/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Chip giant Nvidia Corporation (NVDA) has long been one of the market's biggest darlings, grabbing headlines for its breathtaking rallies and relentless pace of innovation. But now, the stock is trading at valuation levels not seen since at least 2019, well before Nvidia became the face of the artificial intelligence (AI) revolution. But that doesn't mean the company is in trouble. Far from it, in fact. Nvidia's fundamentals remain exceptionally strong. Instead, the recent pullback reflects a shift in investor sentiment.

As the AI build-out matures, enthusiasm for the broader AI trade has cooled, with investors becoming more cautious about the pace of AI spending. At the same time, intensifying competition in the semiconductor industry and a growing search for the next high-growth AI winners have taken some of the shine off Nvidia's once-explosive stock performance. Even so, the recent pullback is far from a reason to abandon the stock. If anything, some on Wall Street believe it has created an attractive entry point.

Nvidia was back in the spotlight on Wednesday after Bank of America reiterated its "Buy" rating and $350 price target, arguing that the company's current valuation already reflects an overly pessimistic outlook. According to analyst Vivek Arya, investors are placing too much weight on concerns over margin pressure, rising competition from custom AI chips, concentrated ownership, and the company's capital allocation strategy. Arya believes those fears overlook Nvidia's biggest strengths. He expects the company's powerful pricing ability, expanding AI infrastructure footprint, and resilient supply chain to keep gross margins in the mid-70% range despite rising memory costs.

Additionally, the analyst noted that Nvidia continues to outpace hyperscaler spending, reinforcing its leadership in AI chips, and expects the company to maintain a commanding 65% to 70% share of long-term AI infrastructure spending. In Bank of America's view, the recent weakness is not a sign of deteriorating fundamentals but rather an opportunity for long-term investors to buy one of the AI industry's strongest franchises at a far more compelling valuation. With that in mind, here's a closer look at NVDA.

About Nvidia Stock

Few companies have played a bigger role in shaping the artificial intelligence revolution than Nvidia. While countless technology firms have ridden the AI wave, Nvidia has been one of the key forces driving it. Founded in 1993 and headquartered in Santa Clara, California, the company first made its name by designing graphics processing units (GPUs) for the gaming industry. What began as a business focused on enhancing gaming experiences has since evolved into a technology powerhouse whose innovations now extend far beyond its original market.

Today, Nvidia sits at the heart of some of the world's most transformative technologies. Its chips power everything from large language models and cloud computing infrastructure to hyperscale data centers, autonomous machines, and advanced scientific research. As AI adoption continues to accelerate across industries, Nvidia has cemented its position as the leading supplier of the computing infrastructure needed to train and deploy generative AI models.

The company's product lineup is led by some of the industry's most sought-after AI platforms, including the H100, Blackwell GPUs, and its next-generation Rubin architecture. Investors have handsomely rewarded that leadership. Nvidia's remarkable rise has propelled its market capitalization to $4.94 trillion, making it the world's most valuable company. Even so, the road to the top has been anything but smooth, with the stock experiencing its share of volatility along the way.

Despite Nvidia's unwavering growth ambitions, its stock has lost some of the blistering momentum that once made it the undisputed star of the AI trade. After delivering a jaw-dropping 14,199% return over the past decade, NVDA's gains have become far more measured. The stock has climbed 24.7% over the past year and 8.9% year-to-date (YTD), solid returns by most standards, but relatively muted compared to several other names in the AI ecosystem that have recently captured investors' attention.

