/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

Valued at a market capitalization of $83.2 billion, Synopsys (SNPS) stock has underperformed the broader market in recent years. While most chip stocks have crushed index returns, SNPS stock has remained largely range-bound over the last three years.

Synopsys is the company behind the software that helps build advanced processors. Now, it is quietly stepping away from a part of its business that once mattered a great deal. At the same time, the firm is telling investors that its AI push is working better than expected. Put those two things together, and you get a company reshaping itself in real time.

Why Synopsys Software Touches Nearly Every Chip Made Today

Synopsys is one of the most dominant players in electronic design automation (EDA), the specialized software used to design and verify computer chips. Chipmakers cannot build advanced processors without tools that Synopsys and its peers offer.

Beyond design software, Synopsys sells intellectual property, prebuilt chip components that customers license rather than build from scratch, and physics simulation tools it acquired with its acquisition of Ansys.

Synopsys plans to stop offering a set of manufacturing process control software used by major chipmakers, according to sources cited by Reuters. Per the report, the company told more than 10 chipmakers — including Samsung Electronics, SK Hynix, Kioxia (KXIAY), and Qorvo (QRVO) — that the products are reaching end of life. That means no new versions of the software and only basic maintenance going forward.

A few dozen employees have also already been let go, according to sources, and Synopsys aims to wrap up maintenance talks with each customer this month. A spokesperson confirmed that the company is discontinuing certain older products to focus on its highest-value offerings, while honoring existing customer contracts.

Samsung confirmed the decision to Reuters and said it does not expect any impact on production. Sources also noted that the move frees up engineers for higher-margin AI design work and reflects that some customers are increasingly building similar tools in-house.

The AI Business Behind the Shift

The retreat from legacy manufacturing tools lines up with what Synopsys told investors recently. In its second-quarter earnings report on May 27, the company reported revenue of $2.28 billion, and beat its own guidance for revenue and EPS.

CEO Sassine Ghazi told analysts that AI is scaling up both the complexity of chips and the systems built around them, driving demand across the portfolio. The company raised its full-year revenue, margin, earnings, and cash flow guidance based on growing demand. Design IP, the licensing business, grew 12% from the prior quarter after bottoming out earlier in the year.

Ghazi said the real opportunity going forward is convincing hyperscale customers who are building their own custom chips to pay a share of ongoing royalties rather than a flat licensing fee, since those companies cannot build competitive chips without Synopsys technology.

Speaking at the 2026 Mizuho Technology Conference on June 9, Ghazi laid out future growth drivers, describing a split between human engineers and “agent engineers” — AI systems that will run Synopsys software alongside people to design chips faster. That shift opens the door to a new pricing model, moving beyond a subscription for human users toward one that also charges for AI agent usage. “Our agentic EDA capabilities are gaining traction with 20 customers now evaluating solutions across more than 25 specialized AI agents spanning front end verification implementation and analog flows,” Ghazi said on the Q2 earnings call. At the Mizuho conference, the CEO also pointed to Synonpsys' partnership with Nvidia (NVDA) spanning accelerated computing, AI agent orchestration, and physical AI simulation.

What's Next for SNPS Stock?

Synopsys still faces China-related restrictions and a workforce reduction tied to its Ansys integration. The company is trimming older, lower-margin software and doubling down on AI-driven design, custom chip licensing, and physics simulation. Synopsys plans to lay out more detail on its long-term strategy at an Investor Day set for September 30. Chip design increasingly looks like a team of humans and AI agents working together, with Synopsys software running underneath either way.

