Costco Wholesale just reported June net sales of $29.24 billion, an impressive 10.6% year-over-year (YOY) increase for the five-week retail period ended July 5. Even better, the company said comparable sales for June jumped 8.8%. All of this included a 10% gain in the United States, a 3.7% jump in Canada, and a 4.7% increase in its international markets. In addition, e-commerce comparable sales were up nearly 21% for June.

Of course, the cornerstone of Costco's success remains its membership business model. Unlike other retailers, which rely on product margins, Costco generates a significant portion of its profits from recurring membership fees rather than from product sales. Costco purposefully operates on very low gross margins because the company is more concerned about driving in more net profit from higher-margin membership fees. What makes Costco even more attractive is its $1.47 per share quarterly dividend paid on May 1, with its next dividend payment scheduled for August 7 to shareholders of record as of July 24. Its dividend payout ratio is 27.18%.

How Investors Should View COST for the Second Half

Looking ahead to the second half of the year, Costco appears well positioned to continue outperforming much of the retail sector. Several potential catalysts remain in place. That includes continued membership growth and high renewal rates, strength in e-commerce, stable demand for grocery and essential products, the expansion of international warehouse locations, and continued success of Kirkland Signature products.

Fueling more excitement, Bernstein analyst Zhihan Ma said Costco is one of her top picks for the second half of the year. With a price target of $1,194, Ma said that while inflation continues to squeeze budgets, Costco finds a way to squeeze that into an advantage.

However, Ma isn’t the only COST bull. Bank of America has a “Buy” rating, with a $1,200 price target; Goldman Sachs has a “Buy” rating with a $1,159 price target; JPMorgan has an “Overweight” rating with a $1,110 price target; Raymond James has an "Outperform" rating with a $1,100 price target. Citi has a “Neutral” rating with a $1,020 price target, and Truist has a “Hold” rating with a price target of $1,011 a share.

Moving forward, the stock could see further upside if Costco’s July sales are even better and if the company does announce further returns for investors.

Furthermore, earnings growth has been strong. In the third quarter, Costco saw EPS of $4.93, which beat estimates by $0.01 per share. Revenue of $70.53 billion, up 11.6% YOY, beat by $890 million. Total sales climbed 12% YOY to $69.2 billion, while comparable sales grew about 10% YOY. Customer traffic frequency jumped 2.4% globally, as the average ticket jumped 7.3%. Plus, according to CFO Gary Millerchip, the company ended the quarter with 82.9 million paid members, 148.5 million cardholders, and a renewal rate of 92.2% in the U.S. and Canada. Globally, the renewal rate was 89.7%.

What Do Analysts Say About COST Stock?

