Bloom Energy (BE) shares have been trending downward since July 8, following an investigative short report published by Hunterbrook Media. Bloom Energy has since responded, denying the claims in the report.

As investors reacted to allegations questioning the company’s production claims and critical supply chains, BE inched closer to its 100-day moving average (MA), with a decisive break below $222 expected to accelerate bearish momentum.

Despite the recent decline, Bloom Energy stock remains a blockbuster performer for 2026, currently up more than 170% versus the start of this year.

What Hunterbrook Alleged in Its Short Report

Hunterbrook’s report focuses intensely on BE’s heavy reliance on scandium — a rare earth element critical for its solid oxide fuel cells.

Despite management’s repeated public claims of having “no China supply chain,” global trade data and corporate filings allegedly trace multiple Chinese routes directly into Bloom’s production lines.

Moreover, the report cast strong doubt on BE’s capability to hit Wall Street’s 5-gigawatt production expectations, arguing that the firm’s massive requirements outstrip total projected global scandium supply.

Hunterbrook also targeted Bloom's financial transparency, claiming a severe mismatch between its unaudited $20 billion backlog and its actual performance obligations while highlighting regulatory delays for key data center projects.

Following the release of the short report, Bloom Energy rebutted the claims, calling them “false and misleading.” Going into further detail, the company reiterated that it does not have supply chain dependence on China, nor will it in the future as the company expands.

Management also reaffirmed the validity of its financial statements and future projections.

The Bull Case for BE Shares

Bloom Energy’s fundamental story remains robust despite the price action.

The company reported Q1 revenue of $751.1 million, representing 130.4% year-over-year growth that beat consensus by 39%.

Operating income swung to $129.7 million from $13.2 million a year earlier, and the firm raised full-year revenue guidance to $3.4 billion to $3.8 billion.

Net profit reached $70.6 million in Q1, compared to a $23.8 million loss in the year-ago quarter.

Bloom Energy stock remains attractive also because of the recent expansion of Brookfield’s financing framework to $25 billion, which represents the most significant institutional validation of BE’s AI data center power thesis.

This is not an order but a financing ceiling committed through Brookfield’s $100 billion AI Infrastructure Fund, enabling hyperscalers to deploy Bloom's fuel cell technology without carrying upfront capital costs.

Meanwhile, Oracle's (ORCL) decision to power its multi-gigawatt Project Jupiter AI factory entirely with Bloom Energy Servers further cements the company’s position at the center of the AI power trade.

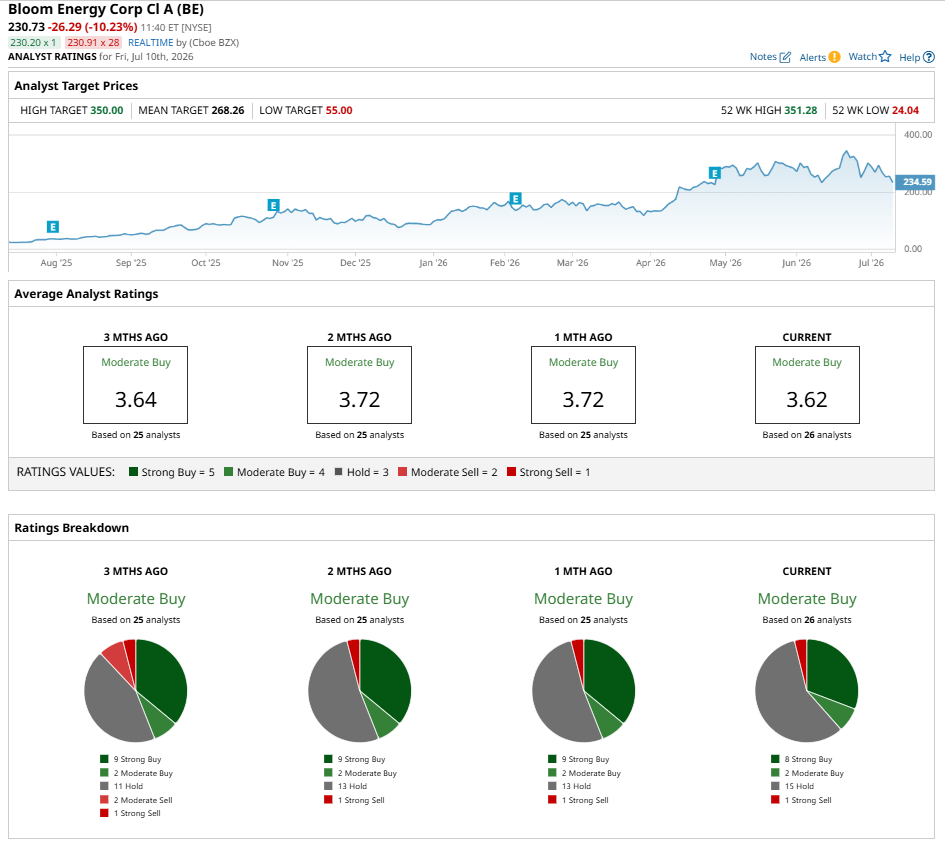

What’s the Consensus Rating on Bloom Energy?

Despite these positives, valuation remains a point of contention. BE stock currently trades at about 219x forward earnings, vastly above the electrical equipment peer group median.

Additionally, Wall Street’s consensus rating on Bloom Energy remains at “Moderate Buy,” and the mean price target of about $268 signals potential upside from current levels.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)