/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

Nvidia's (NVDA) dominance in artificial intelligence (AI) chips is facing a new challenge, and this time it's coming from one of its biggest international markets. According to a new Bloomberg survey of Chinese tech companies, businesses in China expect to allocate nearly half of their AI accelerator budgets to domestic chipmakers over the next year. That represents a sharp increase from roughly 30% today and signals that local companies are becoming increasingly willing to replace Nvidia hardware with homegrown alternatives.

This change comes as China's government moves toward a new direction of self-reliance in the semiconductor industry. Despite Nvidia's dominance as the top global provider for building AI accelerators, the figures from Bloomberg indicate that China may become an even more challenging market in the future, which could potentially curtail one of Nvidia's key long-term growth avenues.

Nvidia Stock Cools as Investors Weigh China Risks

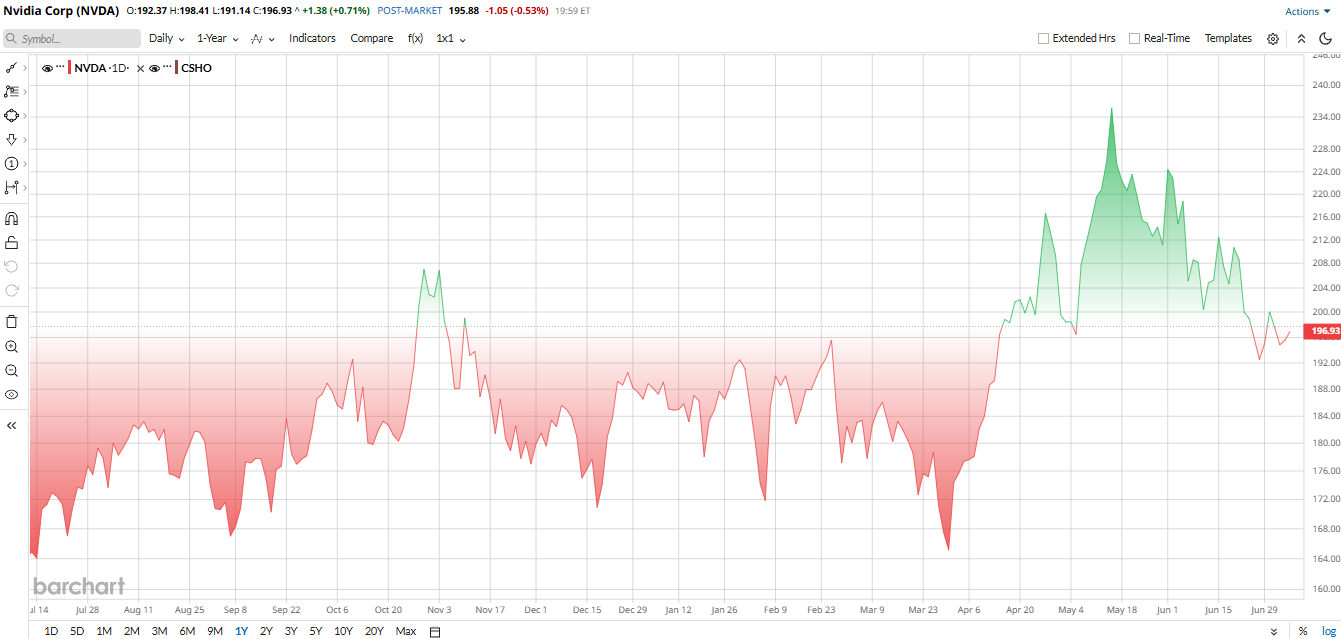

The survey comes at a time when Nvidia shares have already lost some momentum. After reaching record highs near $236 in mid-May, NVDA stock has pulled back to roughly $209. Even so, Nvidia remains up 12% year-to-date (YTD), slightly underperforming the broader S&P 500 ($SPX).

The recent weakness reflects growing concerns that export restrictions, rising domestic competition in China, and increasingly difficult comparisons after several blockbuster quarters could slow the company's extraordinary growth rate.

At the same time, investors continue to recognize Nvidia's unmatched position in AI infrastructure. The company still controls an estimated 70% to 85% of the global AI GPU market, while demand from hyperscale cloud providers, enterprise customers, and sovereign AI projects remains exceptionally strong.

