Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Golar LNG (NASDAQ:GLNG) and the best and worst performers in the infrastructure industry.

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

The 9 infrastructure stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 13.4%.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

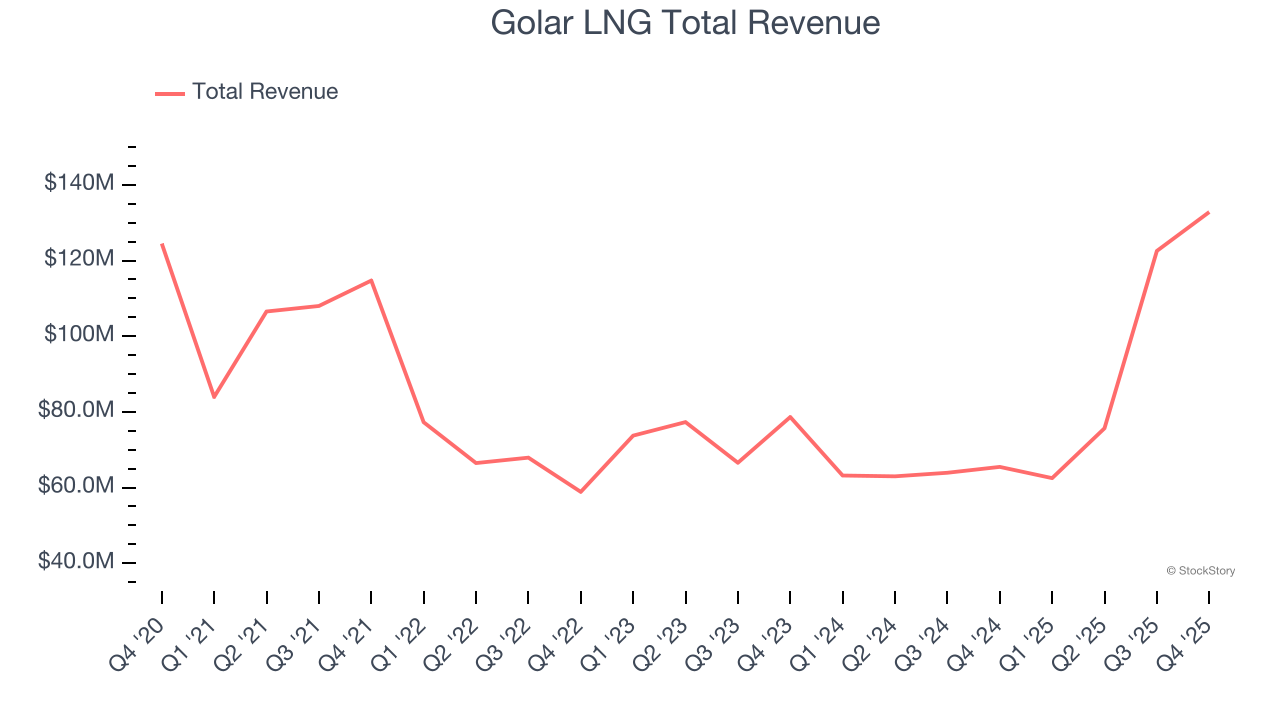

Weakest Q4: Golar LNG (NASDAQ:GLNG)

Pioneering a way to monetize stranded gas reserves that would otherwise be uneconomical to develop, Golar LNG (NASDAQ:GLNG) converts ships into floating liquefied natural gas facilities that liquefy natural gas at offshore sites.

Golar LNG reported revenues of $132.8 million, up 103% year on year. This print exceeded analysts’ expectations by 1.2%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EPS and EBITDA estimates.

Golar LNG achieved the fastest revenue growth but had the weakest performance against analyst estimates of the whole group. Unsurprisingly, the stock is up 16.7% since reporting and currently trades at $52.35.

Read our full report on Golar LNG here, it’s free.

