/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

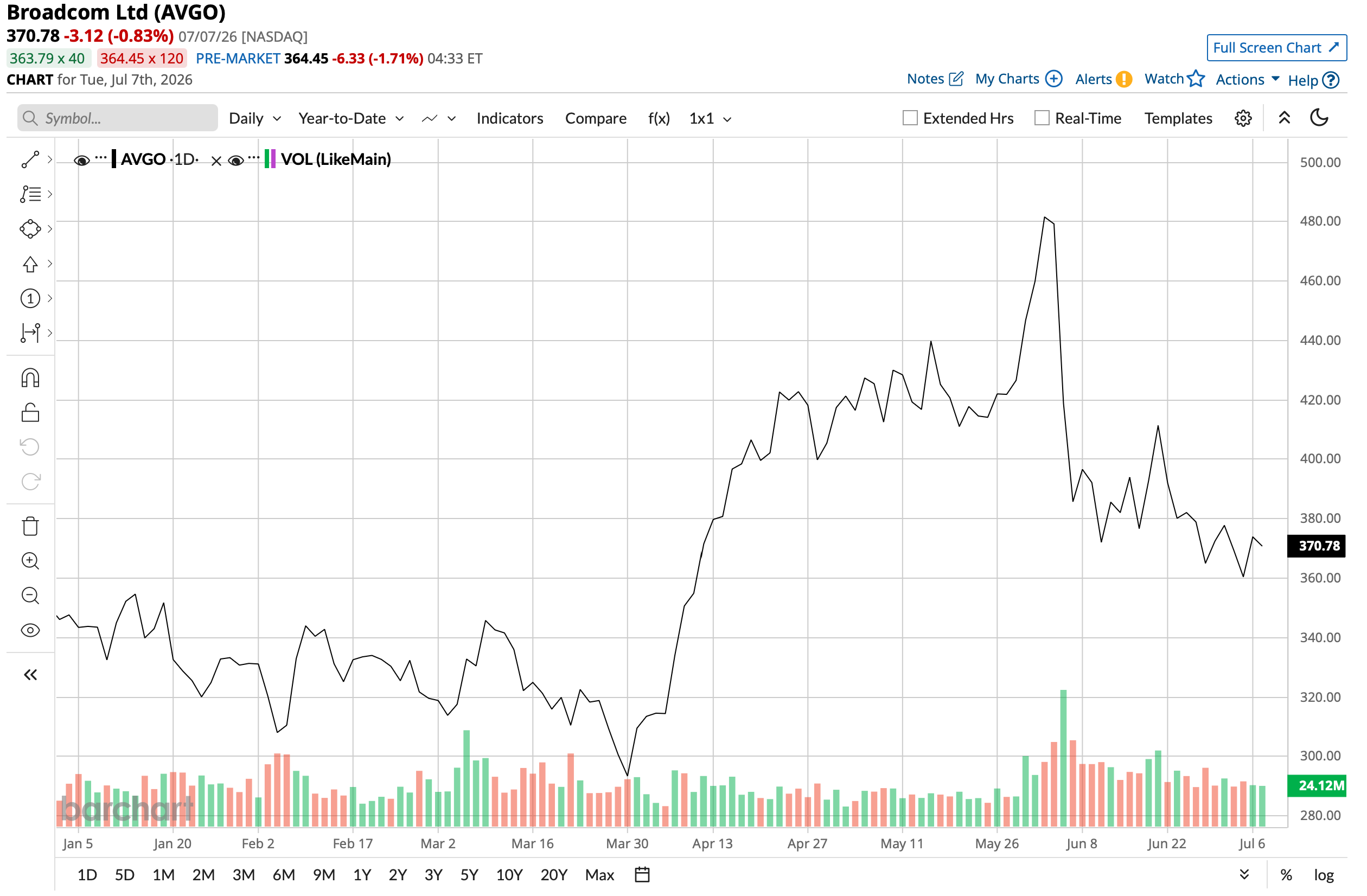

The Erste Group recently downgraded shares of chipmaker Broadcom (AVGO) to “Hold” from “Buy.” Opining that AVGO stock is trading at overvalued levels, analyst Hans Engel said that “the potential for further price appreciation currently appears limited.” However, in the same note, Engel dispelled fears about Broadcom's long-term prospects by reiterating that the company's gross margin and operating margin should remain at high levels, with revenue expected to jump 89% from the previous year to $29.4 billion.

