/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

BlackRock (BLK) is the world’s largest asset manager, helping individuals, institutions, and governments invest across stocks, bonds, ETFs, private markets, and alternative assets. That scale was on full display in the second quarter as the company delivered another blockbuster earnings report, fueled by strong investor demand and broad-based growth across its business.

Net inflows accelerated across ETFs, private markets, active fixed income, and systematic equity strategies, while the top and bottom lines comfortably topped Wall Street’s expectations. More importantly, those inflows pushed BlackRock’s assets under management (AUM) to a record $15.34 trillion, highlighting the company’s ability to attract fresh capital even in an uncertain market.

Rising AUM is particularly significant for an asset manager because it directly expands the pool of assets on which management fees are earned, supporting future revenue and profit growth. Investors clearly welcomed the results, sending BLK stock sharply higher after the report.

With BlackRock delivering across the board and the stock responding in kind, how should investors play BLK stock now?

About BlackRock Stock

Founded in 1988 and headquartered in New York City, BlackRock is the world’s largest asset manager, overseeing trillions of dollars in assets on behalf of institutional and individual investors worldwide. The company provides a broad range of investment solutions spanning equities, fixed income, multi-asset strategies, alternatives, private markets, and exchange-traded funds (ETFs).

BlackRock is also known for its Aladdin risk management platform, which is widely used by financial institutions for portfolio analytics and risk management. Serving clients across more than 100 countries, the firm has established itself as a global leader in investment management, technology, and financial advisory services. Its market capitalization currently stands at $169.5 billion.

