/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Citi’s latest call on Micron Technology (MU) comes down to one clear tailwind. The firm added MU to its upside Catalyst Watch because it expects stronger DRAM pricing in the second half of 2026.

That view looks even more interesting when you look at Citi’s bigger pricing outlook. The bank expects DRAM prices to nearly triple next year, which would be a big win for Micron since its revenue and margins move closely with memory prices.

The timing also makes sense. Micron just posted Q2 CY2026 revenue of $41.46 billion, up 346% from a year ago. On top of that, the stock has climbed 132.8% over the past three months.

That kind of beat-and-raise story tends to keep investors paying attention. With Citi now signaling that Micron could have another near-term upside trigger, the key question is whether MU still has room to run after its huge rally.

Micron’s Upside Numbers

Micron manufactures DRAM, NAND, and high-bandwidth memory products from its plant in Boise, Idaho. The company sells to data centers, PC makers, mobile device producers, and automotive customers. At this point, its market cap is about $1.10 trillion.

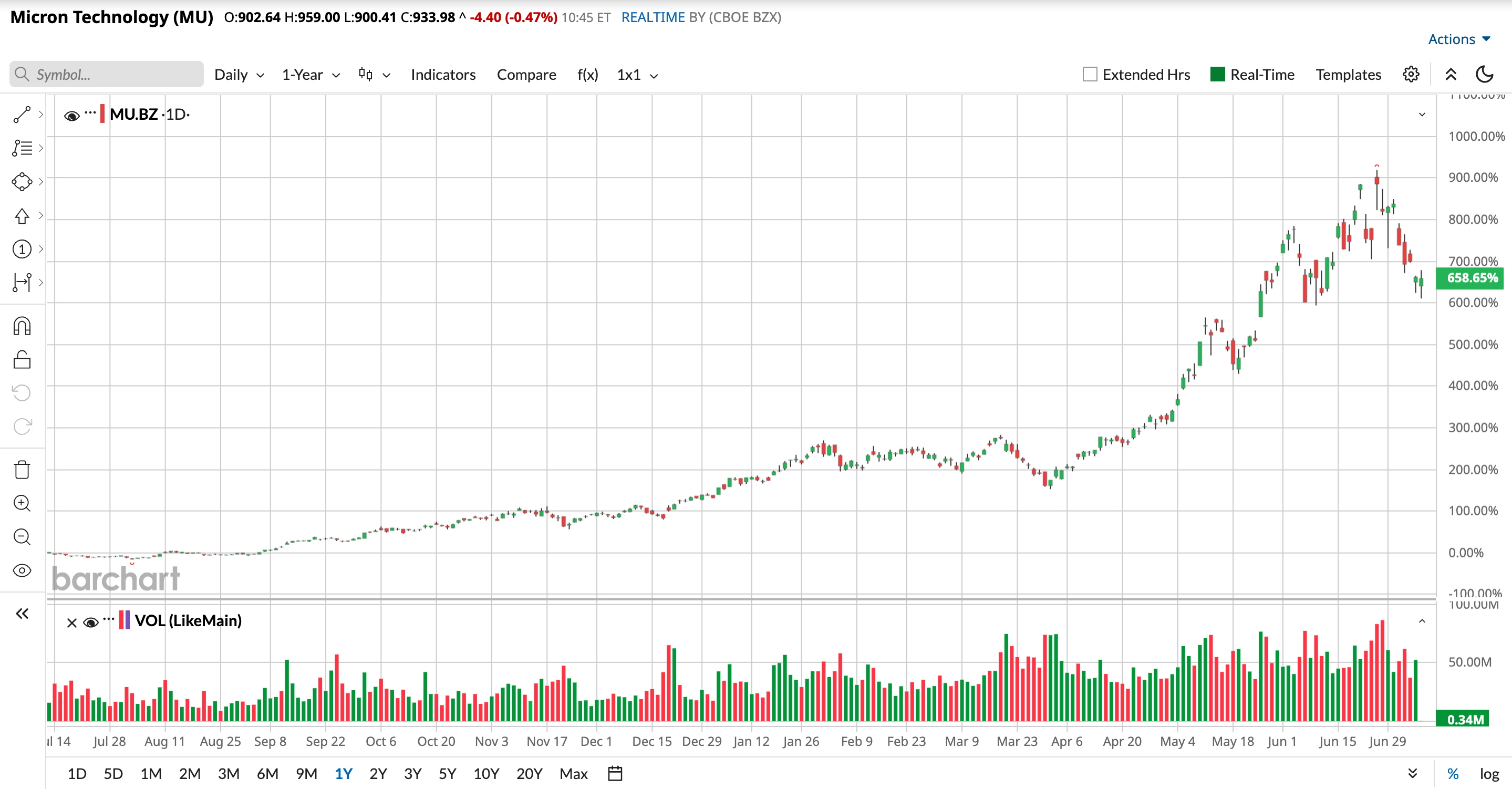

MU stock is up 231.7% for the year and 660.9% over the last 52 weeks.