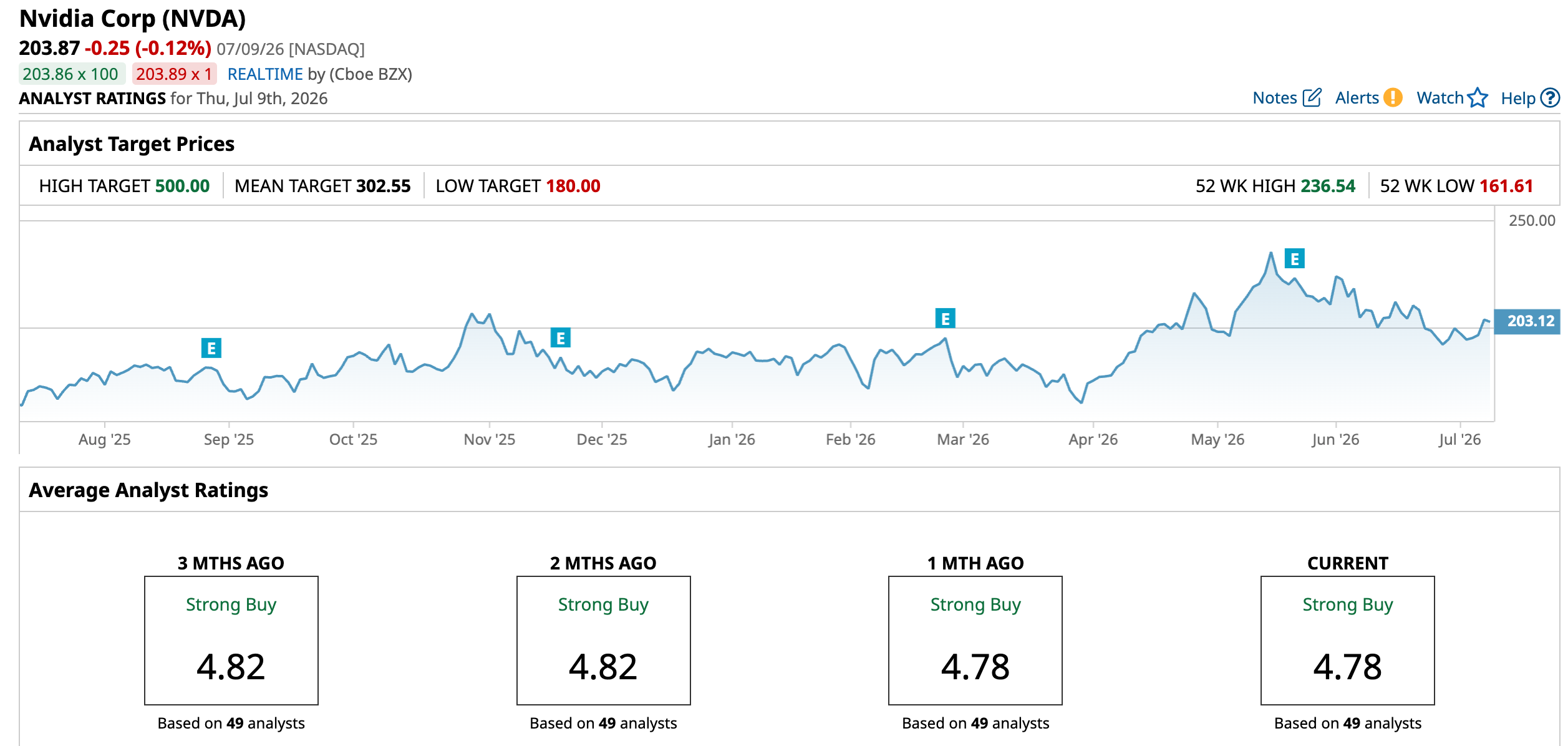

After surging to a record high of $236.54 on May 14, Nvidia shares have since pulled back 13.9% from that peak. The decline reflects a combination of profit-taking, cooling enthusiasm around AI spending, and intensifying competition across the semiconductor industry. In fact, for a company that continues to dominate the AI chip market and deliver industry-leading growth, Nvidia's valuation has significantly cooled and appears far more affordable relative to its peers. The stock currently trades at just 22.65 times forward price-to-earnings, well below Advanced Micro Devices (AMD) at 83.95 times and Intel (INTC) at a staggering 174.25 times.

Inside Nvidia’s Q1 Earnings Report

Nvidia's latest earnings report left little doubt that the AI infrastructure boom remains alive and well. When the company released its fiscal 2027 first-quarter results on May 20, it not only surpassed Wall Street's expectations across the board but also demonstrated that demand for its AI chips continues to accelerate at an extraordinary pace. The numbers were nothing short of remarkable. Quarterly revenue climbed to a record $81.6 billion, representing an 85% year-over-year (YOY) increase from $44.1 billion and a 20% sequential jump from the previous quarter.

The result comfortably topped analysts' consensus estimate of $78.84 billion, highlighting Nvidia's ability to consistently outperform even lofty expectations. Profitability remained equally impressive. Adjusted earnings per share surged a massive 140% YOY to $1.87, easily beating Wall Street's forecast of $1.77. The combination of explosive revenue growth and expanding profits further reinforced Nvidia's position as one of the technology sector's most dominant growth companies.

Another notable development during the quarter was Nvidia's decision to reorganize its reporting structure. To better reflect its expanding business and long-term growth strategy, the company now reports its operations under two primary platforms, Data Center and Edge Computing, a move that illustrates how its business has evolved well beyond traditional graphics processors. The numbers show just how central the Data Center business has become.

The segment generated a record $75.2 billion in revenue during the quarter, accounting for more than 92% of Nvidia's total sales. Revenue from the division soared 92% YOY, fueled by continued investment from hyperscalers, enterprises, and governments racing to build generative AI infrastructure and expand cloud computing capacity. While Data Center remains the clear growth engine, Nvidia's newly defined Edge Computing business is also gaining momentum.

The segment generated $6.4 billion in quarterly revenue, up 29% from a year ago. The business includes data processing technologies supporting agentic and physical AI applications across PCs, gaming consoles, workstations, AI-RAN base stations, robotics platforms, and automotive solutions. Nvidia's ability to translate strong demand into sustained profitability also remained on full display. The company reported a GAAP gross margin of 74.9%, virtually unchanged from the prior quarter and 14.4 percentage points higher than the same period last year, underscoring the strength of its pricing power and operating efficiency.