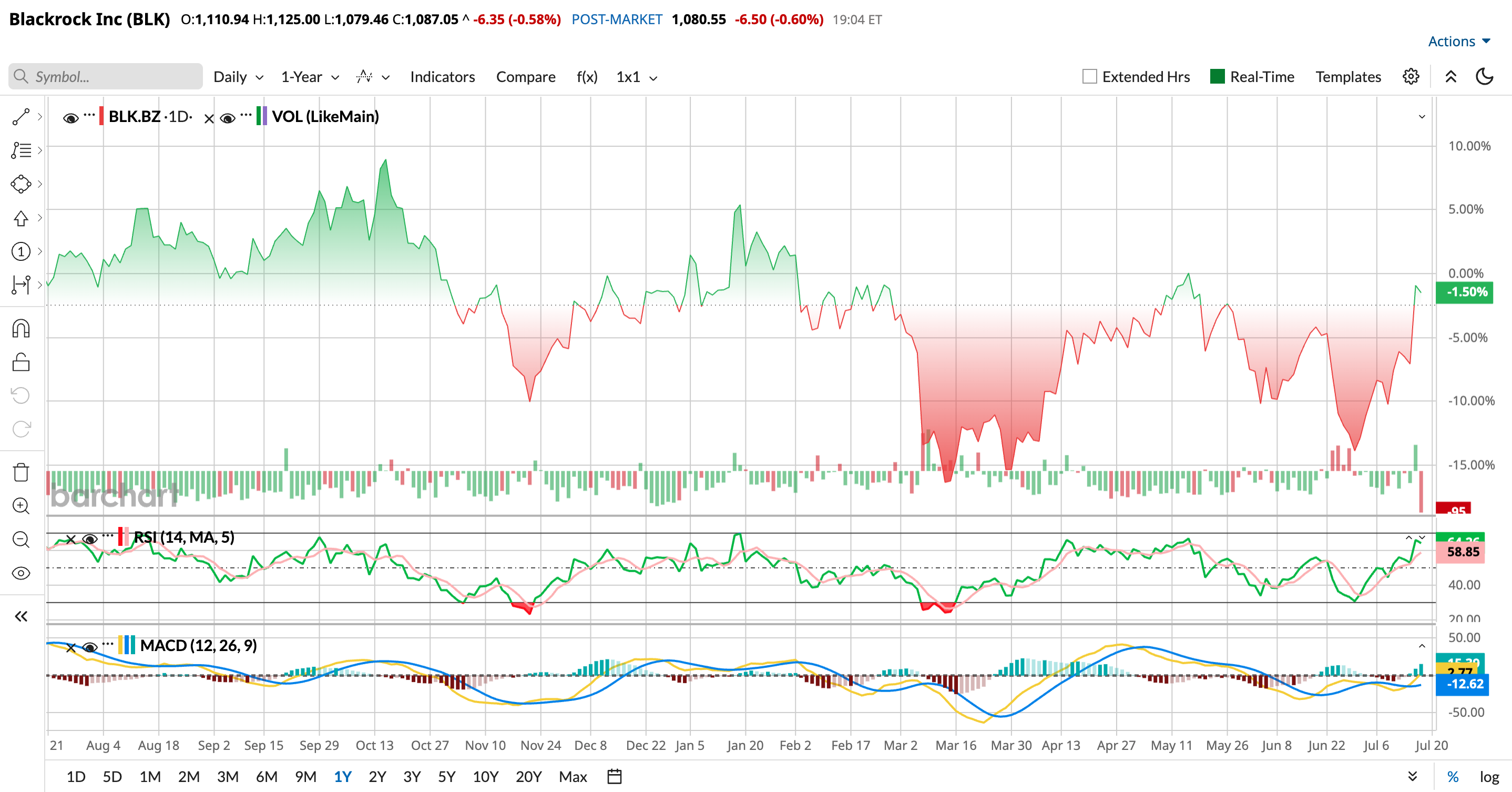

Shares of BlackRock have largely moved sideways over the past year, gaining a modest 0.44%, while its year-to-date (YTD) return stands at 1.56%. However, the recent momentum tells a much stronger story.

BLK stock has gained 3.3% over the past month and 6.1% during the last three months, reflecting growing investor optimism. The biggest catalyst came after the company’s blockbuster second-quarter earnings report, which sent BLK shares soaring 6.63% on July 15 alone. That rally also helped the stock climb 6.61% over the past five trading days. From a technical standpoint, the 14-day RSI has climbed to 64.26, suggesting strong bullish momentum while remaining just below overbought territory.

Valuation-wise, BLK stock is not exactly cheap. The stock trades at 18.93 times forward adjusted price-to-earnings and 5.93 times sales, both above the sector median. However, analysts expect double-digit revenue and earnings growth this fiscal year, making that premium easier to justify.

Beyond growth, BlackRock has also built a strong reputation for rewarding shareholders. The company has paid dividends for more than 20 consecutive years and has increased its payout for 16 straight years. Its latest quarterly dividend of $5.73 per share translates to an annualized payout of $22.92 per share, offering a 2.24% annualized yield. With a 41.23% payout ratio, the dividend appears well covered by earnings, leaving room for future increases.

A Closer Look at Blackrock’s Impressive Q2 Numbers

BlackRock delivered another stellar quarterly numbers recently that reinforced why it continues to dominate the global asset management industry. The company’s latest results were powered by healthy client inflows, rising fee-generating assets, and steady demand across both traditional and alternative investment products, allowing it to comfortably beat Wall Street’s expectations.

Over the last 12 months, BlackRock attracted a remarkable $868 billion in net inflows, translating into 10% organic base fee growth. That momentum remained strong during the second quarter, with long-term net inflows reaching $199 billion, ahead of analysts’ expectations and up sharply from $136 billion in the previous quarter. The strong performance lifted first-half 2026 net inflows to $335 billion, with demand spanning ETFs, private markets, active fixed income strategies, and systematic equity products. The broad-based nature of these inflows suggests investors continue to trust BlackRock across virtually every major asset class.

That growth translated into another impressive financial performance. Adjusted EPS amounted to $13.91 per share, easily surpassing consensus estimates while improving from $12.53 in the previous quarter and $12.05 a year earlier. Revenue surged 30.6% year-over-year (YOY) to $7.08 billion and rose 5.8% sequentially, coming in ahead of expectations.

Chairman and CEO Laurence Fink struck an optimistic tone while discussing the results, saying market fundamentals remain strong, supported by expanding profit margins, healthy earnings momentum, and rapid technological innovation. He highlighted that BlackRock’s client flows during the first six months of 2026 more than doubled from a year earlier, helping push the firm’s AUM to a record $15.3 trillion.

The company’s core fee-generating businesses continued to expand. Investment advisory, administration, and securities lending revenue climbed to $5.73 billion, reflecting both YOY and sequential growth. Meanwhile, technology services revenue increased to $566 million, underscoring continued demand for BlackRock’s technology platform alongside its investment offerings.

