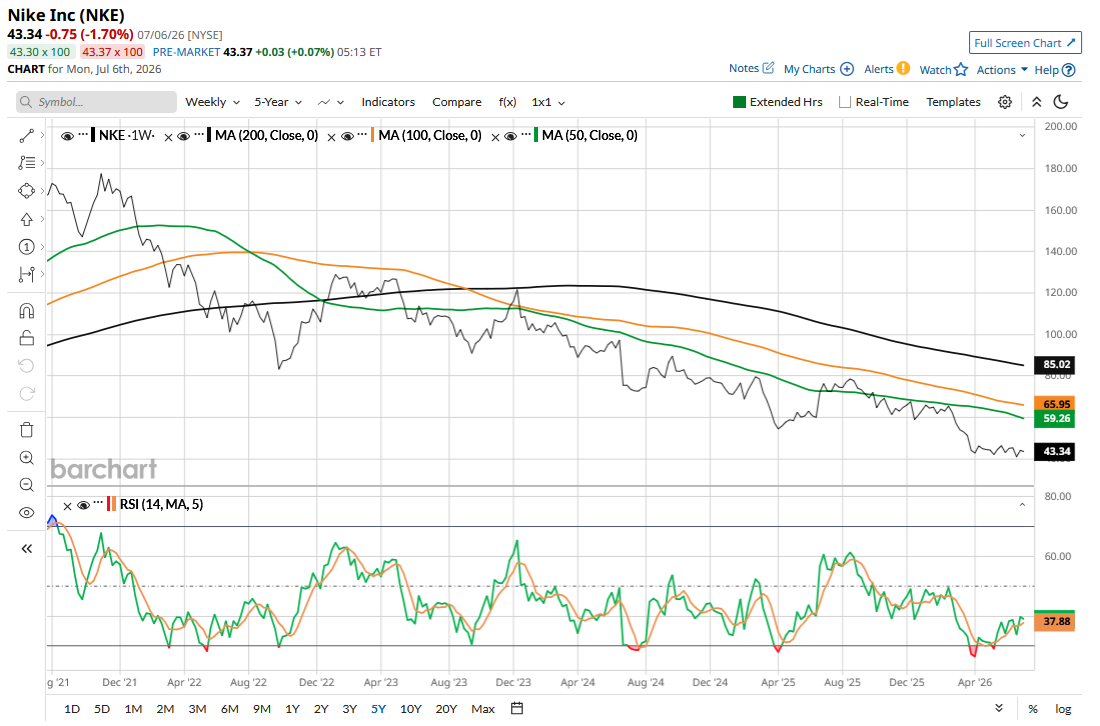

Nike (NKE), the iconic sneaker brand, is having a tough time. The stock closed in the red for the last four consecutive years and is down nearly 32% for this year. NKE stock peaked in November 2021 and has since lost three-fourths of its market cap.

Amid a sagging stock price, Nike brought back Elliott Hill, a company veteran, to lead the company in October 2024. Hill succeeded John Donahoe, whose strategy of focusing on direct sales while cutting down on wholesale sales backfired after the initial success during the Covid-19 pandemic. In hindsight, the company miscalculated the brand pull and lost out to other brands that were well stocked at third-party stores. Along with mending relations with wholesalers, Hill has shifted Nike’s attention back towards sports, which used to be its USP. However, these measures haven't helped reverse the slide in NKE stock.

A sagging stock price coupled with gradual dividend hikes has pushed Nike’s dividend yield to nearly 3.8%, which is near the record highs that we saw last month when the stock hit its 52-week lows. In my previous article, I noted that while Nike’s risk-reward has improved, it’s not a compelling buy yet. Let’s explore if the stock can fit into portfolios of investors who crave high dividend stocks, beginning with the company’s recent financial performance.

Nike's Tepid First Half Guidance

Nike’s revenues fell 1% year-over-year (YoY) in its fiscal Q4 2026, which ended in May, even though the metric came in slightly better than feared. Wholesale revenues rose 4% in the quarter but couldn’t fully offset the 7% decline in Direct sales. Looking at the geographical breakdown, North America revenues rose 3% while sales in Greater China fell 12% in the quarter.

Notably, China remains a structural headwind for Nike, as not only is that market not growing as fast as it once used to, but Chinese consumers have increasingly been preferring domestic brands over U.S. rivals. During the Q4 earnings call, Hill discussed the need to be “more premium and culturally relevant” in China, which is the company’s second biggest market.

