/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)

Spire Global (SPIR) just checked off another important milestone in its growth strategy.

On July 8, the company confirmed that it successfully deployed 10 new satellites aboard SpaceX’s (SPCX) Transporter-17 mission, marking its third satellite launch of 2026. While the launch itself was widely expected and barely moved SPIR stock on the day, it represents another step in expanding Spire’s satellite constellation and turning customer backlog into revenue-generating assets.

For investors, that's the bigger story. Every satellite that reaches orbit strengthens Spire's ability to collect weather, maritime, aviation, and radio-frequency data for customers across government and commercial markets. If management executes as planned, the larger constellation could support stronger contract wins and higher recurring revenue over the coming quarters.

Spire Global Stock Has Been Volatile, But Investors Remain Focused on Growth

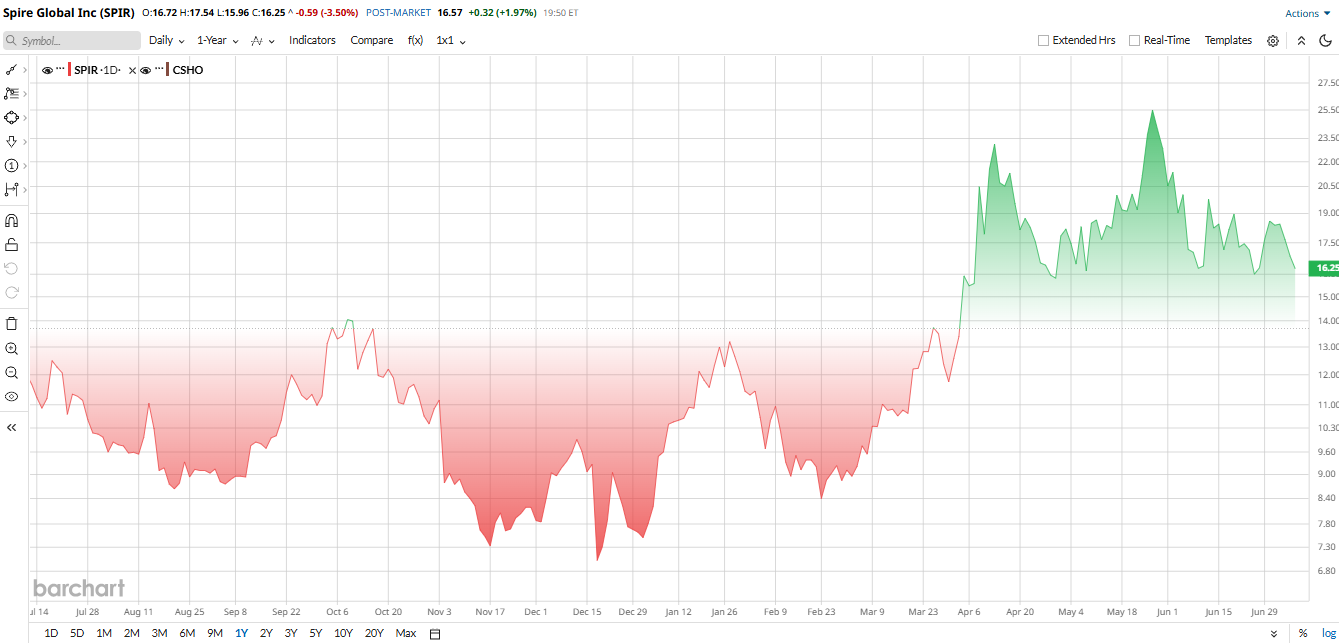

Spire Global shares have experienced a dramatic ride over the past year. SPIR stock has climbed roughly 122% from lows near $6.60, although shares are still below the 52-week high of $25.93. Investors rewarded the company after it strengthened its balance sheet by selling its maritime business, reduced debt, secured major government contracts, and raised $70 million through private financing earlier this year.

Despite those gains, the stock has cooled over the last few months alongside weakness across many tech names. Shares are up 96% year-to-date (YTD) but down 32% for the past three months.

From a valuation perspective, Spire still appears relatively inexpensive compared with many aerospace peers. The stock trades at a trailing price-to-earnings (P/E) ratio of roughly 10 times, which sits comfortably below the industry average. Although its price-to-sales (P/S) ratio remains elevated at 8.7 times because of its relatively small revenue base, investors are not paying an aggressive earnings multiple for future growth.

