Alcoa (AA) stock came under immense pressure on Friday after the company posted disappointing Q2 earnings per share and lowered its full-year guidance for alumina production.

Management now expects to produce up to 9.6 million metric tons of alumina in 2026, down from its previous outlook for at least 9.7 million metric tons, due to operational bottlenecks at its Pinjarra refinery.

The muted quarterly release arrives at a time when Alcoa shares have already been out of favor with investors, currently down more than 45% versus its recent high.

What Made Alcoa Cut Its Production Guidance?

The downgrade stems from an organic compound outbreak in bauxite at the Pinjarra refinery in Australia, an issue exacerbated by gas supply disruptions tied to Cyclone Narelle.

For investors, it’s a subtle reminder that AA shares face weather-related risks as well.

While Alcoa delivered record quarterly revenue on the back of favorable commodity pricing, the production setback illustrates that strong market conditions alone cannot fully offset operational disruptions.

That said, AA currently pays a dividend yield of 0.89%, which makes it somewhat more attractive to own for income-focused investors.

Should You Load Up on AA Shares on the Dip?

Alcoa’s adjusted EPS miss, coming in at $2.12 versus expectations of $2.32, highlights the firm’s sensitivity to rapid commodity price swings.

Management attributed the shortfall to a sharp decline in aluminum prices at the tail end of June, compounded by a 15-day pricing lag that amplified the impact of the downturn.

This highlights how closely AA’s margins remain tied to “short-term” pricing volatility. Combined with higher Section 232 tariffs on Canadian imports, the company faces significant cost headwinds.

All in all, even as Alcoa pursues strategic expansion through the $5.5 billion South32 acquisition, its near-term profitability remains hostage to macroeconomic turbulence.

Wall Street’s View on Alcoa Stock

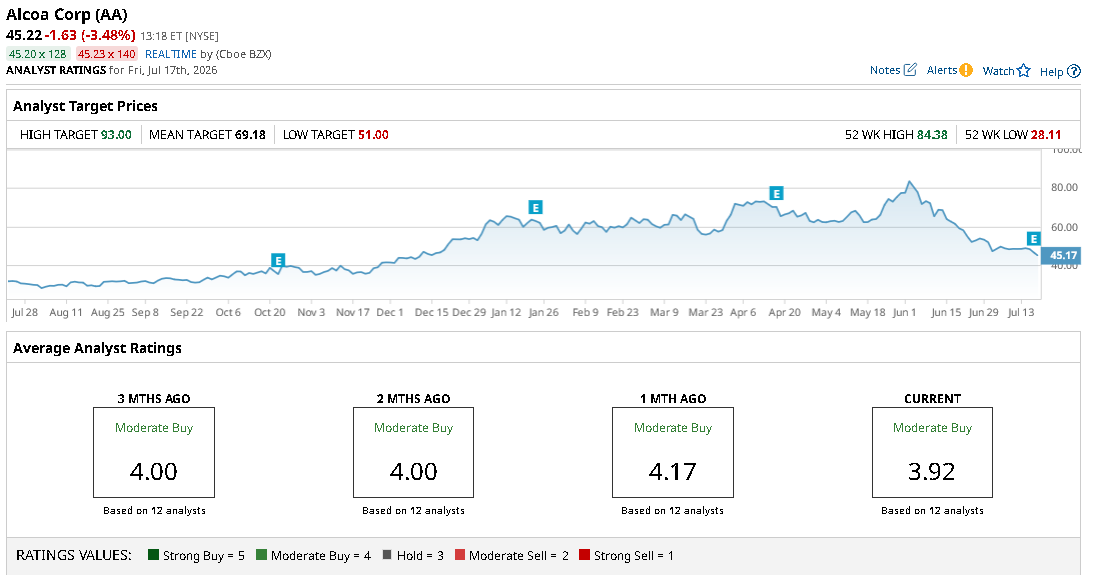

Heading into July 17, Wall Street had a consensus “Moderate Buy” rating on Alcoa stock, with a bullish mean price target of about $69.

However, it’s reasonable to expect at least some downward revisions in the weeks ahead as the analyst community incorporates the production cut Alcoa announced today in their estimates.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)