/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

Valued at a market cap of roughly $2.25 trillion, SpaceX (SPCX) owns and operates self-landing rockets, a satellite internet network that reaches nearly every corner of the planet, as well as a fast-growing artificial intelligence business.

However, one of Wall Street's respected independent research firms believes the space-tech stock is grossly overvalued and poised for a massive pullback.

Argus just issued its first-ever rating on SPCX stock. And the message underneath that rating is more complicated than a simple “buy” or “sell” call.

Argus Rating on SPCX Stock Signals Years of Price Adjustment Ahead

According to a report from Insider Monkey:

- Argus initiated coverage of Space Exploration Technologies with a “Hold” rating on June 26.

- Argus said SpaceX's IPO valuation implies a price-to-sales multiple near 95 times its 2025 revenue.

- A high multiple suggests investors are paying a steep premium today for growth that has not yet fully shown up in profits.

SpaceX is growing its top line rapidly but is yet to turn profitable. Argus described the company's operating plan as a mix of a mature infrastructure business and a venture-style growth bet.

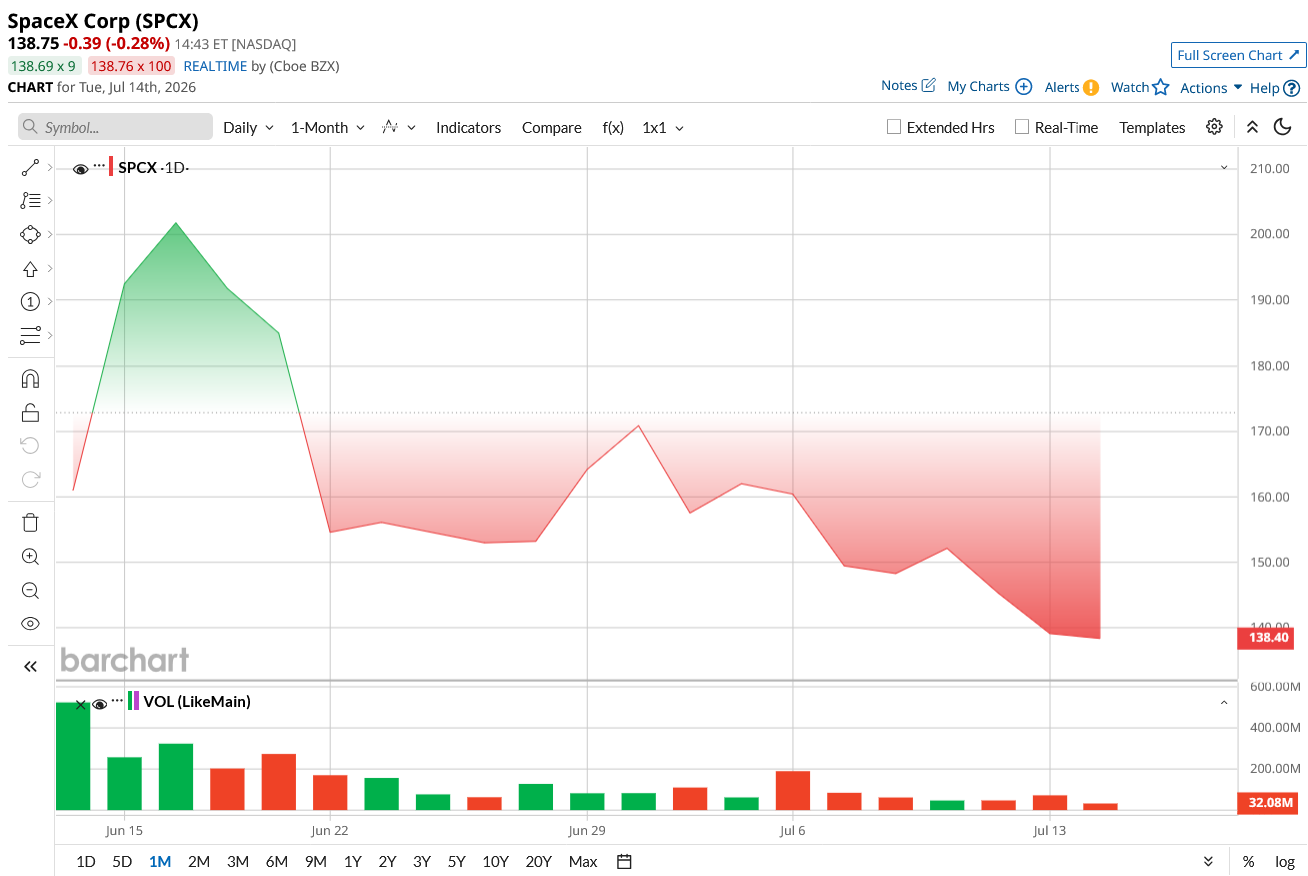

The investment firm also believes it could take years for SpaceX's valuation multiple to settle into a more normal range. Argus flagged volatility as a near-term risk, given SPCX stock slid more than 20% from all-time highs last week.

Shares have swung sharply since the debut, partly because relatively few shares are available to trade and partly because SpaceX was quickly added to several major stock indexes, according to Insider Monkey, a combination that amplifies price swings in both directions.

Argus said it would consider upgrading the stock if shares fall sharply for reasons unrelated to the business itself, or if revenue and earnings growth accelerate faster than expected.

What SpaceX Does and Why Investors Are Excited

SpaceX was founded in 2002 with a single goal: to make rockets reusable and cut the cost of reaching space.

SpaceX landed its first booster in 2015, while re-flying one in 2017. Chief Financial Officer Bret Johnsen said the Falcon 9 rocket can now carry 23 metric tons to orbit, and the newer Starship vehicle is approaching 100 metric tons of capacity.

That launch capability feeds two newer businesses.

