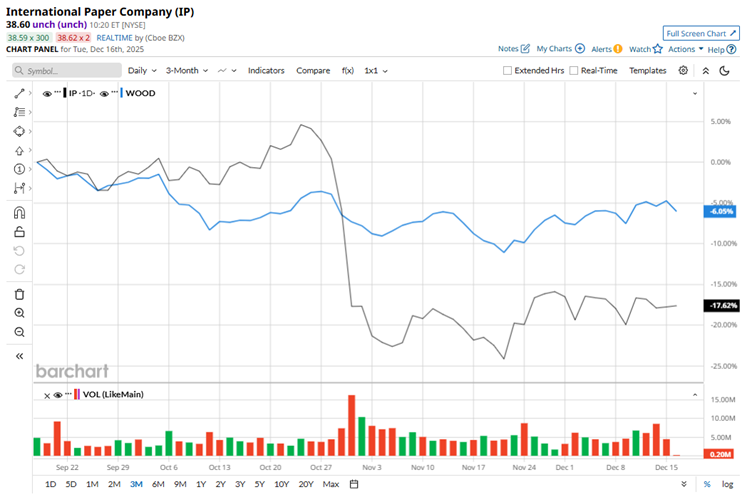

However, despite the company’s significant role in the economy, its shares appear to lag behind those of its peers. We benchmark the stock against the iShares Global Timber & Forestry ETF (WOOD), a natural fit given International Paper’s core role in the timber value chain, where it sources wood fiber and converts it into essential packaging, paper, and pulp products used worldwide.

International Paper has been under heavy pressure lately. The stock has fallen 16.2% over the past three months, far worse than the benchmark ETF’s 4.3% dip. After peaking at $60.15 in January, IP has since given up nearly 35.5%, underscoring how sharply sentiment has cooled.

The longer-term picture offers little relief. International Paper’s shares are down 30.5% over the past year and have fallen another 28% in 2025, signaling sustained pressure on the stock. By contrast, the iShares Global Timber & Forestry ETF has been far more resilient, posting comparatively modest declines of 9.6% over the past year and 6.1% in 2025, highlighting just how sharply IP has lagged its sector peers.

From a technical standpoint, the trend remains weak. International Paper has stayed below its 200-day moving average since the end of July and has also traded below its 50-day moving average for most of that stretch, with only brief, short-lived rebounds along the way.

Investors have remained cautious on International Paper as the company continues to restructure its operations throughout the year. Broader industry headwinds, including uneven demand, elevated input costs, and an evolving market landscape, have weighed down the stock. These pressures have led to recent financial losses and plant closures, even as the company retains long-term upside tied to the growing shift toward sustainable packaging.

Adding to near-term concerns, International Paper announced in early November that it will close two U.S. packaging plants by January as part of its ongoing cost-cutting and consolidation strategy in response to softer demand. The closures will affect facilities in Compton, California, and Louisville, Kentucky, impacting roughly 218 employees, with production volumes set to be transferred to nearby plants.

IP’s selloff has been notably sharper than that of peer Packaging Corporation of America (PKG). While International Paper is down heavily, PKG has been relatively more resilient, slipping about 14.1% over the past year and 9.5% in 2025.

Despite the stock’s lackluster performance, Wall Street hasn’t lost faith. International Paper currently holds a consensus “Moderate Buy” rating from 13 analysts, signaling confidence. The average price target of $49.71 suggests the stock could climb nearly 28.8% from current levels.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)