After witnessing a drop-off, AVGO stock recovered to end the day marginally lower on July 7. Overall, valued at a market capitalization of about $1.8 trillion, shares of Broadcom are up 17% on a year-to-date (YTD) basis.

How should investors view Broadcom stock now? Quite favorably, if you ask me. Let's take a closer look.

About Broadcom Stock

With roots tracing back to 1961, Broadcom is a leader in the custom ASICs market. Broadcom currently operates two primary business segments: Semiconductor Solutions and Infrastructure Software. While the former is predominantly focused on custom silicon for data centers, the latter is geared toward enterprise software.

Google-parent Alphabet (GOOGL) is Broadcom's marquee customer. To that end, Google's migration to MediaTek to develop its next chip, “Triggerfish,” should have triggered a sharper adverse response in AVGO stock. It didn't. Instead, a recent chip deal win with AI trendsetter OpenAI to co-develop the “Jalapeño” chip soothed investor sentiment.

Looking beyond these customer rearrangements, Broadcom continues to remain the preeminent name in the custom ASICs market, as I've highlighted before. However, Broadcom's edge goes well beyond its Tomahawk and Jericho switching networks and routing chips.

Optics is quietly becoming Broadcom's next moat. In March, the company debuted Taurus — described as the industry's first 400G per lane optical DSP — and it is pushing co-packaged optics that embed the light engine directly onto the switch package. This matters against its biggest competitor, Marvell Technology (MRVL) specifically because optical DSPs and connectivity are Marvell's home turf. Broadcom is now attacking that revenue pool head-on while also collecting the switch, the SerDes, and the optics on the same design win. The company already has 102.4 terabit switching shipping and a 200 terabit product in development, so it is building the entire scale-up and scale-out road map rather than a single chip.

Broadcom has also tied VMware Cloud Foundation 9.1 directly to enterprise AI inferencing, and it deliberately supports AMD (AMD), Intel (INTC), and Nvidia (NVDA) hardware, meaning software revenue climbs as CPU cores get deployed alongside GPUs rather than competing with them.

All of this has led to the company's robust order book. Broadcom reported AI bookings above $30 billion in a single quarter against only $10.8 billion shipped, extending its order visibility into fiscal 2028. Management reiterated $56 billion in fiscal 2026 AI revenue and is targeting more than $100 billion in fiscal 2027.

Buoyant Fundamentals

Beyond its strong presence in the custom ASICs market, Broadcom's financials reflect its market-leading position. Notably, Broadcom is also one of the few chip companies that has not only been paying dividends but raising them, with 15-straight years of increases. Its current dividend yield stands at 0.70%.

Despite some unnecessary noise, Broadcom's results for the fiscal second quarter were solid. Broadcom achieved net revenue of $22.2 billion, representing a 48% year-over-year (YOY) increase. The semiconductor solutions segment, its main chip operation, posted particularly robust results with revenue advancing 79% YOY to $15 billion. Management expects this segment to generate $16 billion in Q3, pointing to continued acceleration. Meanwhile, the infrastructure software segment saw more moderate growth of 9% YOY to $7.2 billion, slightly missing the analyst forecast of $7.3 billion.

Non-GAAP EPS rose 54% YOY to $2.44, comfortably exceeding the consensus estimate of $2.40 and marking the ninth consecutive quarter of outperforming profit projections. Cash flow from operations was also solid, increasing 60% YOY to $10.5 billion. Broadcom ended the quarter holding $19.6 billion in cash, well ahead of its short-term debt balance of $2.3 billion.

That said, AVGO stock continues to trade at elevated multiples relative to the broader sector. The forward price-to-earnings (P/E) ratio of 36.2 times, price-to-sales (P/S) multiple of 27.6 times, and price-to-cash flow (P/CF) multiple of 48.1 times all sit notably above corresponding sector averages.

What Do Analysts Think of Broadcom Stock?