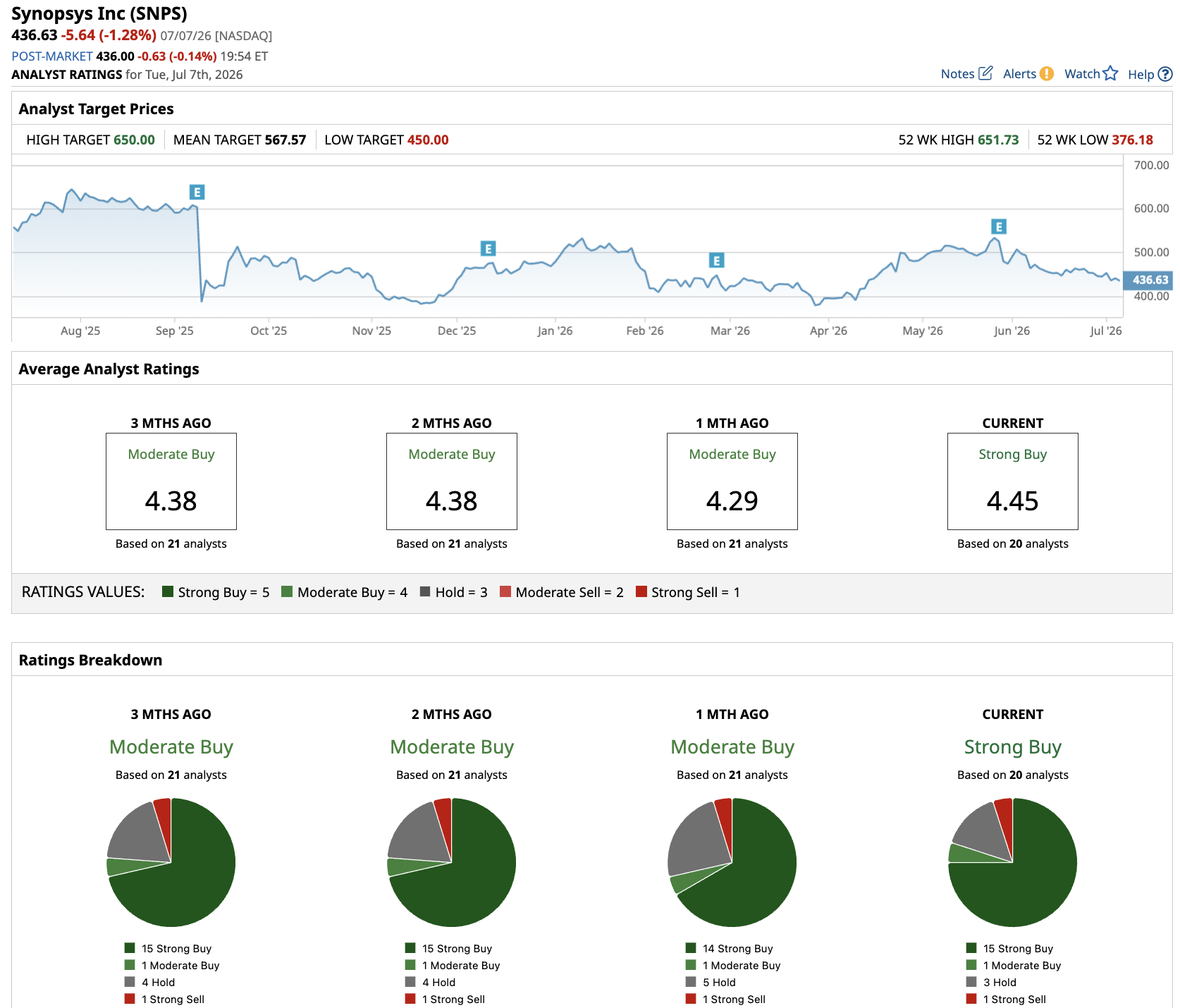

Analysts tracking Synopsys stock have a consensus “Strong Buy” rating. Out of the 20 analysts covering SNPS stock, 15 recommend a “Strong Buy” rating, one recommends a “Moderate Buy,” three recommend a “Hold," and one analyst has a “Strong Sell." The average price target of $567.57 suggests potential upside of 29% from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)