On valuation, Micron’s trailing price-to-earnings is 20.80 times, below the sector median of 26.17 times. Its price-to-sales ratio comes in at 11.69 times, which is well above the sector median of 3.66 times.

Micron Technology reported Q2 fiscal results as it posted an earnings surprise for the quarter ending May 26, with reported EPS of $24.89 against an estimate of $20.98. The result represented a positive surprise of 18.64%.

MU delivered revenue of $41.46 billion, ahead of the $36.28 billion consensus, marking 346% year-over-year (YOY) growth and a 14.3% beat. Micron Technology also reported adjusted EPS of $25.11, topping the $19.66 analyst estimate by 27.7%.

This quarter also produced adjusted operating income of $33.68 billion, above estimates of $25.4 billion. It translated into an 81.2% adjusted operating margin and a 32.6% beat, which points to exceptional profitability.

The company’s operating margin reached 80.4%, up from 23.3% in the same quarter last year. In May 2026, MU generated an operating cash flow of $45.702 billion, up 124.98%. Micron ended the period with net cash flow of $15.376 billion, which was up 258.58%.

Citi’s Bullish Case for Micron

Alongside the stronger DRAM outlook, Micron is shoring up demand with a deeper partnership with General Motors (GM). GM will use Micron’s memory and storage platforms in vehicle production and, just as importantly, lock in future supply without risking disruptions on the factory floor.

The parts involved are very specific and matter a lot commercially. General Motors is sourcing LPDRAM for localized high-speed compute processing, NOR Flash for reliable near-instant system boot-ups, and UFS NAND for high-capacity, ruggedized storage.

Those are core components, not side extras. They sit right next to the computing and storage functions that are becoming standard in newer vehicles, which gives Micron a more central role in the auto supply chain.

Also, Micron has signed a long-term Strategic Customer Agreement (SCA) with Ford Motor Company (F). That deal is meant to secure memory and storage solutions for Ford’s next-generation vehicle lineup and keep that supply stable over time.

There is a clear supply angle here as well. Micron is boosting output of key automotive memory products, with new capacity meant to support long product lifecycles and keep critical vehicle programs supplied.

Taken together, these moves make Citi’s thesis easier to follow.

Analysts Still See More Room in MU

Wall Street clearly is not treating MU like a name that has already topped out. The next big check‑in is Sept. 22, when Micron is due to report earnings again. For the current quarter ending in August 2026, analysts are calling for average EPS of $31.06, versus just $2.86 a year earlier, which works out to an eye‑popping 986.01% growth rate.