Nike’s beat on the bottom line also with adjusted earnings per share (EPS) of 20 cents, easily surpassing the 12 cents that analysts were modeling. Importantly, the numbers don’t account for the $986 million tariff refund Nike expects after the Supreme Court voided most of the tariffs President Donald Trump imposed.

Meanwhile, even as Nike’s earnings were better-than-expected, the management cut its guidance and now expects sales to fall “low to mid-single digits” in the first half of the current fiscal year. The company, however, expects gross margin expansion from the first quarter versus the previous guidance of it rising from the second quarter.

NKE Stock Forecast

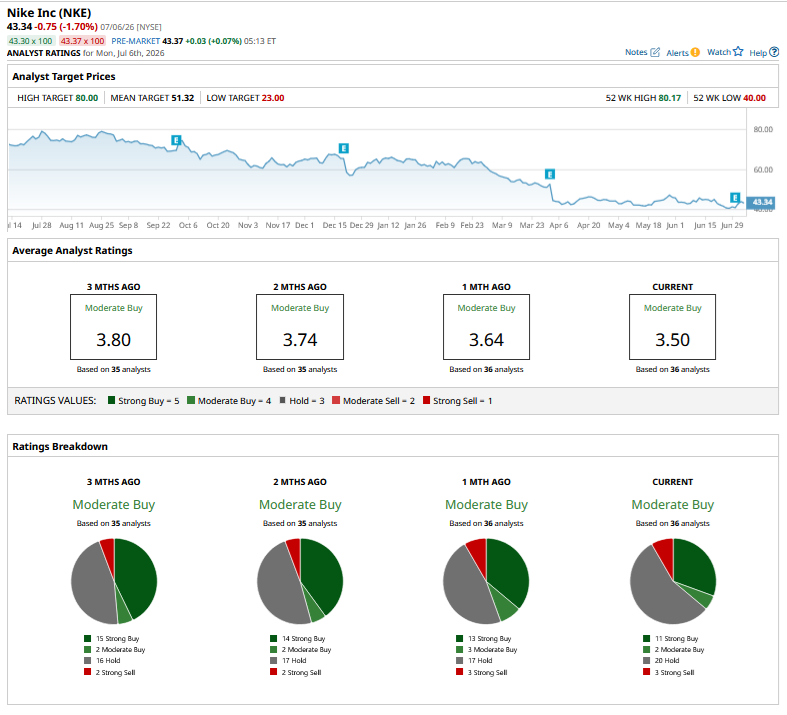

Analysts have been gradually lowering Nike’s target price, along with intermittent downgrades, and their reaction to the company’s fiscal Q4 2026 earnings was no different. There was a flurry of target price cuts after the company’s cautious outlook. Looking at some of the major changes, Barclays lowered NKE stock's target price from $67 to $52, while Bank of America lowered its from $55 to $47. There were even bigger cuts heading into the confessional, and Oppenheimer cut its target by half to $60, while BTIG lowered its estimate from $75 to $55.

Overall, NKE stock has a mean target price of $51.32, which is about 19% higher than its current price. Its Street-low target price of $23 (via BNP Paribas) represents a downside of another 47% even from these depressed levels.

Should You Buy Nike for Its Dividend?

More often than not, companies with very high dividend yields tend to be in trouble, unless they are in sectors that are known to pay much of their earnings as dividends, REITs, for instance. Nike, meanwhile, characterizes itself as a “growth company,” and investors should expect the majority of gains to come from the increase in share price, which sadly hasn’t been the case since late 2021, as the stock has only gone south.

Nike trades at a forward price-to-earnings (P/E) multiple of 24.48x and 18.2x its expected fiscal 2028 earnings. The multiples have come off amid the decline in NKE’s stock price, but I still don’t find them attractive enough to buy the stock.

The company's stock is a play on the turnaround, which is taking a lot longer than expected. Moreover, there is no quick fix to the company’s woes, as increasing sales and margins concurrently is easier said than done. Turning around the China business would be another challenging task for Nike, given the deep-rooted challenges in that market. Overall, while the downside in NKE should be limited from these levels, the risk-reward is not enticing enough to buy the stock even with a fat dividend yield.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)

/A%20close-up%20shot%20of%20a%20Broadcom%20chip%20by%20g0d4ather%20via%20Adobe%20Stock.jpeg)