Trade Today - By Eli Gal Levy - read the full brief HERE

The setup, the levels, and the session’s pressure points.

01 — THE 90-SECOND READ

The Data Gave the All-Clear; the Curve Refused to Sign It

REGIME Positive Gamma · Pinned in the Box

Tuesday’s S&P cash close of 7,543.59 sits about 66 points (0.87%) above the dealer gamma flip. Dealers dampen — but the put wall sits just below and the call wall just above, so the tape is pinned in a narrow box with a hawkish Chair due to speak inside it.

- The July hike is gone June CPI landed cool enough to end the argument that ruled last week: headline −0.4% m/m (the biggest monthly drop since 2020) took the annual rate to 3.5%, and core printed flat on the month for a 2.6% annual pace — the coolest since 2021. Odds of a July 29 hike collapsed from roughly two-in-five to 14–20%. Stocks took the win: the S&P closed +0.38%, the Nasdaq Composite +0.90%.

- But yields rose on the good news Here is the tell the equity tape is ignoring: on a downside inflation surprise, Treasury yields went up, not down — the 2-, 10- and 30-year all ticked +2–3bp, the long bond back to 5.124%. The bond market is not trading the print. It is trading what comes after it: a third straight up-day in oil, and a new Fed Chair with a hawkish reputation who testifies at 10:00.

- Warsh is the day, not the data The 8:30 PPI matters, but the catalyst with the fattest tail is Chair Warsh’s Senate Banking testimony at 10:00. At his June debut he called policy “not particularly restrictive” and stressed restoring price stability. With headline inflation falling while core stays sticky and oil re-rating higher, every sentence about the September path gets amplified — and the cool CPI just handed him room to hold without looking like he caused a selloff.

- Banks pass the baton Yesterday the money-center banks cleared roughly $49B in quarterly profit, up about 39% year-on-year on a trading-and-dealmaking surge. This morning Morgan Stanley and BlackRock report before the bell to extend it — BlackRock is already indicated +4.5% pre-market. The capital-markets cycle is not the thing that’s wobbling.

- The rotation matured, IBM bounced A day after its 25% collapse — its worst on record, on a preliminary Q2 miss and a customer budget shift toward AI infrastructure — IBM is bouncing +1%. The cohorts it disturbed are settling in place: semis and chip-tools stayed bid (Applied Materials +2.9%, Lam +2.6%), while the defunded software names steadied rather than extended. This is a tape digesting a rotation, not fighting one.

03 — CALENDAR & SCENARIO MAP

A Wholesale Inflation Print, Then the Chair

| Time (ET) | Event | Consensus | Prior |

|---|---|---|---|

08:30 | PPI final demand YoY (Jun) | ~6.4% | 6.5% |

08:30 | Core PPI MoM (Jun) | — | +0.3% |

| 08:30 | Empire State Mfg Index (Jul) | — | — |

| 08:45 | NY Fed Pres. Williams speaks | — | — |

10:00 | Chair Warsh — Senate Banking testimony | — | — |

| 14:00 | Fed Beige Book | — | — |

| 18:30 | St. Louis Fed Pres. Musalem speaks | — | — |

Retail sales and jobless claims are tomorrow; industrial production is Friday. Today’s hard data is PPI plus Empire State — and with cheap June gasoline already in the rear-view, wholesale inflation is a confirm, not a catalyst. The catalyst wears a witness badge.

Bank Kickoff — Round Two Reports This Morning

| Name | Pre-market | Read |

|---|---|---|

Morgan Stanleyreports BMO | +1.05% | Wealth + trading in focus after the money-centers’ blowout; SpaceX-driven fee upside a swing factor |

BlackRockreports BMO | +4.54% | Indicated sharply higher — the tape is pricing a beat and strong net flows before the print crosses |

Round one — the money-center banks — already cleared, and cleared big. The question this morning is whether the asset-gatherers and the wealth machine confirm that the capital-markets thaw is broad, not just a trading-desk windfall.

Binary 1 — June PPI08:30 ET · cons ~6.4% YoY · prior 6.5%

SOFT — IN LINE OR BELOW The disinflation confirm. A cool wholesale print stacks on top of yesterday’s CPI and hands Warsh cover to sound patient rather than pre-emptive. In this branch the positive-gamma pin holds, the front end stays bid, and the tape works the top of its box.