Also, management continued returning significant amounts of capital to shareholders. During the first quarter alone, Nvidia returned a record $20 billion through share repurchases and cash dividends. However, perhaps the biggest takeaway from the report was management's outlook. Nvidia projected second-quarter fiscal 2027 revenue of approximately $91 billion at the midpoint, comfortably ahead of Wall Street's consensus estimate of roughly $86.11 billion.

Notably, that forecast excludes any contribution from Data Center compute revenue generated in China, highlighting the strength of demand elsewhere. And, the company expects GAAP gross margins of 74.9% and non-GAAP gross margins of 75%, plus or minus 50 basis points. Altogether, the guidance suggests that enterprise AI spending remains robust and that Nvidia's growth momentum is showing little sign of slowing.

What Analysts Are Saying About Nvidia Stock

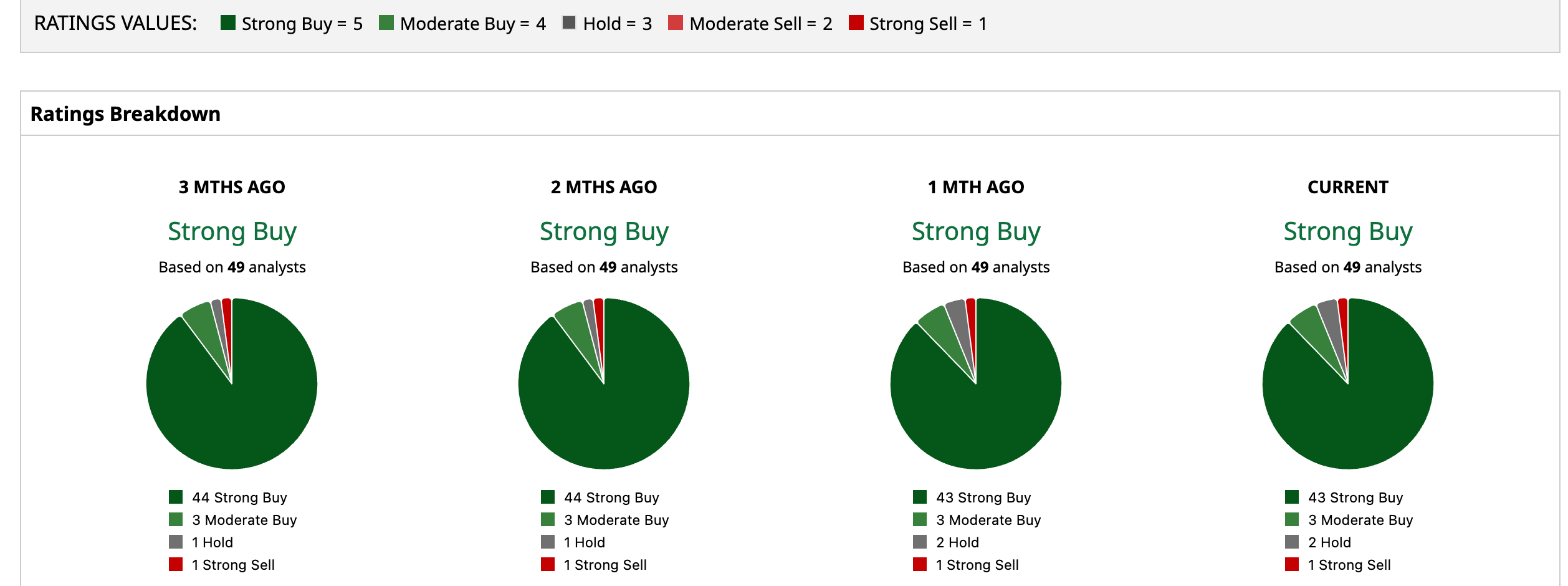

Although investor enthusiasm has cooled as capital rotates toward other corners of the rapidly evolving AI ecosystem, Wall Street's conviction in Nvidia has remained remarkably resilient. And the bullish sentiment is echoed across Wall Street. Nvidia currently enjoys a "Strong Buy" consensus rating based on recommendations from 49 analysts. Of those, an overwhelming 43 rate the stock "Strong Buy," three recommend "Moderate Buy," two advise "Hold," and only one has issued a "Strong Sell" rating.

Wall Street also sees significant upside ahead. The average price target of $302.55 implies a potential gain of 48.4%, while the Street-high target of $500 suggests Nvidia shares could soar by as much as 145.3%. Overall, even as Nvidia's stock has cooled from its highs, its business momentum remains firmly intact. Backed by strong fundamentals, continued AI leadership, and broad Wall Street support, the company’s valuation reset could prove to be an attractive opportunity for long-term investors.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)