/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

Arm Holdings (ARM) shares are in the spotlight on July 14 after senior HSBC analyst Frank Lee downgraded the British chip designer to “Hold,” citing “foundry capacity bottlenecks.” However, he raised his price objective on the Nasdaq-listed firm to $315, indicating potential upside of more than 10% from current levels.

Despite recent weakness, ARM stock remains a blockbuster performer for 2026, currently up 150% year-to-date.

HSBC’s Concerns Regarding Arm Stock

HSBC’s shift to a more neutral stance highlights a growing concern: ARM shares have run too far ahead of the company’s near-term financials.

In his research report, Lee admitted that the firm’s expansion into “merchant server CPUs” remains highly promising, but said the hype has already created a major valuation bubble.

At about 288x forward earnings, ARM is much more expensive to own than Nvidia (NVDA), with its valuation multiple leaving no room for operational errors or macro slowdowns.

According to Lee, while the long-term runway for AI chips is very real, the market has pulled years of future growth into the current price, capping further upside in the near term.

Arm Is Set to Post Earnings on July 29

HSBC recommends at least some caution in playing ARM stock ahead of the company’s quarterly earnings scheduled for July 29. Consensus is for it to record $0.18 in earnings per share (EPS), up 12.5% year-on-year.

While memory shortages could weigh on smartphone shipments and the royalty sales they generate for Arm, analyst Lee also notes that transitioning into designing custom server silicon is tied to significant execution risks as well.

That said, Barchart holds a “56% BUY” opinion on ARM, signaling technical momentum remains in favor of the firm at the time of writing.

Wall Street Remains Bullish on ARM Shares

Despite aforementioned concerns, other Wall Street analysts are sticking to their constructive view on ARM shares for the remainder of 2026.

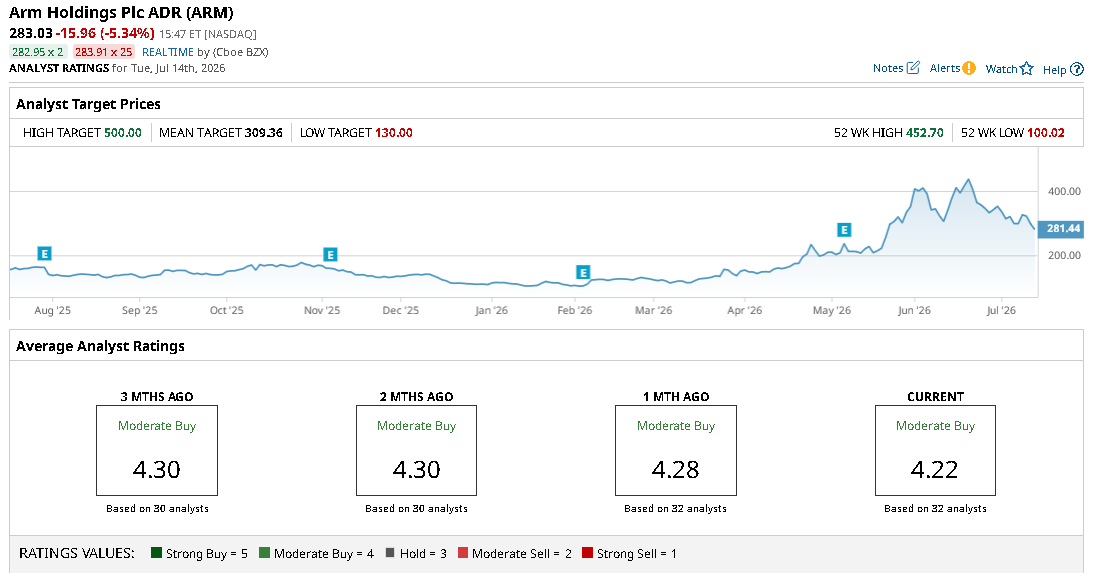

According to Barchart, the consensus rating on Arm Holdings remains at “Moderate Buy,” with the mean price target of about $309 suggesting potential for another 10% rally from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)