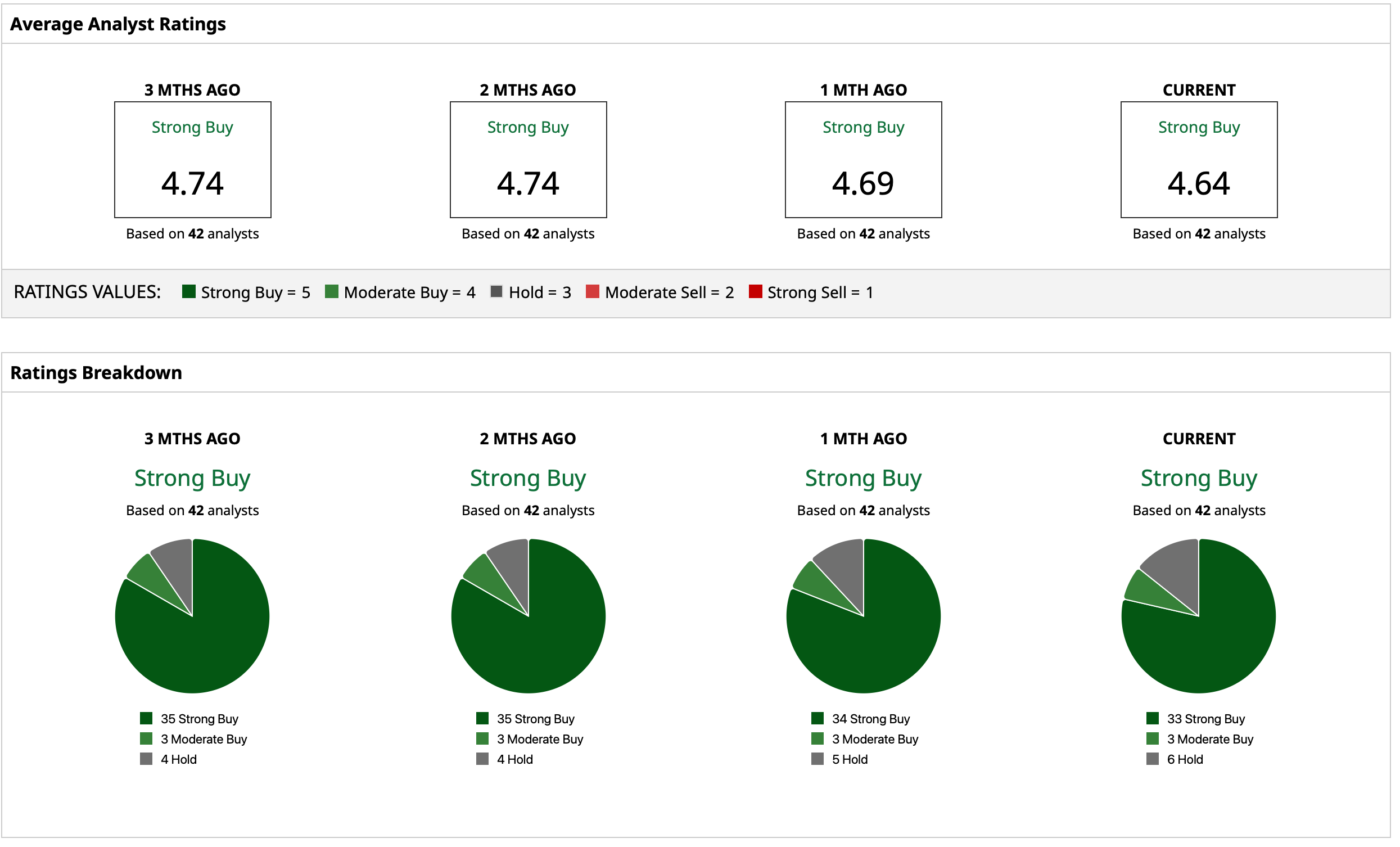

Overall, analysts have a consensus “Strong Buy" rating for AVGO stock. The average target price of $516.59 indicates potential upside of about 28% from current levels. Out of the 42 analysts covering the stock, 33 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and six analysts have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)