The Satellite Launch Adds to Several Expansion Initiatives

The Transporter-17 mission was more than just another routine launch. Spire deployed 10 satellites, including satellites monitoring methane emissions for GHGSat, satellites for a number of commercial customers, and one satellite to replace one from Spire's own constellation. The successful deployment boosts the company's capability for delivering subscription models of Earth observation and analytics.

The growth plan is also accompanied by other efforts from the satellite expansion.

Earlier this year, Spire established a new satellite manufacturing plant in Munich, Germany, which can manufacture around 100 satellites per year. The company also pledged alliances with Schaeffler (SFFLY) for the production of satellite hardware and signed a memorandum with Diehl Defence in the area of missile-warning technology. At the same time, Spire has been making further investments in its software and analytics services, recently launching a new model on its Cirrus platform with an advanced forecasting tool. These factors are all proof that Spire is evolving from a company that just launches satellites to a company that does all three: manufacturing, defense, and advanced data services.

Spire Reports Q1 Earnings

Spire's first-quarter results came ahead of Wall Street's estimate. During Q1 2026, revenue came in at $15.8 million, down about 34% from the prior year because of last year's maritime business divestiture. Excluding that business, however, revenue increased roughly 13%, reflecting continued growth across the company's core operations.

The company reported a net loss of $25.8 million, compared with a loss of $23.5 million a year earlier, while GAAP earnings came in at a loss of approximately $0.78 per share. Cash used in operations totaled $26.2 million, leaving Spire with roughly $49.5 million in cash and marketable securities at quarter-end.

Management nevertheless maintained its full-year outlook, projecting 2026 revenue between $75 million and $85 million while forecasting an adjusted loss of approximately $0.79 to $0.93 per share. Those projections remain broadly in line with Wall Street's expectations, as management expects newly deployed satellites to contribute more meaningfully to revenue growth during late 2026 and into 2027.

What Do Analysts Think of SPIR Stock?

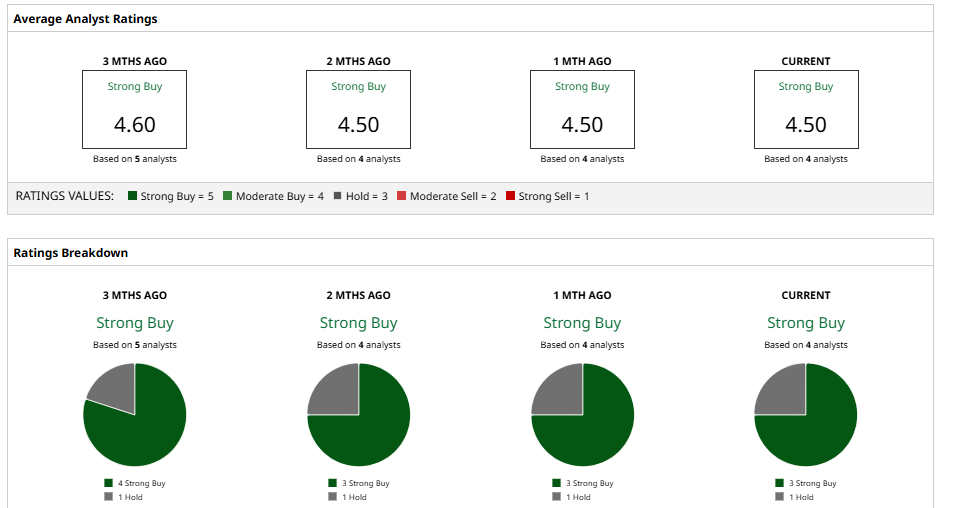

In the longer term, Wall Street still has a captive audience for Spire.

In June, Stifel maintained its “Buy” rating and raised its price target to $24, believing that the company's continued progress in reducing operational risk alongside steady execution and an expanding backlog proves its analysis. H.C. Wainwright also kept a “Buy” rating and raised its target to $19, citing Spire's balance sheet and growing demand in the government for space-based solutions.

However, the wider consensus among analysts is more conservative. The median price target is $20.88 per share, indicating potential upside of 42% from current levels, but the market isn't overly positive about the price prospects for the near future.

This leaves investors with one thing from which they can't turn away. Launching satellites is an important step, but making those satellites a long-term source of margin improvement — and eventually a profitable business — will determine whether or not Spire can ultimately justify being worth a higher valuation in the long term.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)