HOT — SERVICES/PIPELINE FIRM The uncomfortable branch: a firm core-goods or services PPI, arriving as oil re-rates, revives the “headline down, pipeline sticky” worry the bond market is already voicing. That is the read that lets yields keep rising on cool data — and it lands ninety minutes before the Chair speaks.

Binary 2 — Warsh Senate Banking Testimony10:00 ET · ~90 min after the print

DEFERS — PATIENT TONE If the Chair leans on the cool CPI and points to the September meeting, the hawkish-debut reputation gets softened and the market reads a hold as the base case. Sentiment is defensive enough (Fear at 44, bulls below average) that this branch has relief-rally fuel loaded beneath it.

REINFORCES — STILL RESTRICTIVE ENOUGH? The branch the tape is not hedging: a Chair who repeats that policy is “not particularly restrictive,” keeps September live, and treats one soft month as insufficient. Paired with rising yields and firm oil, that is how the “inflation scare is over” narrative reverses inside a single session — through the rates channel, not through fear.

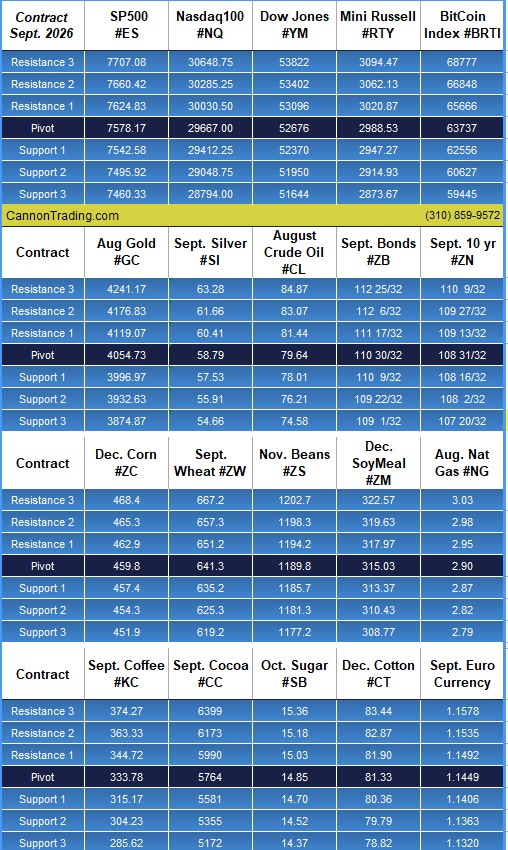

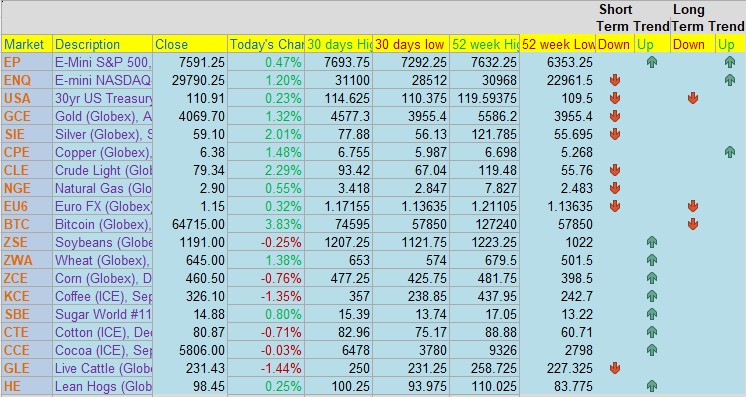

04 — PIVOT POINTS & GAMMA MAP

Levels & Structure

Good Trading,

Ilan Levy-Mayer, M.B.A

Vice President

Cannon Trading Co, Inc. Est. 1988

www.CannonTrading.com

Toll Free: 800-454-9572

Direct Line: (310) 858-6111

Margins / Commissions / Platforms / Professional Traders /Free Demo

Cannon Trading Co, Inc. a CFTC registered Independent Introducing Broker and NFA Member (NFA #0216708), 12100 Wilshire Blvd. Suite 1240, Los Angeles, CA 90025

Check Out Our Reviews

![]()

The finest compliment I can receive is a referral from a trusted client

*Trading commodity futures and options involves substantial risk of loss.

The recommendations contained in this letter is of opinion only and does not guarantee any profits. These are risky markets and only risk capital should be used. Past performance is not indicative of future results*

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)