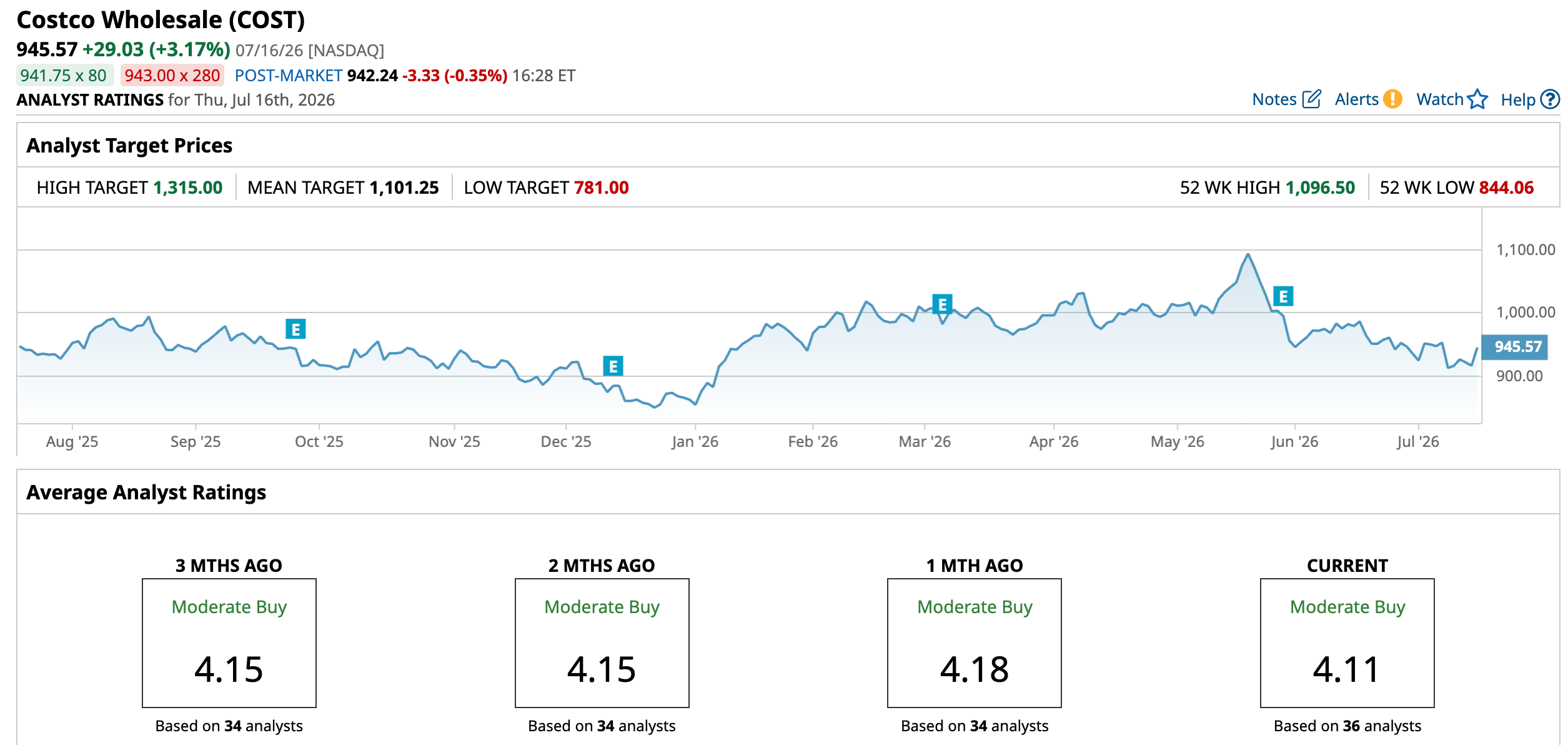

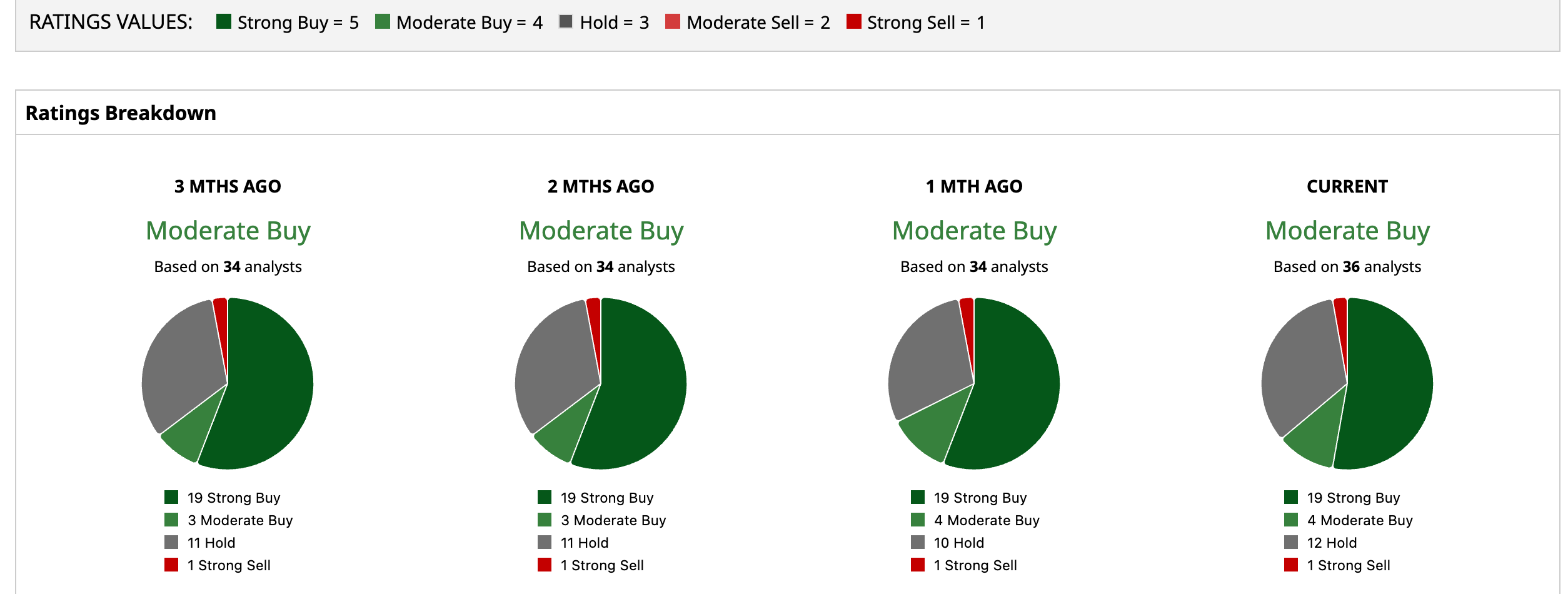

Of the 36 analysts covering COST stock, 19 have a “Strong Buy” rating, four have a “Moderate Buy” rating, 12 have a “Hold” rating, and one analyst has a “Strong Sell” rating, making for a consensus “Moderate Buy" rating. The mean target price of $1,101.25 implies potential upside of 16.5% from current levels. Meanwhile, the high price target of $1,315 implies as much as 39% possible growth from here.

Closing Thoughts

Costco’s combination of brand strength, recurring membership revenue, and growth strategy is difficult to ignore. If the company continues to perform as well as it has so far, COST could have more upside ahead — especially as investors look for businesses capable of delivering reliable growth in an uncertain market.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)