Nvidia Continues Delivering Exceptional Financial Results

Despite growing concerns surrounding China, Nvidia's financial performance remains extraordinarily robust. The company reported outstanding first-quarter fiscal 2027 results, with revenue climbing 85% year-over-year (YOY) to $81.6 billion and increasing 20% sequentially.

The Data Center business once again drove nearly all of the growth, with revenue surging 92% YOY to $75.2 billion as enterprise AI deployments continued accelerating. Gross margin remained close to 75%, while net income climbed to $58.3 billion, producing EPS of $2.39. Adjusted earnings reached $1.87 per share, up roughly 140% YOY.

Cash generation also remained impressive. Nvidia produced approximately $50.3 billion in operating cash flow and roughly $48.6 billion in free cash flow during the quarter. The company also continued rewarding shareholders by returning nearly $20 billion through dividends and share repurchases while also authorizing an additional $80 billion stock buyback program.

Looking ahead, management guided Q2 revenue of approximately $91 billion, assuming virtually no AI data-center revenue from China, suggesting Nvidia already expects geopolitical restrictions to remain a headwind.

Nvidia Keeps Expanding Its AI Ecosystem Beyond GPUs

While investors focus on China, Nvidia continues investing aggressively across the broader AI ecosystem.

Earlier this year, the company unveiled its next-generation Vera Rubin AI platform while expanding partnerships designed to strengthen its position in hyperscale data centers.

Nvidia also continues building its enterprise AI software ecosystem, recently investing in AI security company Verkada and strengthening its enterprise sales organization.

Moreover, Nvidia believes its existing Blackwell and Rubin product families provide several years of runway as global AI infrastructure spending continues to expand.

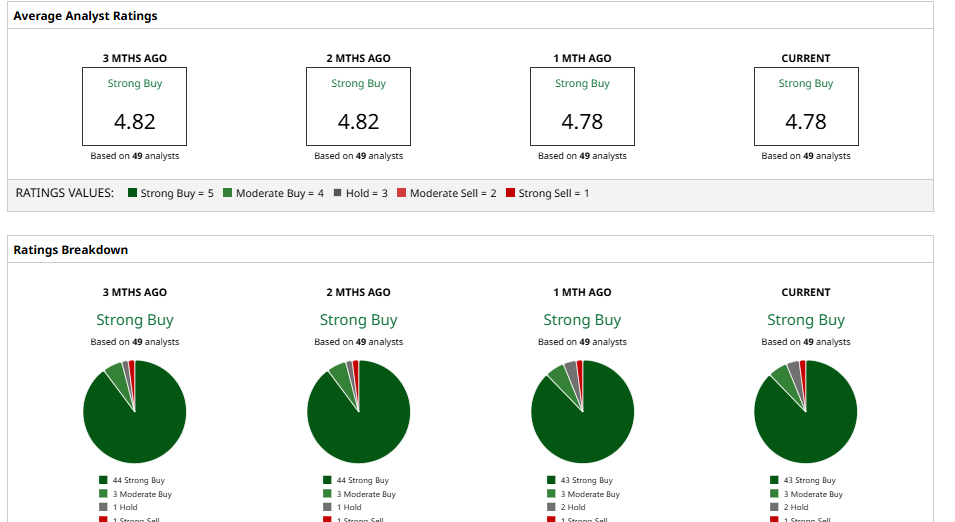

Wall Street Remains Overwhelmingly Bullish on Nvidia

Wall Street continues to be long on Nvidia's plans and projections. In a recent note, Morgan Stanley restated its $288 price target for NVDA stock, citing Nvidia's market-leading position, software, and value proposition among AI processor companies.

Meanwhile, Goldman Sachs remained bullish on the company with a $285 price target and “Buy” rating. Bank of America also recently upped its target to $350, establishing NVDA stock as a top semiconductor pick as AI gains broader usage industry-wide.

Overall, analysts continue to rate Nvidia stock as a consensus “Strong Buy." The average 12-month price target of $302.55 implies roughly 44% potential upside from current levels.

With the Bloomberg survey obviously raising new questions for Nvidia about its future in China, the U.S. semiconductor firm is already subject to intense backlash from domestic Chinese businesses. Yet, the majority of analysts feel that Nvidia will be able to more than compensate for any slowed growth in one market due to its dominant position in other areas, such as AI systems across hardware, software, and networking solutions.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)