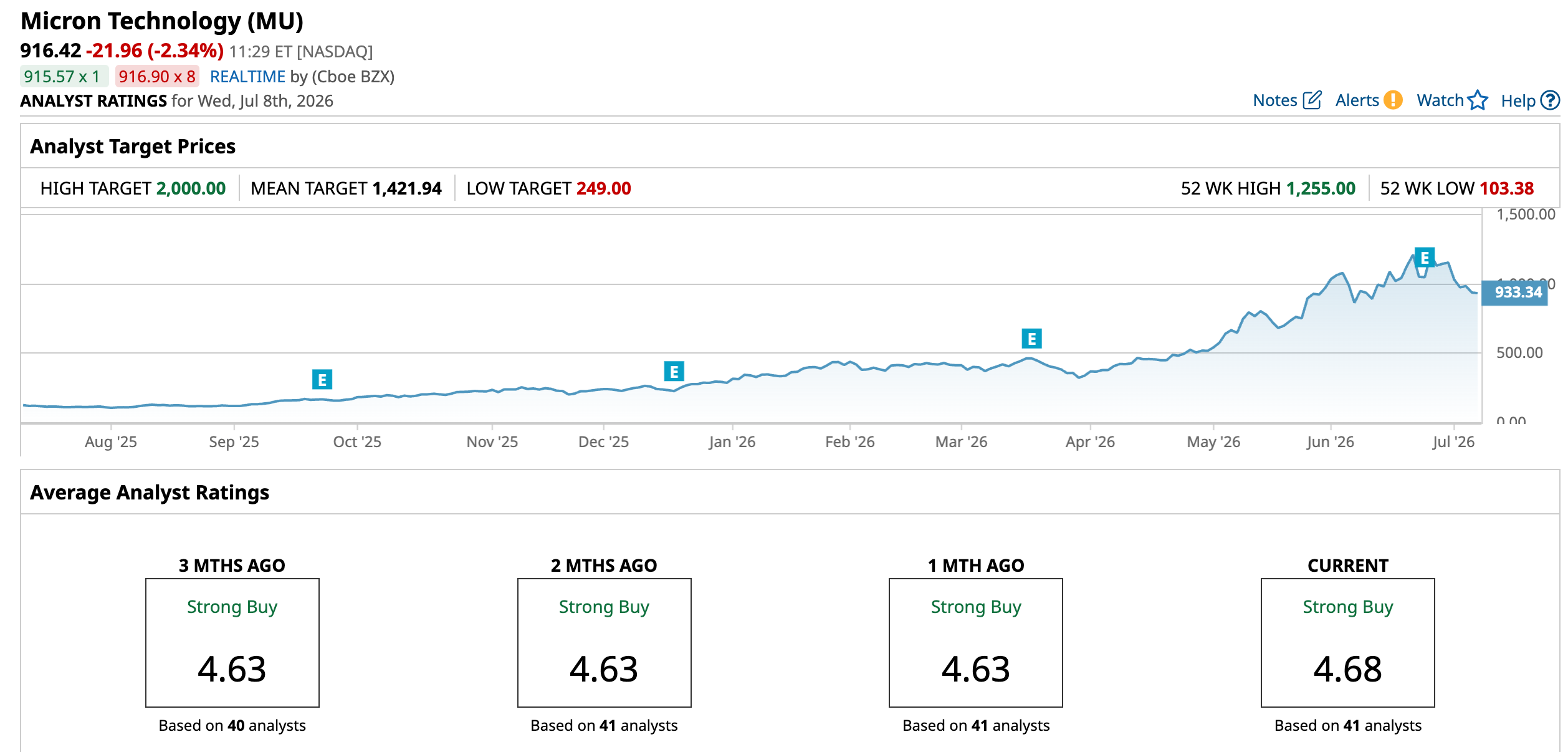

After Micron’s blowout report, Dan Ives lifted his price target on the stock to $1,400 per share, implying 53% upside from recent levels. Stifel has stayed positive as well, keeping its “Buy” rating in place and highlighting Micron’s Strategic Customer Agreements, or SCAs, as a key pillar of the bull case.

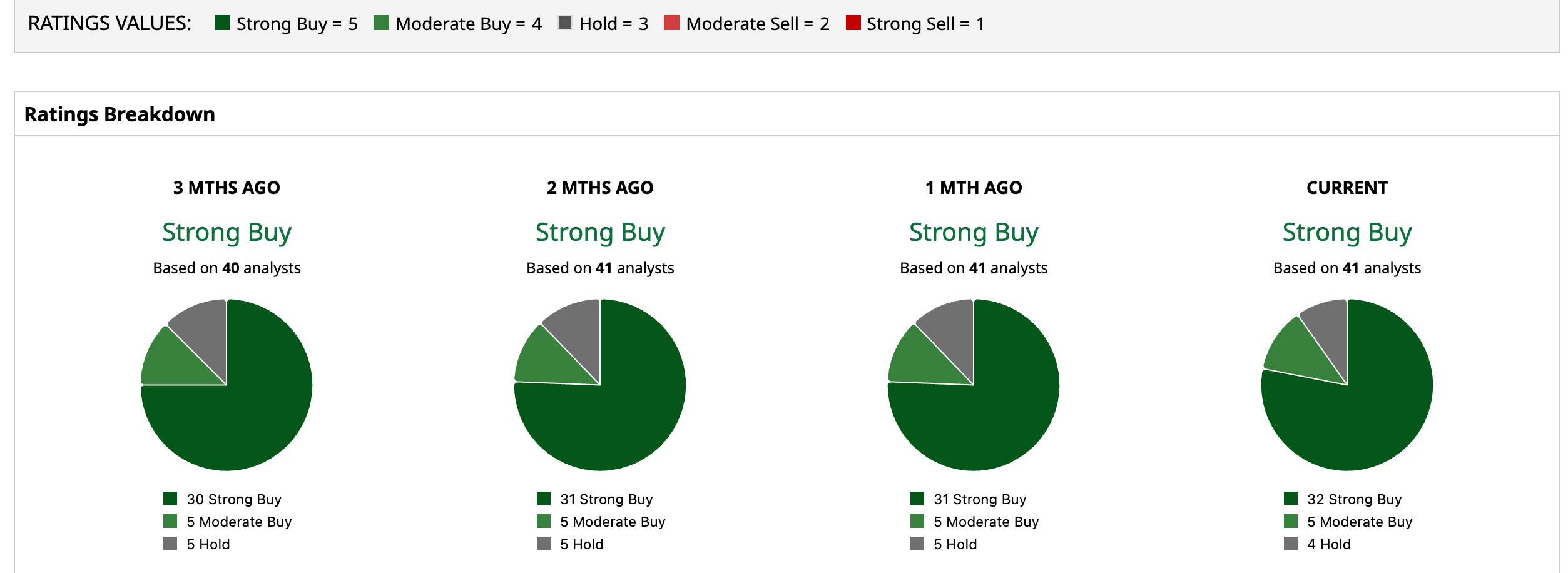

The broader consensus remains firmly bullish. MU carries a consensus “Strong Buy” rating based on 41 analyst opinions. Their average analyst price target stands at $1,421.94, which points to 55.2% upside from here and backs the idea that many pros still see more room for this rally to extend.

Conclusion

Citi’s call suggests Micron still has room to run, not just a good story on paper. Strong earnings, rising DRAM prices, and tighter customer relationships all support a bullish view on MU stock.

The most likely direction from here still leans higher, especially if pricing holds up and Micron keeps beating expectations. After such a big move, the stock probably will not climb in a straight line. Even so, the overall picture still points to more strength than weakness in the shares.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)