/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

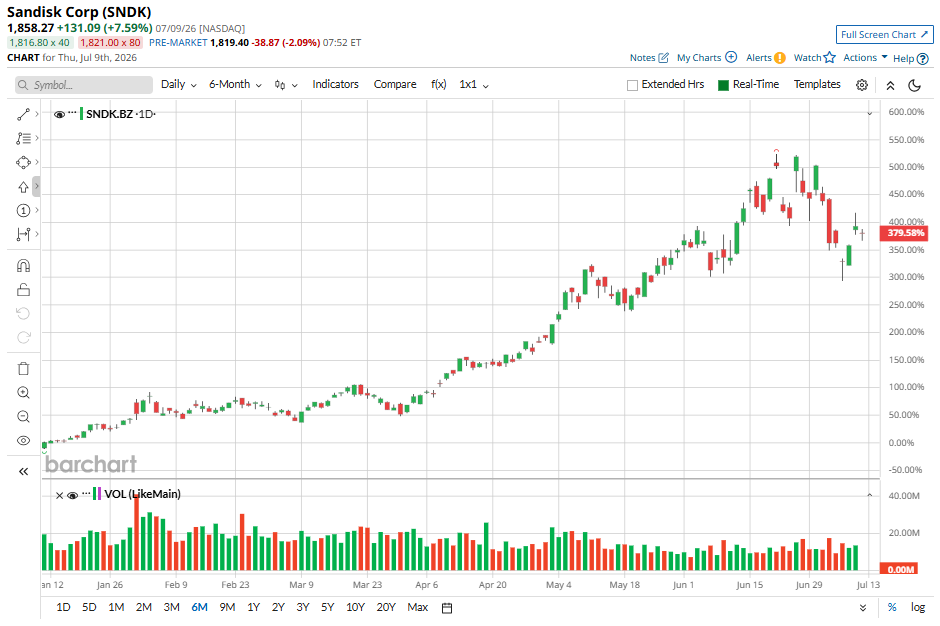

After an explosive rally, Sandisk (SNDK) stock has pulled back roughly 19% from its 52-week high. This provides investors with an opportunity to buy shares at an attractive valuation.

While SNDK stock has pulled back, the company's underlying business remains solid. Surging demand for high-performance storage solutions, improving pricing trends, and favorable industry tailwinds suggest Sandisk's growth story remains intact.

Sandisk Delivered a Blockbuster Q3 as Pricing Fueled Growth

Sandisk has been growing revenue and earnings at a solid pace, supported by higher pricing and volume. In the third quarter, surging NAND flash prices and booming AI-driven storage demand powered record revenue growth and significantly stronger profitability.

Third-quarter revenue jumped 251% year-over-year (YOY) to $5.95 billion, driven primarily by a 248% increase in average selling price (ASP) per gigabyte. The sharp rise in pricing reflects a favorable supply-demand environment for NAND flash memory.

The biggest growth driver was Sandisk's data-center business, where revenue soared 645% YOY. The segment benefited from a 186% increase in ASP. Momentum also extended beyond data centers. Revenue from the edge business climbed 295%, as stronger pricing more than offset modest shipment declines. Meanwhile, consumer revenue increased by 44%, demonstrating resilient demand despite lower shipment volumes, with higher selling prices more than offsetting weaker unit sales.

Profitability improved even faster than revenue. Sandisk's adjusted gross margin expanded to 78.4% in Q3 from 51.1% in the previous quarter, reflecting leverage from rising NAND prices and an improving product mix.

Looking ahead, management expects industry supply-demand dynamics to remain favorable through 2026 and beyond. With artificial intelligence (AI) infrastructure spending continuing to accelerate and NAND pricing remaining solid, Sandisk appears well-positioned to sustain margin expansion and deliver further earnings growth in the coming quarters.

AI Demand, NBMs Create a Strong Growth Foundation

SNDK stock is benefiting from one of the strongest memory market environments in years, as accelerating AI infrastructure spending is driving demand for high-performance NAND flash storage. Hyperscalers and enterprises are expanding AI data centers, while a tighter industry supply is supporting stronger memory pricing. This has created a favorable operating backdrop for the company.