Combined with an adjusted operating margin of 45.9%, which is the highest in almost five years, the results suggest BlackRock is not only attracting more client assets but also converting that growth into stronger profitability.

Analysts tracking Blackrock expect its earnings path to look resilient. EPS for fiscal 2026 is expected to be $54.09 per share, up 12.5% annually, and then climb by 15.1% YOY to $62.27 per share in fiscal 2027.

What Do Analysts Expect for Blackrock Stock?

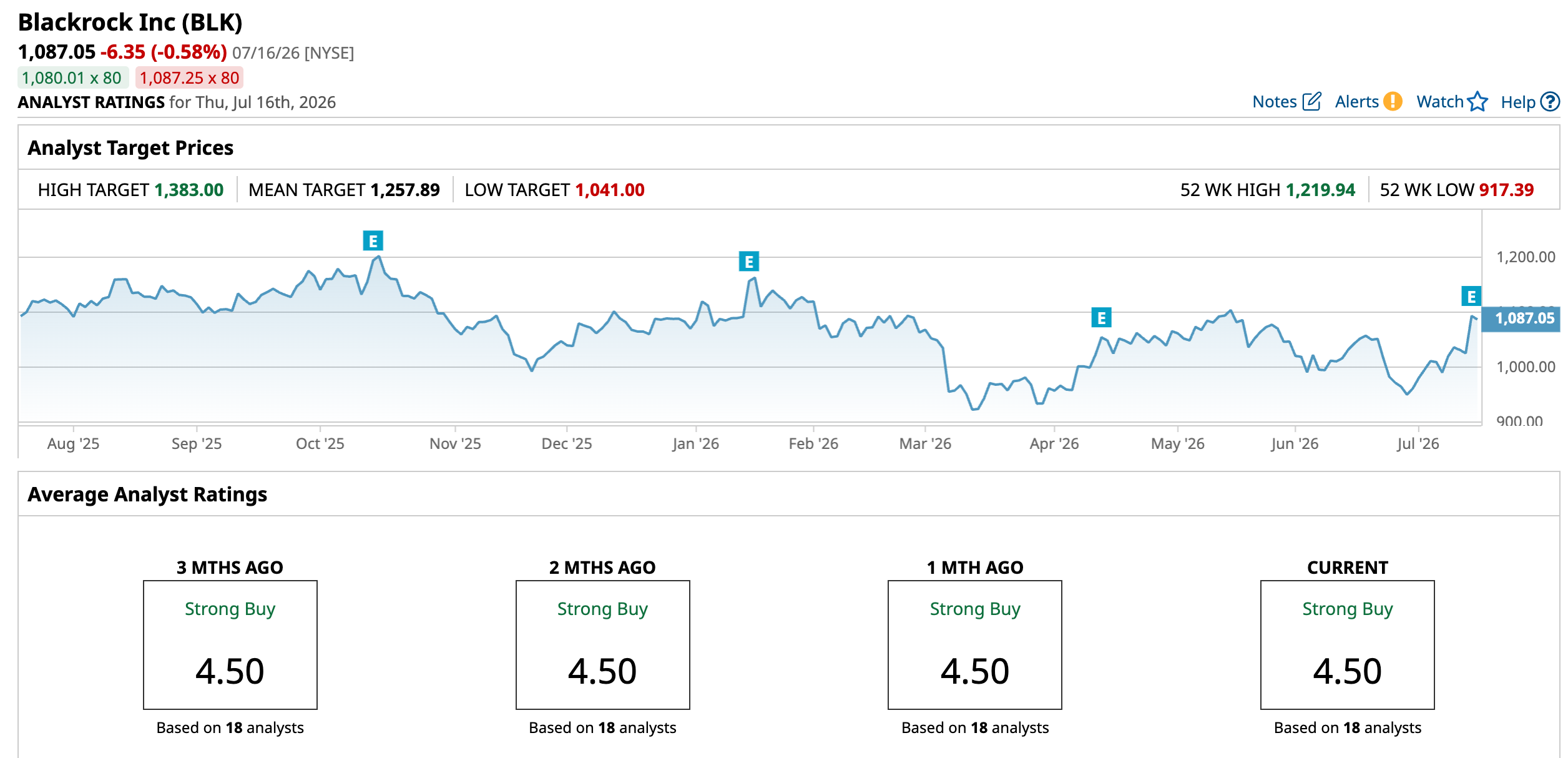

Wall Street's confidence in BlackRock has strengthened following its impressive second-quarter performance. JPMorgan upgraded the stock to “Overweight” from “Neutral”, lifted its price target to $1,364, and added BLK to its Analyst Focus List, citing a favorable setup for fund flows, organic revenue growth, and operating leverage.

