/A%20close-up%20shot%20of%20a%20Broadcom%20chip%20by%20g0d4ather%20via%20Adobe%20Stock.jpeg)

For years, the biggest debate surrounding semiconductor stocks wasn't whether artificial intelligence would fuel another wave of growth. It was which companies could protect that growth from their largest customers.

Investors watched major technology companies increasingly design their own chips, squeezing suppliers out of lucrative markets. That trend appeared destined to catch Broadcom (AVGO), whose largest customer, Apple (AAPL), had spent years developing more components internally.

Apple's newly announced $30 billion agreement with Broadcom changes that narrative in one stroke. Rather than replacing Broadcom, Apple just committed billions to keep it at the center of future iPhones and other devices.

Apple Eliminated Broadcom's Biggest Long-Term Risk

The agreement secures Broadcom as Apple's supplier of critical wireless connectivity and radio frequency (RF) technologies through 2031.

For years, Wall Street viewed Apple's internal chip ambitions as Broadcom's largest strategic threat because Apple historically represented about 20% of Broadcom's annual revenue. That customer concentration always carried the risk that Apple could eventually walk away. Instead, Apple effectively acknowledged that one area remains beyond its in-house expertise.

Broadcom's specialized Film Bulk Acoustic Resonator (FBAR) filters and advanced RF components manage the increasingly crowded wireless spectrum used by 5G, Wi-Fi, and Bluetooth. Those filters prevent signals from interfering with one another, improving call quality, wireless speeds, and battery efficiency.

The agreement also includes custom application-specific integrated circuits (ASICs) designed for wireless networking and specialized processing tasks across future Apple devices. Unlike Apple's A-series and M-series processors, these chips handle dedicated communication functions that require decades of RF engineering expertise.

Stable Cash Flows Can Fuel Broadcom's AI Expansion

Ironically, this deal isn't really about consumer electronics. It's about artificial intelligence. Broadcom is investing $1.5 billion to modernize its manufacturing facility in Fort Collins, Colorado. Apple's long-term commitment gives Broadcom confidence that those factories will operate at high utilization instead of sitting partially idle.

That predictable revenue stream frees management to pursue the company's fastest-growing opportunity—custom AI accelerators.

Broadcom already designs custom AI ASICs for hyperscale customers, including Alphabet's (GOOG) (GOOGL) Google, Meta Platforms (META), OpenAI, and Anthropic. Those chips compete in a different segment than Nvidia's (NVDA) GPUs by delivering purpose-built silicon for massive cloud workloads.

Steady consumer hardware revenue effectively becomes the financial engine that funds Broadcom's AI expansion without stretching its balance sheet or threatening its dividend growth.

Granted, Apple still represents a large percentage of revenue, so customer concentration doesn't disappear overnight. But the nature of that concentration changes when the customer signs a multi-year commitment rather than working toward replacing you.

Broadcom has always generated healthy free cash flow, but this agreement gives investors something equally valuable: visibility. Few semiconductor companies can point to billions of dollars in contracted business spanning multiple product generations while simultaneously participating in the AI infrastructure boom.

That combination makes Broadcom stand apart from many chipmakers that depend on shorter product cycles or more volatile consumer demand.

Valuation Still Leaves Room for More Upside

Despite market concerns rising as AI memory stocks face a decline amid geopolitical tensions and profit-taking in the AI sector, Broadcom doesn't appear fully priced for the opportunities now in front of it. The company trades at 35.21 times forward earnings, in line with many high-growth AI semiconductor peers, despite generating faster revenue growth than most of the industry.

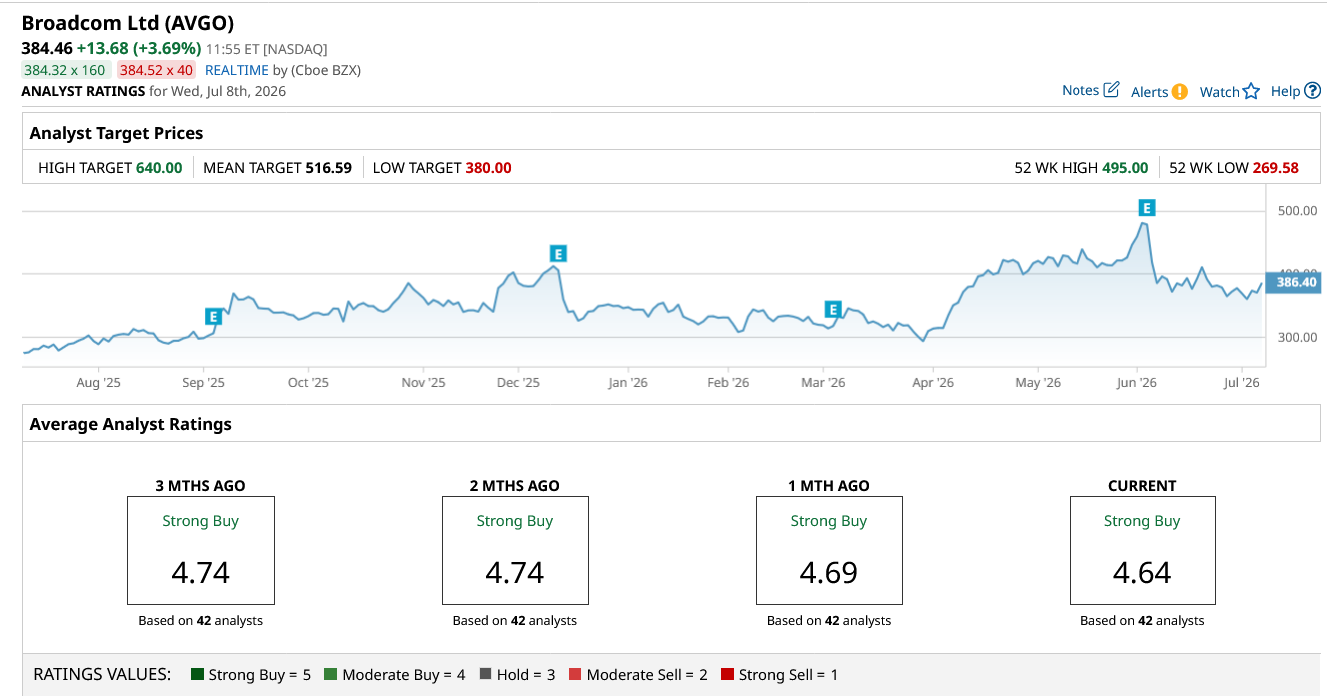

Wall Street also remains firmly in Broadcom's corner. Consensus estimates from 42 analysts call for shares to reach $516.59 over the next 12 months, implying 39% upside from recent trading levels.

Granted, Broadcom is no longer the bargain it was before the AI boom began. But investors aren't simply buying a semiconductor company anymore. They're buying a business with a long-term consumer hardware cash machine, a rapidly expanding custom AI chip franchise, growing software revenue from VMware, and now one less existential risk hanging over the investment thesis.

Key Takeaway for AVGO Stock

In short, Apple's $30 billion commitment is far more than another supply agreement. It removes Broadcom's largest structural risk, supports a $1.5 billion U.S. manufacturing expansion, and provides the dependable cash flow needed to accelerate its custom AI chip business.

Apple isn't simply buying components—it is committing to Broadcom's unique RF technology because it remains difficult to duplicate. For long-term investors seeking dividend growth, dependable cash flow, and exposure to one of the fastest-growing corners of AI infrastructure, Broadcom looks stronger today than it did before the agreement. That's a rare combination in the semiconductor industry, and one that makes AVGO stock look like a compelling long-term buy.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)