/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

Leading broker Wedbush has initiated coverage of social media platform Reddit (RDDT) with an “Overweight” rating and a price target of $250. This indicates a potential upside of 35% from current levels.

Citing multiple drivers of growth, such as better app quality, innovative products, and licensing deals with LLM developers such as Google's (GOOG) (GOOGL) Gemini and OpenAI's ChatGPT, Wedbush reckons Reddit is operating from a position of strength.

About Reddit

Founded in 2005, Reddit is one of the world's largest online discussion platforms and has evolved from a simple internet message board into one of the internet's most valuable repositories of human-generated conversations. Today, Reddit operates more than 100,000 active communities (subreddits) where users discuss virtually every topic imaginable, from investing and technology to sports, healthcare, gaming, and AI, among others.

With a market cap of $35.7 billion, RDDT stock is down 22% on a year-to-date (YTD) basis.

Reddit's Authentic Moat

Reddit's tagline is “The Heart of the Internet,” and this is where its biggest competitive advantage lies. While other social media platforms have evolved to become polished, influencer-led content hubs, sometimes far removed from reality, Reddit's audience base is led by authentic conversations generated by users with limited curation. The platform's anonymity drives this. While one can be anonymous on Instagram and Facebook, those users are not regarded as authentic or are increasingly referred to as “bots” by other users. However, in Reddit, anonymity is the core tenet.

Consequently, in the age of AI, this has opened up a significant revenue stream for the company—licensing its data to LLM developers. Based on the ones announced officially by the company, Reddit has deals with two of the largest LLM developers, Gemini and ChatGPT. While the expanded partnership with Gemini gives Google access to Reddit's Data API for AI model training and improved Reddit content discovery, the one with OpenAI is also on similar lines.

Notably, Reddit's vast repository of genuine human conversations is being reflected in its metrics, with revenue and advertising income continuing to expand at a much faster pace than the rate of user additions, pointing to enhanced monetization effectiveness and supporting the view that the platform remains significantly under monetized relative to its full potential.

And to realize that potential, Wedbush highlighted that Reddit Max and Dynamic Product Ads will be key.

Reddit Max, unveiled at CES in January 2026 and now in beta, is an automated campaign type that hands over targeting, creative selection, placement, and budget allocation to AI for the length of a 21-day run. What separates it from the black box automation on Meta (META) or Google is transparency, since Max opens up new reporting like Top Audience Personas that cluster viewers into groups.

On the other hand, Dynamic Product Ads handle the bottom of the funnel. Reaching general availability in 2025, they read on-platform and off-platform shopping signals to match items straight from an advertiser's catalog to the right Redditor at the right moment. The payoff is measurable, with advertisers running both DPA and standard conversion campaigns earning double the return on ad spend, and DPA delivering 94% higher returns as the models improved.

This is significant for growth, as Reddit users are unusually primed to buy: 77% use the platform during the consideration phase, and Redditors are 63% more likely than users of rival platforms to expect spending increases.

Coming to AI, Reddit Answers is the answer to other popular generative AI platforms. Unlike ChatGPT or Google's overviews that scrape the whole web, Reddit Answers pulls only from actual posts and comments made by redditors, so responses carry the lived experience and messy honesty that made people trust Reddit in the first place. That keeps users inside the app rather than bouncing to an outside tool, and it gives Reddit a way to monetize the very content that competitors are freely mining. Further, Reddit has rolled out AI-powered translations across a growing list of markets that directly widens the addressable audience.

However, heavy reliance on Google is a risk. Moreover, Reddit has licensing deals that bring in revenue, but those arrangements also help build the tools that may reduce the need to visit Reddit at all, which is an uncomfortable long-term tension.

Finances Thriving Just Like Its Communities

Reddit's numbers are impressive not just in engagement but also in its financials.

Q1 2026 saw the company reporting a beat on both revenue and earnings. Revenue grew at a considerable rate of 69% from the previous year to $663 million, with ad revenue seeing an even sharper increase of 74% in the same period to $625 million. For Q2 2026, the company expects revenue to be between $715 million and $725 million. Analysts are expecting $731 million.

Meanwhile, earnings shot up to $1.01 per share from just $0.13 per share in the prior year. It also came in much higher than the consensus estimate of $0.57 per share, marking the ninth consecutive quarter of earnings beat from the company.