Other brokerages echoed the optimism. Barclays raised its target to $1,450, BofA Securities increased its target to $1,320, and Keefe, Bruyette & Woods lifted its target to $1,300, while maintaining bullish ratings.

Meanwhile, Morgan Stanley raised its price target to $1,488 and kept the “Overweight” rating, arguing BlackRock’s valuation remains disconnected from its strong fundamentals despite durable growth, expanding margins, and rising earnings expectations.

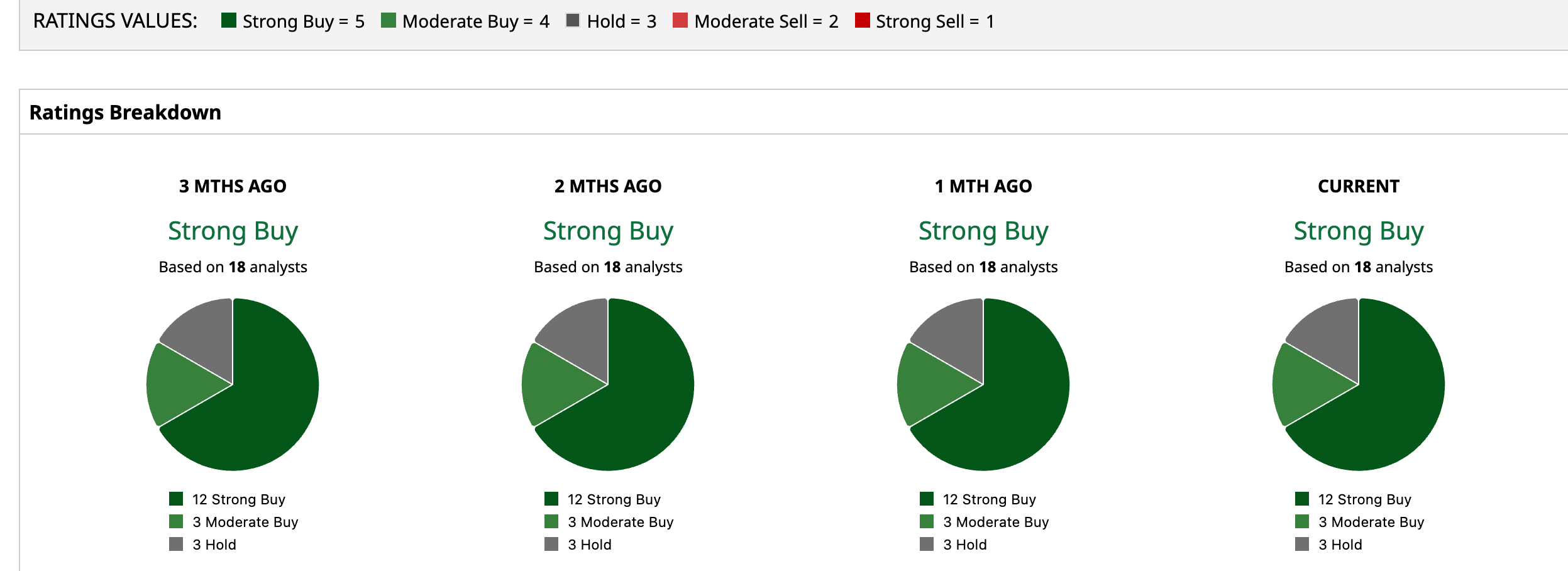

Overall, analysts are upbeat, with BLK currently rated a “Strong Buy” overall. Of the 18 analysts covering the stock, 12 suggest a “Strong Buy,” three advises a “Moderate Buy,” and three recommend a “Hold” rating.

The mean price target of $1,257.89 suggests the stock could surge by 15.7% from the current price levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)