PepsiCo (PEP) shares opened in the red this morning even though the beverage giant posted better-than-expected earnings for its second financial quarter.

The multinational reported $24.18 billion in revenue — up 6.4% on a year-over-year basis — and $2.20 in earnings per share (EPS) for its fiscal Q2.

The quarterly release adds to pressure on PepsiCo stock that was already down about 17% heading into July 9.

Why Is PepsiCo Stock Under Pressure Today?

Investors are bailing on PEP shares mostly due to weakness in the firm’s North America business.

While international markets boomed, the domestic segment experienced a 2% decline in revenue to $6.37 billion in the second quarter.

Additionally, to tackle generic rivals and attract inflation-weary customers, PepsiCo had to lower prices and resort to significant affordability initiatives.

This resulted in a 40-basis-point decline in Q2 core operating margin. Compounding the pain, the recent high-profile loss of PEP’s global partnership with Marriott is hurting sentiment as well.

Note that the post-earnings decline saw PepsiCo sink below its 20-day moving average (MA) today, reinforcing shifting momentum in favor of the bears.

Should You Buy the Post-Earnings Dip in PEP Shares?

For patient, long-term investors, PepsiCo shares remain attractive to buy on the post-earnings dip.

Despite regional pressure, the Nasdaq-listed firm successfully turned around its total sales volumes, posting a 1% global increase for the second financial quarter.

Meanwhile, management confidently reaffirmed its full-year guidance for at least 2% organic sales growth and 4% upside in core constant-currency EPS as well.

Crucially, PEP currently pays a rather healthy 4.35% dividend yield, which combined with a newly authorized $10 billion stock buyback program offers significant downside protection.

All in all, loading up on PepsiCo today offers exposure to a resilient, defensive staple at a notable discount.

Wall Street Remains Bullish on PepsiCo

Despite its year-to-date underperformance, Wall Street firms haven’t thrown in the towel on PEP stock.

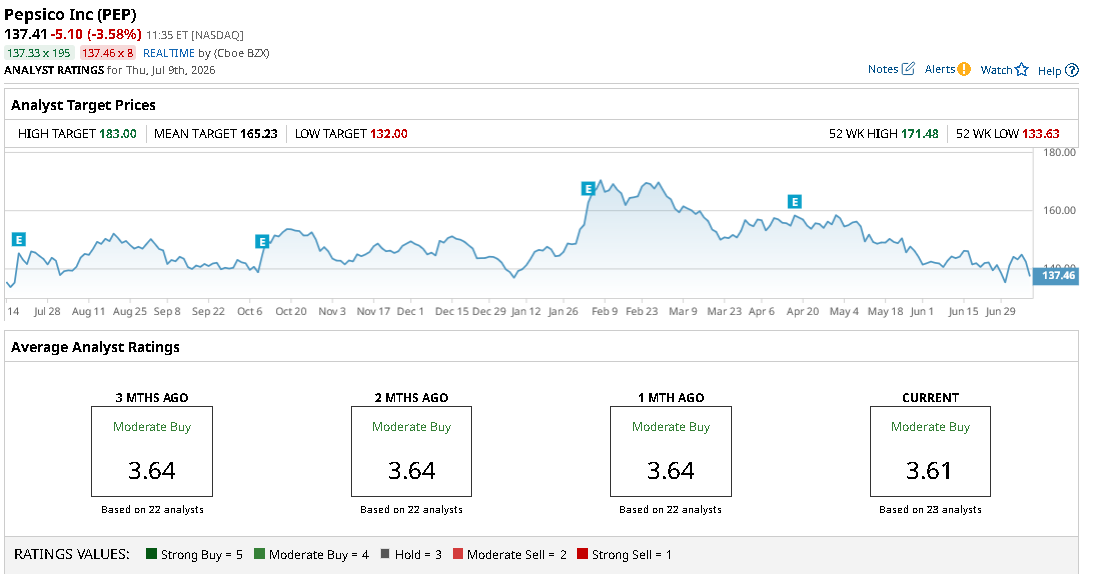

According to Barchart, the consensus rating on PepsiCo remains at “Moderate Buy,” with the mean price target of about $165 indicating potential upside of more than 20% from current levels.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)