Nike (NKE) surprised Wall Street with a stronger-than-expected fiscal fourth quarter in 2026. Both earnings and revenue beat consensus estimates by a wide margin. Yet, the Q4 print failed to impress investors, with the stock down 31% year-to-date (YTD), underperforming the overall market gain of 9.1%. This muted reaction shows that investors need more than just a single good quarter to believe in Nike’s sustained turnaround story.

So, despite the earnings beat, are investors right to be cautious?

The Quarter Was Good, but the Underlying Story Is More Complicated

In the fourth quarter of fiscal 2026, Nike reported a 1% dip in revenue on a reported basis to $11 billion. This modest decline was the contribution of the North America business that partially offset continued weakness in Greater China, Europe, Middle East & Africa (EMEA), and Converse. Revenue beat Wall Street expectations by $122.6 million. Gross margin expanded sharply to 49.2%, an increase of 890 basis points year over year. However, this improvement was the doing of a one-time $986 million recovery of previously paid tariffs. Excluding this recovery, gross margin would have been 40.2%.

Likewise, reported earnings per share reached $0.72, beating consensus estimates by $0.59. But remove the tariff recovery benefit, and EPS would have been just $0.20. Nonetheless, Nike maintained disciplined cost control in the quarter, with selling, general, and administrative expenses falling 2% despite higher marketing investments for the FIFA Women's World Cup.

For the full fiscal year, revenue mostly remained flat on a reported basis. Gross margin for the year also improved to 42.9%, thanks to tariff recoveries. Diluted EPS totaled $2.10, down 3% from the prior year. Nike also had to absorb roughly $400 million in severance costs as part of its restructuring efforts. However, these efforts are intended to streamline operations and ultimately boost long-term profitability.

Investors Remain Focused on the Slow Recovery

Despite these operational improvements, investors remained focused on Nike's largest businesses that continue to struggle. Sportswear and Jordan Streetwear are still experiencing difficult sell-through trends, elevated discounting, and weaker future order books. Together, both these businesses account for half of Nike's total revenue. Therefore, their recovery is essential for restoring sustainable long-term growth. Management expects both categories to remain negative during fiscal 2027, with improvement anticipated only in the second half of the year.

Coming to regional performance, while North America remained the bright spot, revenue declined 6% in EMEA, and Greater China saw revenue dip by 17%. Meanwhile, Asia Pacific and Latin America (APLA) saw revenue decline 1%. Management cited weaker discretionary consumer spending, declining store traffic, evolving tariff policies, geopolitical disruption in the Middle East, and higher oil prices as factors weighing on demand. Probably what disappointed investors was when management stated that Nike does not expect the macro environment to improve much over the next six months.

Overall, Nike now expects first-quarter fiscal 2027 revenue to decline by the low-to-mid single digits, with a similar trend expected over the first half of the year. The consensus revenue estimates for fiscal 2027 align with the company’s projections, but analysts estimate earnings to increase by 8.8% in fiscal 2027, before rising by 38.4% in fiscal 2028. To summarize, the near-term growth story failed to excite investors.

Is Nike Still A Good Dividend Stock?

Although the turnaround did not impress growth investors, NKE stock is still appealing to income investors. It pays a forward dividend yield of 3.8%, much higher than the consumer discretionary and the market average. Its forward payout ratio of 71% may be high, raising concerns about the dividend's sustainability. But Nike has been paying and increasing dividends for the past 23 years, despite earnings pressure. In fact, the company is close to earning the title of a “Dividend Aristocrat,” which is awarded to companies that pay and increase dividends for 25 years in a row.

During the earnings call, management also emphasized that the company is improving supply chain efficiency, operating costs, and cash flow generation, all of which could strengthen long-term dividend sustainability. The company ended the quarter with $9 billion in cash, equivalents, and short-term investments.

The Bottom Line on NKE Stock

No doubt, Nike's Q4 and fiscal-2026 results were stronger than what Wall Street expected. However, the Sportswear and Jordan Streetwear, which account for a significant chunk of its revenue, remain under pressure, while Greater China continues to struggle. Even management warned of another six months of difficult operating conditions. While these factors make the short-term story vulnerable, the case is different for long-term investors. Nike is rebuilding its product pipeline, regaining momentum in performance categories such as running and football, modernizing its retail footprint, and maintaining one of the strongest balance sheets in the industry. The turnaround will likely take time, so long-term investors may want to hold on to the stock.