Daily active users rose as well, by 17% on a year-over-year (YoY) basis to 126.8 million. Average revenue per user at $5.23 reflected a growth rate of 44%.

Cash from operations more than doubled to $312 million, with free cash flow showing almost identical growth rates to come in at $311 million. Overall, Reddit ended Q1 2026 with a cash balance of $1.37 billion, with short-term debt of just $7.2 million.

However, the slide in RDDT stock could not change its overvalued status. Its forward P/E, P/S, and P/CF of 27.77, 11.79, and 30.67 all have substantial gaps with the sector medians of 13.25, 1.18, and 7.98, respectively.

Analyst Opinion on RDDT Stock

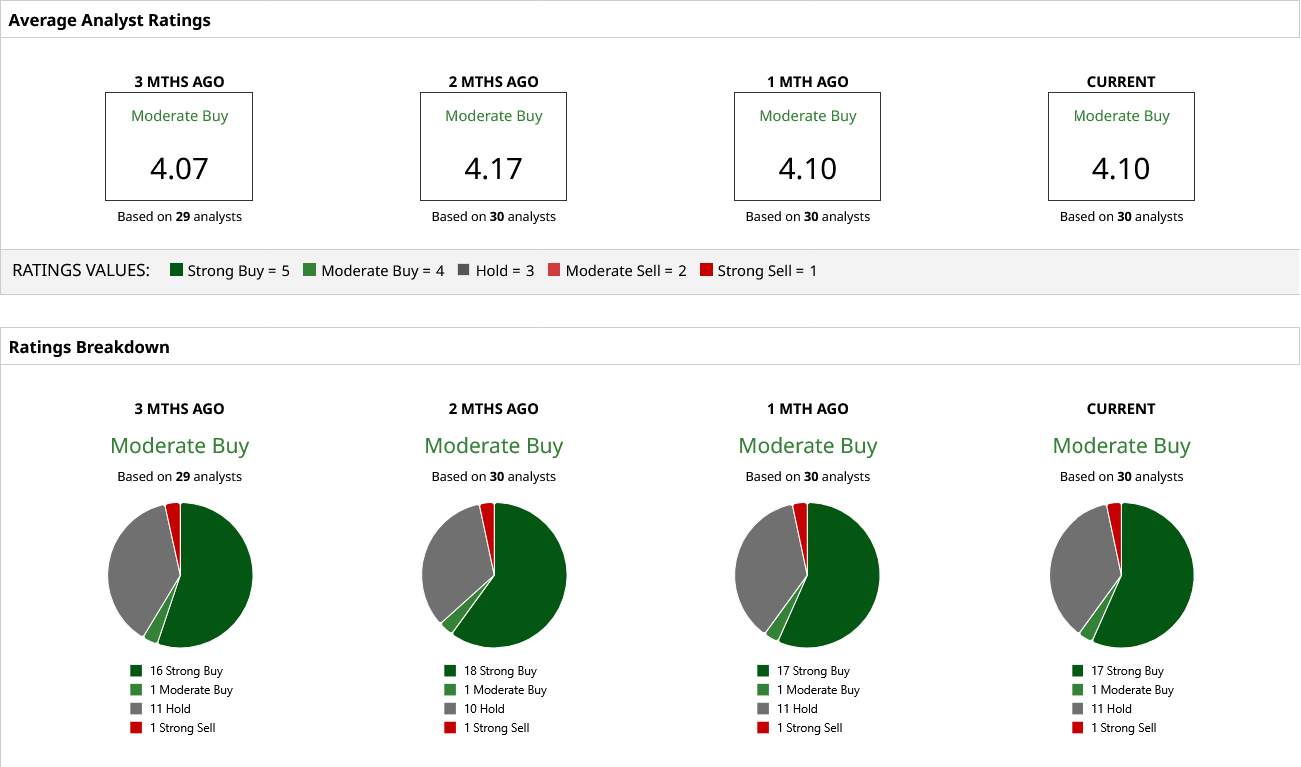

Thus, analysts remain guardedly hopeful about RDDT stock, with a “Moderate Buy” rating. The mean target price of $223.06 denotes an upside potential of about 25% from current levels. Out of 30 analysts covering the stock, 17 have a “Strong Buy” rating, one has a “Moderate Buy” rating, 11 have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)