- The first is Starlink, the company's satellite internet network. Johnsen said the network passed 10.3 million users by the end of the first quarter of 2026, more than double the user count from a year earlier, and now reaches over 164 countries.

- The second is artificial intelligence. SpaceX built a large data center called Colossus 2 and recently struck a hosting deal with Anthropic, along with a separate coding partnership with Cursor, a company that SpaceX is set to acquire for $60 billion.

SpaceX generated close to $19 billion in revenue last year, up more than 30% from the prior year, with almost $7 billion in adjusted earnings before interest, taxes, depreciation, and amortization.

The connectivity segment grew roughly 50% year over year. In the first quarter of 2026, the company posted about $5 billion in revenue, with connectivity contributing roughly $3 billion of that total.

Morningstar Sees an Even Steeper Gap Between Price and Value

Argus is not the only firm raising a flag. Morningstar published its own pre-IPO analysis and landed on a far more cautious number.

Morningstar equity analyst Nicolas Owens valued SPCX at $63 per share, roughly 53% below the IPO price, and assigned the stock a “Narrow” economic moat rating. The analyst model builds three possible futures for SpaceX's AI business, ranging from “modest” to a “Moonshot” scenario, as Morningstar calls it.

That top scenario requires two things that do not exist yet: a rapidly reusable Starship rocket and commercially competitive data centers built in orbit. Morningstar does not expect either technology to be proven out before 2028, even under generous assumptions.

Only in that best-case future does Morningstar's valuation approach $154 per share, and the firm assigns that outcome just a 7% probability. Morningstar noted that SpaceX's established space and connectivity businesses, which carry far less uncertainty, are worth roughly $40 per share on their own.

Everything above that, in Morningstar's view, is investors paying an option premium of about $72 per share for ambitions that have not yet been proven, including ideas like chip manufacturing and Mars colonization.

What Next for SPCX Stock Investors

Put together, Argus and Morningstar are telling a similar story from different angles. SpaceX has built businesses that are challenging to copy, and the growth numbers back that up. But the current stock price already assumes several difficult engineering breakthroughs will happen on schedule, and both firms think that assumption is a stretch.