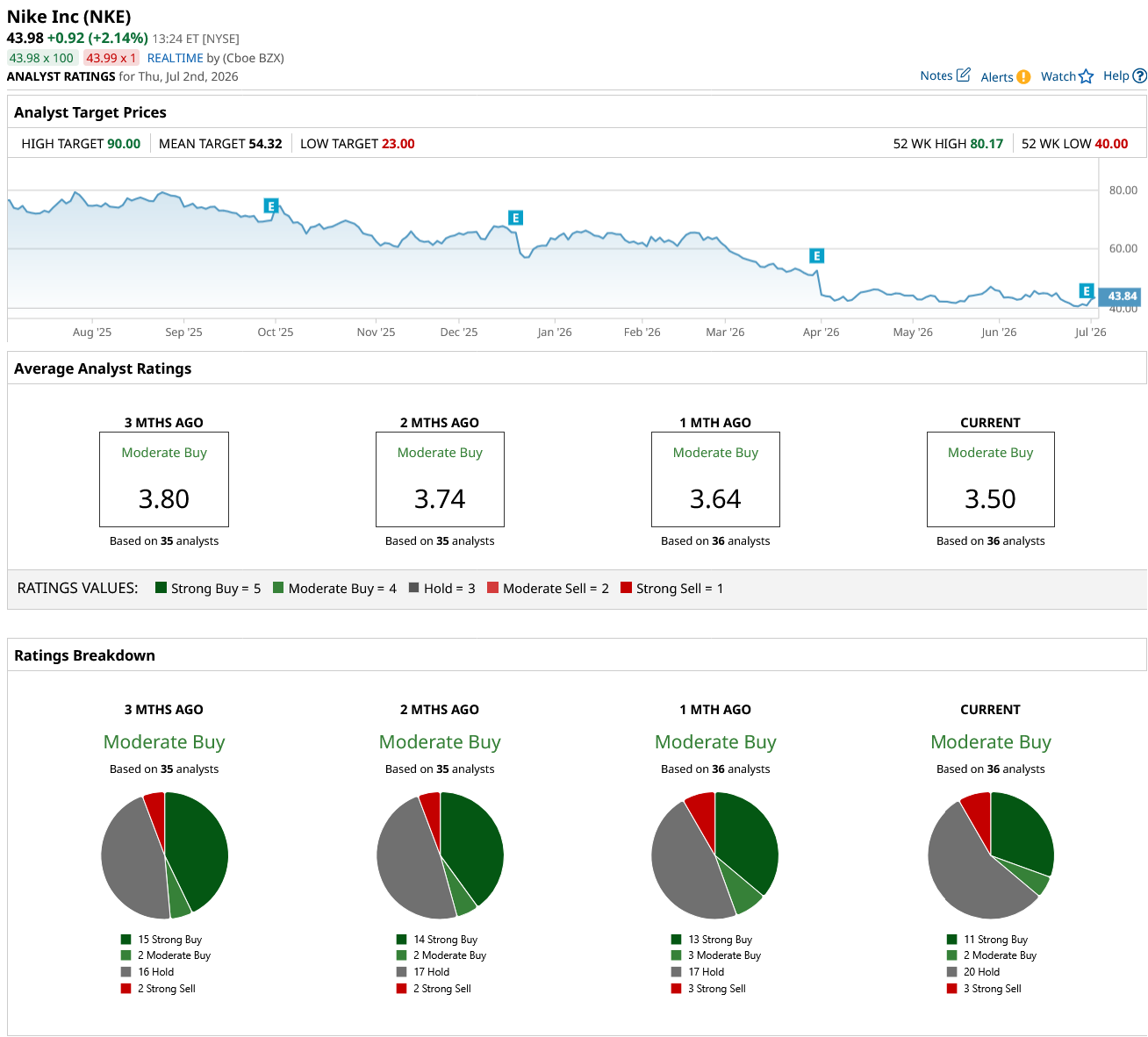

On Wall Street, NKE stock is rated as a “Moderate Buy.” Of the 36 analysts who cover the stock, 11 rate it as a “Strong Buy,” two say it is a “Moderate Buy,” 20 rate it a “Hold,” and three say it is a “Strong Sell.” The average analyst target price of $54.32 for Nike implies a 24% increase over current levels. Furthermore, its Street-high estimate of $90 suggests that the stock could rally by up to 105% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)