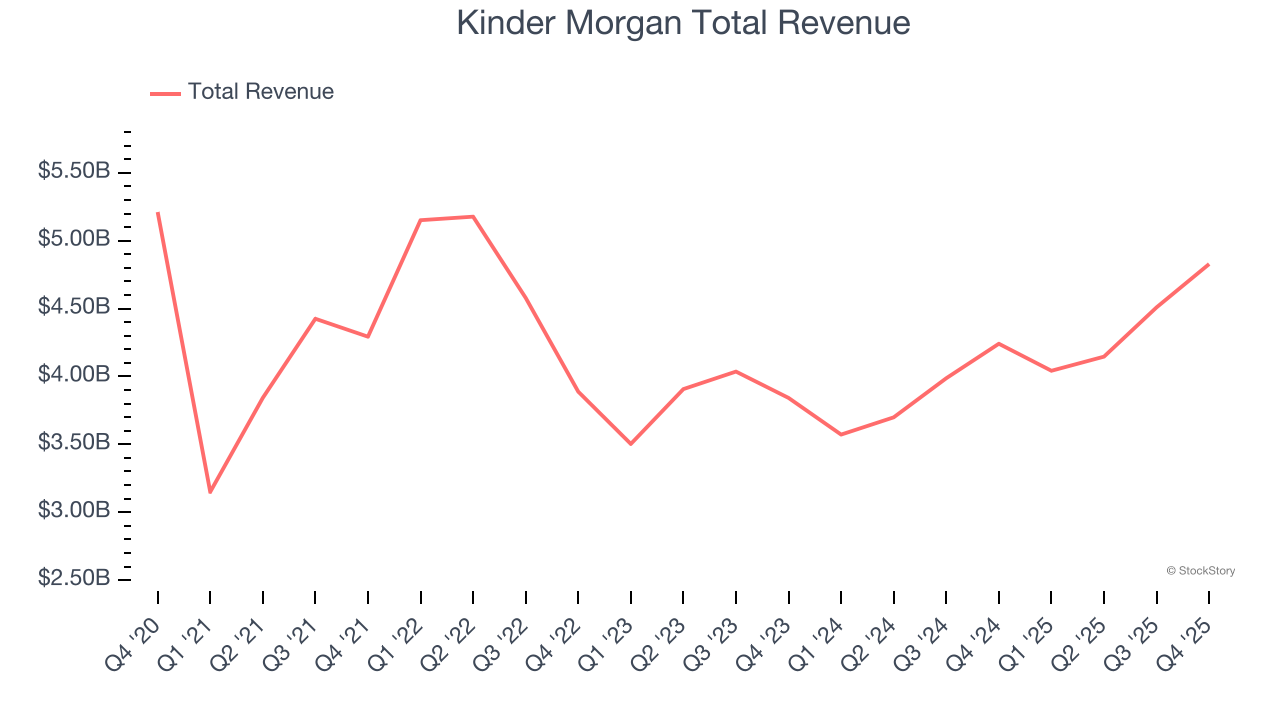

Best Q4: Kinder Morgan (NYSE:KMI)

Operating what amounts to the toll roads of the energy industry, Kinder Morgan (NYSE:KMI) transports natural gas, refined petroleum products, and crude oil through its pipeline network across North America.

Kinder Morgan reported revenues of $4.83 billion, up 13.8% year on year, outperforming analysts’ expectations by 3.3%. The business had a stunning quarter with a beat of analysts’ EPS estimates.

The market seems content with the results as the stock is up 1.5% since reporting. It currently trades at $32.29.

Is now the time to buy Kinder Morgan? Access our full analysis of the earnings results here, it’s free.

Genesis Energy (NYSE:GEL)

Operating a 64% stake in the Poseidon Pipeline, one of the Gulf of Mexico's largest crude oil pipelines, Genesis Energy (NYSE:GEL) provides midstream services like pipeline transportation, storage, and processing for crude oil and natural gas producers and refiners.

Genesis Energy reported revenues of $446.6 million, up 12.1% year on year, exceeding analysts’ expectations by 11.4%. Still, it was a slower quarter as it posted a significant miss of analysts’ EPS and EBITDA estimates.

As expected, the stock is down 10.6% since the results and currently trades at $14.68.

Read our full analysis of Genesis Energy’s results here.

DHT Holdings (NYSE:DHT)

With each vessel capable of carrying roughly 2 million barrels of oil—enough to fill about 125 Olympic swimming pools—DHT Holdings (NYSE:DHT) operates very large crude carriers that transport crude oil across international routes for energy companies and traders.

DHT Holdings reported revenues of $157.4 million, up 97.4% year on year. This print surpassed analysts’ expectations by 3.8%. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS and EBITDA estimates.

The stock is down 8.3% since reporting and currently trades at $17.51.

Read our full, actionable report on DHT Holdings here, it’s free.

Calumet (NASDAQ:CLMT)

With roots dating back to 1919 and facilities strategically positioned from Louisiana to Montana, Calumet (NASDAQ:CLMT) refines crude oil into specialty products like lubricating oils, solvents, and waxes used in cosmetics, batteries, and industrial applications.

Calumet reported revenues of $1.03 billion, up 3.6% year on year. This number topped analysts’ expectations by 8%. Taking a step back, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a significant miss of analysts’ EBITDA estimates.

Calumet had the slowest revenue growth among its peers. The stock is up 15.8% since reporting and currently trades at $40.06.

Read our full, actionable report on Calumet here, it’s free.

Market Update

Over the past year, investors have been forced to repeatedly answer the same question: what is the market’s biggest risk? The answer has changed several times, and each shift has reshaped market leadership.

Late in 2025 and early 2026, artificial intelligence became the market’s primary uncertainty. Investors questioned whether AI would erode software pricing power and weaken competitive moats as AI made it easier to replicate once-differentiated products.

By the spring, technology took a back seat to geopolitics. The U.S. conflict with Iran briefly became the market’s dominant narrative, raising concerns about oil prices, inflation, and global growth. But as energy markets remained orderly and fears of a prolonged supply disruption faded, investors quickly turned their focus back to fundamentals.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)