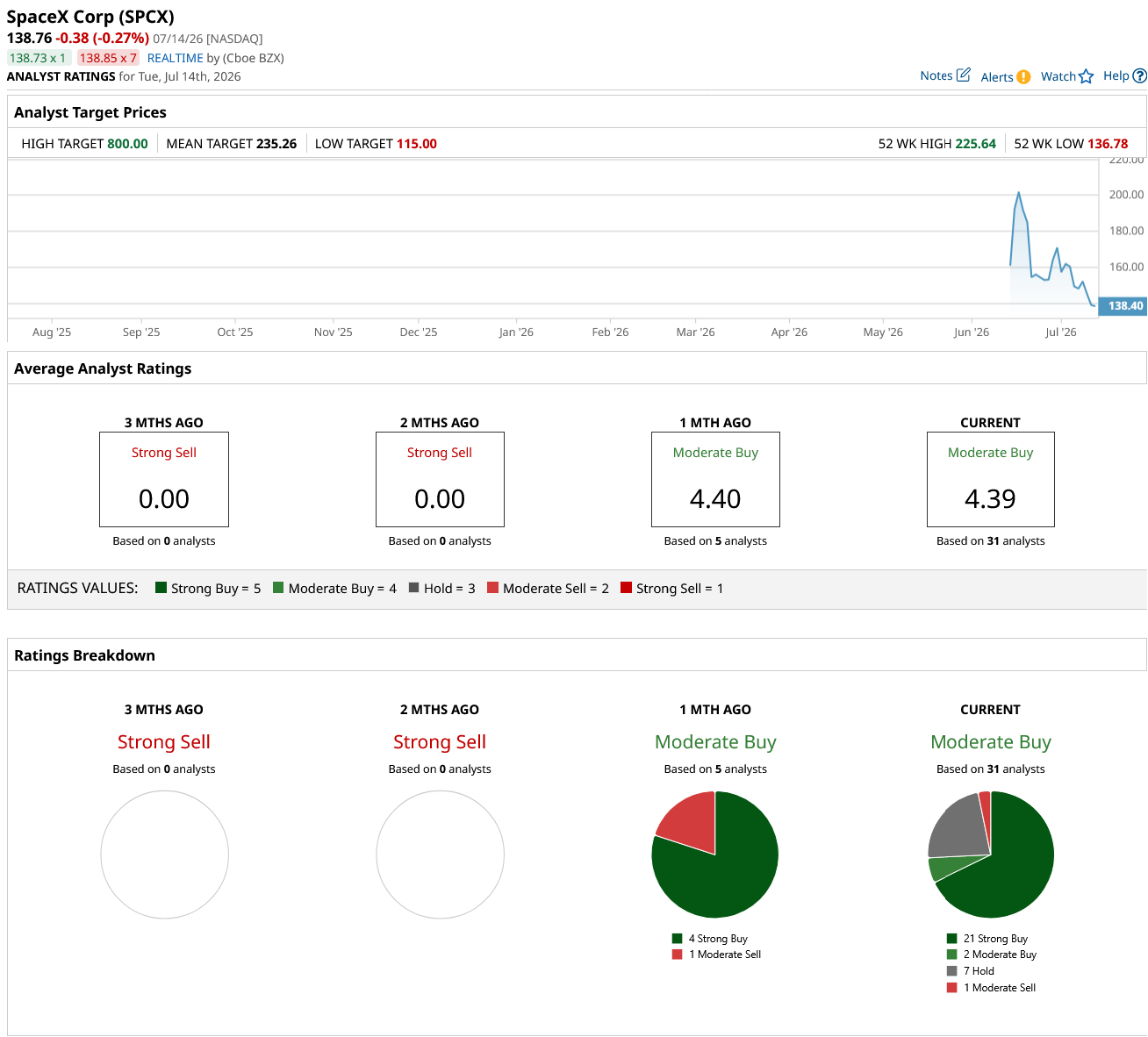

Out of the 31 analysts covering SPCX stock, 21 recommend “Strong Buy,” two recommend “Moderate Buy,” seven recommend “Hold,” and one recommends “Moderate Sell.” The average SPCX price target is $235.26, above the current price of about $134.

Anyone owning SPCX stock should brace for a bumpy multiyear stretch as the market figures out how much of SpaceX's AI ambition is still a bet on the future.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.