/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

SoFi Technologies (SOFI) will release its second-quarter earnings on Wednesday, July 29. After spending much of the year under pressure, SoFi shares have staged a notable comeback, climbing more than 10% over the past month. Even so, the stock remains down more than 30% year-to-date (YTD), leaving plenty of room for a recovery if the company delivers another strong quarter.

The key catalyst for SOFI stock would be a reacceleration in its non-lending businesses. Strong execution in these segments, along with upbeat guidance, could push the stock higher.

With this background, here's what investors should expect from SoFi's second-quarter results.

SoFi Q2 Earnings: Key Trends to Watch

While the slowdown in SoFi's non-lending business has weighed on its stock price, the financial technology company’s overall growth outlook remains strong. Strong member additions, rising product adoption, expansion of fee-based businesses, and continued strength in the Lending arm could help SoFi deliver another solid quarter.

SoFi has been growing its member base at a solid pace. For instance, in Q1, SoFi added 1.1 million new members, increasing total members by 35% year-over-year (YoY) to 14.7 million. This momentum is likely to continue in Q2, as management is forecasting at least 30% YoY member growth in 2026.

Further, much of the adoption of newer financial products will once again come from its existing members. This cross-selling strategy enhances customer lifetime value while reducing customer acquisition costs, supporting long-term profitability.

A key concern heading into the quarter is the loss of a major client in SoFi's Technology Platform business, which is expected to weigh on non-lending revenue.

However, the company's rapidly expanding Financial Services segment should help offset some of that weakness.

Higher customer spending through SoFi Money and credit card products, rising brokerage fee income, and continued strength in the Loan Platform Business (LPB) are expected to support non-lending revenue growth.

The LPB remains particularly attractive because it generates fee income without requiring SoFi to hold loans on its balance sheet, making it a highly capital-efficient business.

During the first quarter, SoFi facilitated the sale or transfer of $3.8 billion in personal and home loans while securing an additional $3.6 billion in funding commitments from three new partners. These agreements significantly expand the platform's lending capacity and strengthen its future revenue pipeline.

Despite the growing importance of fee-based businesses, lending is expected to remain SoFi's largest revenue contributor.

Healthy demand for personal, student, and home loans should continue to support lending revenue. Meanwhile, ongoing deposit growth provides a lower-cost funding source, helping improve net interest margins and profitability.

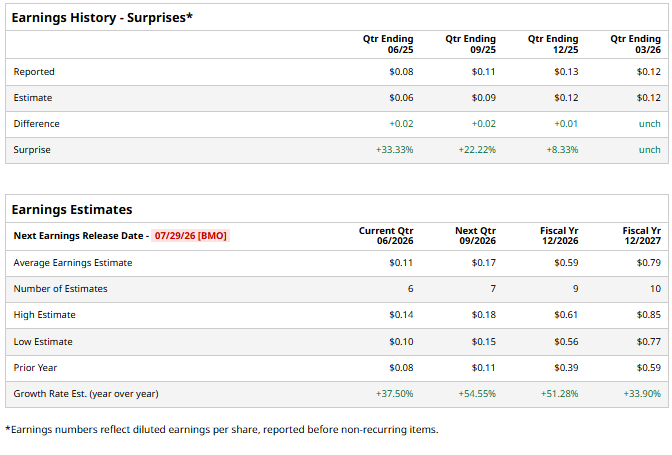

For the second quarter of 2026, management is targeting approximately 30% YoY adjusted net revenue growth. SoFi expects adjusted earnings per share (EPS) of $0.10 to $0.11, while Wall Street analysts currently forecast EPS of $0.11.

Is SOFI Stock a Buy?

A strong second-quarter report and solid outlook for non-lending revenues could mark an important turning point for SoFi Technologies. While concerns around the Technology Platform business amid the loss of a key client remain valid, the company's broader growth story appears intact.

SoFi continues to benefit from rapid member growth, increased product adoption among existing customers, and the expansion of its high-margin, fee-based businesses. Meanwhile, its lending business remains resilient, supported by healthy loan demand and a steadily expanding low-cost deposit base that continues to fuel earnings and cash flow.

Looking ahead, the company's ongoing investments in product innovation and brand awareness could provide an additional catalyst for growth in the second half of 2026, further strengthening its competitive position.

Overall, SoFi is well-positioned to deliver solid growth, supporting a bullish investment thesis. While Wall Street analysts currently maintain a “Hold” consensus rating on the stock, SoFi's improving fundamentals indicate the shares offer an attractive opportunity for investors with a longer-term horizon.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.