/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Artificial intelligence has been the leading story of Meta Platforms (META), with Meta receiving praise (and critique) from the market for allocating up to $145 billion in capital expenditures to invest in building AI infrastructure. That story received new fodder for the bears last week when CEO Mark Zuckerberg commented during an internal town hall that AI agent development of Meta hasn't been moving "in the way we expected" over the past four months.

That comment came just a few days after the news that Meta intends to rent extra AI computing capacity through the cloud business, raising questions on whether AI infrastructure investments are outpacing the demand. Nevertheless, the company keeps generating impressive cash flow through its highly profitable advertising business, thus having much more financial flexibility compared to most of its rivals focused on developing AI infrastructure.

About Meta Stock

Meta Platforms is among the world's largest technology firms and owns such famous services as Facebook, Instagram, WhatsApp, Messenger, Threads, and a wide range of products based on artificial intelligence. Headquartered in Menlo Park, California, META has a market cap of approximately $1.47 trillion and is one of the largest public firms on the planet.

Despite the recent rise, META stock is still lagging compared to its 52-week peak. The share price has jumped by more than 8% over the last five trading days and is trading now approximately 18% above its 52-week low level, while the stock is still 23% away from its 52-week high. The weakness in META stock is caused by doubts of investors about the pace of the return of capital invested by Meta in its AI projects while the overall digital advertising business is still incredibly profitable.

If looking at the valuations, META is trading with relatively moderate ratios for the firm posting revenue growth above 30%. The stock is trading at 20x P/E and 19.8x forward P/E ratios, together with a PEG ratio of 1.03. Considering also that the company has a 36.9% ROE, 30.1% profitability, and 0.24 debt/equity ratio, the valuation looks rather moderate compared to many other AI-focused technology rivals despite its huge investments.

Meta Beats on Earnings

Meta announced another solid quarter during Q1 2026. Revenues grew by 33% year-over-year (YoY) and reached $56.31 billion from $42.31 billion in the prior year period. Net income jumped 61% to $26.77 billion, while diluted earnings per share increased 62% to $10.44 against $6.43 per share reported a year ago.

Operationally, things are going well for the company too. Family Daily Active People (DAP) are now at the level of 3.56 billion people, while ad impressions increased by 19%, and the average price per ad was up by 12%, proving that Meta is successfully monetizing its huge user base despite fears about the entire advertising industry.

Management repeated its expectations that revenues in the next quarter would reach between $58 billion and $61 billion and maintained its outlook on the full-year operating income to beat 2025 levels. In addition, Meta increased its guidance on 2026 capital expenditures to $125 billion-$145 billion, citing increased component prices and more investments in data centers to support future AI capacity.

Nevertheless, the comments made by Zuckerberg provide additional information about those investments. According to Reuters, the CEO noted that AI agent development has not accelerated as expected in the past several months and stated that recent reorganizational changes did not produce the expected results. That shows that maybe Meta's biggest problem is not AI infrastructure financing but creating commercially successful AI projects based on said record investments.

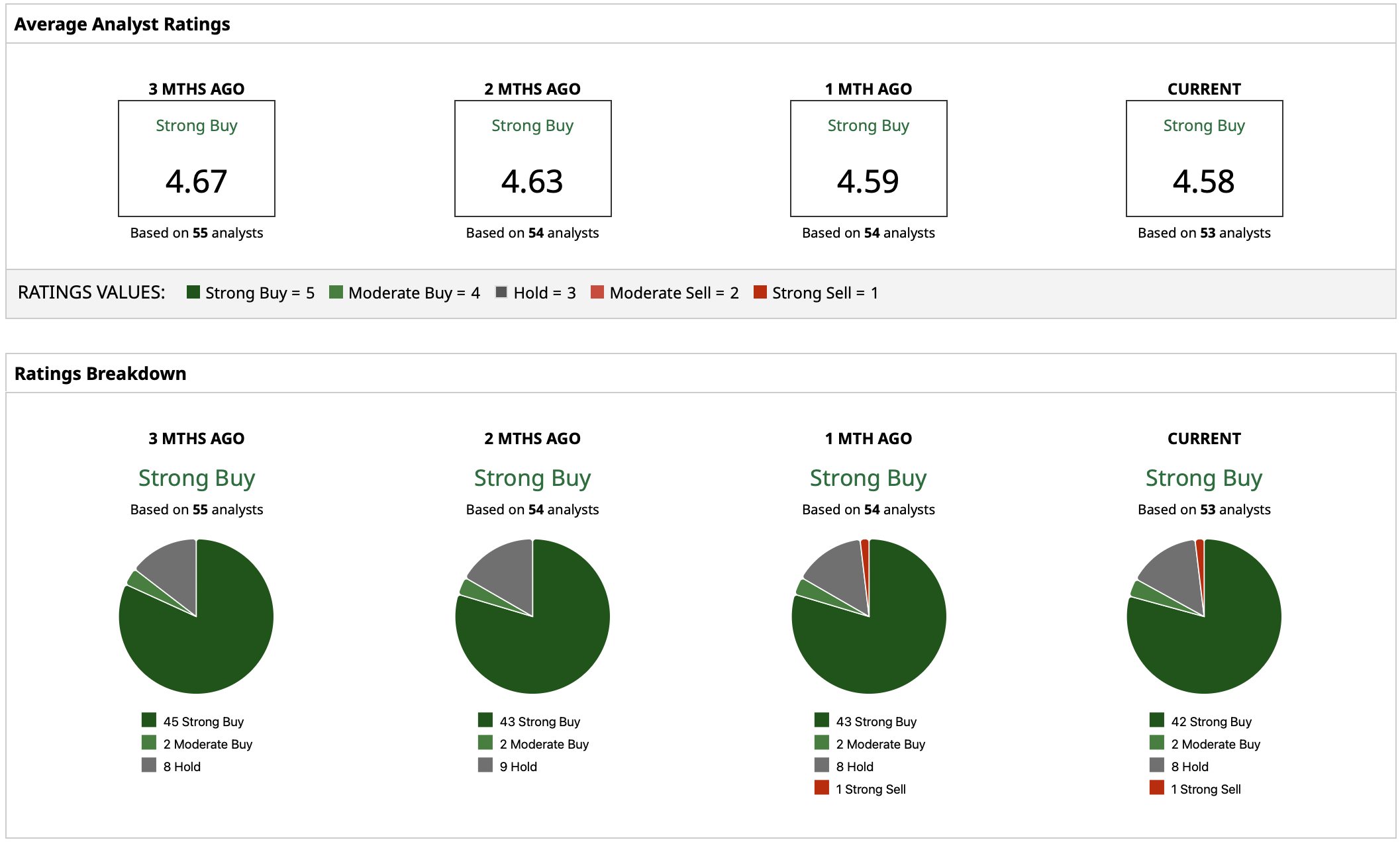

What Analysts Say About META Stock

Analysts assign a “Strong Buy” rating consensus based on the belief that its advertising franchise will allow the company to fund the largest AI project in the industry. Currently, the mean analyst price target is at $823.60. That suggests an upside of approximately 35% to META's current share price of about $610, while the highest published target reaches $1,015.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)