However, Sandisk's long-term investment case extends beyond the current upcycle. The company is reshaping its business with new business models (NBMs) built around multiyear supply agreements that aim to deliver more predictable revenue and reduce the earnings volatility that has historically defined the memory industry.

These long-term contracts replace the traditional spot-market approach, securing committed customer demand over several years. Greater visibility allows Sandisk to plan production more efficiently, improve factory utilization, and reduce the risk of excess capacity during weaker market conditions, supporting steadier revenue and margins.

The strategy is already gaining traction. During Q3, Sandisk signed three multiyear agreements representing approximately $42 billion in minimum revenue commitments backed by financial guarantees. Some contracts run for as long as five years and include provisions that allow commitments to grow as customers increase purchasing volumes.

As AI-driven storage demand continues to expand, Sandisk's shift toward long-term agreements could make the business more resilient, less cyclical, and better positioned for sustained earnings growth.

Sandisk Stock Appears Undervalued

SNDK stock still looks remarkably undervalued despite the company's solid growth outlook. As its earnings continue to accelerate, the current valuation leaves plenty of room for upside.

Sandisk trades at just 9.6 times forward earnings, which is too low for a company expected to deliver explosive profit growth. Wall Street analysts forecast EPS to surge 181% in fiscal 2027, following another year of exceptional earnings growth in fiscal 2026.

What's Next for Sandisk Stock?

Sandisk appears well-positioned to benefit from surging AI-driven demand for high-performance storage, a favorable pricing environment, and its strategic move toward multiyear supply agreements, which could improve revenue visibility and profitability.

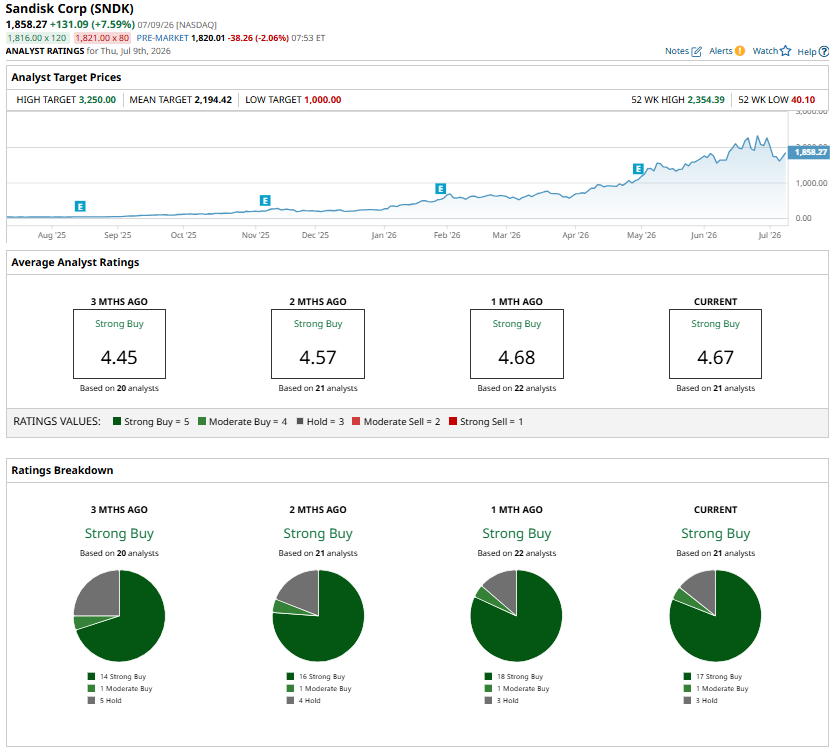

Despite these tailwinds, SNDK stock continues to trade at an attractive valuation, suggesting further upside potential. Adding to the bullish outlook, Wall Street analysts maintain a “Strong Buy” consensus rating. Taken together, these factors make Sandisk an appealing stock for investors seeking attractive long-term returns.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.