/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

Global cloud infrastructure spending hit $129 billion in the first quarter of 2026, up 35% year-over-year (YOY), because companies are spending more than expected on compute, storage, and AI.

Big tech spending plans for 2026 just got bumped up from about $600 billion to approximately $750 billion after the latest earnings season. That is a 67% jump for the year, and 2027 projections are already closing in on $1 trillion.

This has caught the attention of Jefferies. The firm has a “Buy” rating and a $675 price target on Microsoft Corporation (MSFT), and it says the company is pulling ahead of the rest as cloud spending stays strong.

Azure is taking market share too. In Microsoft's fiscal third quarter of 2026, Azure revenue jumped 40% YOY, beating what analysts expected. Azure now holds roughly a 21% share of the global cloud infrastructure market, putting it second behind Amazon (AMZN) Web Services. Demand for Azure is still stronger than what Microsoft can supply right now.

With Jefferies Financial Group calling Microsoft a standout in the cloud spending boom and Azure taking more market share, is this a stock that the market is still undervaluing?

Financial Strength in Focus

Microsoft makes most of its money from cloud services, business software, and tools that help companies run day to day, with Azure and Microsoft 365 at the center of that setup.

The stock, though, has had a rough stretch. It is down 22.6% over the past 52 weeks and 20.2% so far this year.

At today’s levels, Microsoft Corporation trades at a forward price-to-earnings ratio of 20.25 times, below the sector average of 24.61 times, which makes the valuation look relatively cheap. Income investors also get a steady stream of cash.

The company pays a quarterly dividend of $0.91, last paid on May 21, with a 0.91% yield versus a 1.37% average for the technology sector and a forward payout ratio of 21.42%. Microsoft has raised its dividend for 24 straight years, which helps it stand out as both a growth and income name.

The March 2026 quarter was strong. Revenue rose 18% to $82.9 billion, and operating income increased 20% to $38.4 billion. Net income jumped 23% to $31.8 billion, with earnings per share at $4.27, also up 23%, showing that profits are growing faster than sales.

Microsoft Cloud revenue came in at $54.5 billion, up 29%, and commercial remaining performance obligations nearly doubled, up 99% to $627 billion, pointing to heavy demand locked in for the future. Intelligent Cloud revenue grew 30% to $34.7 billion, helped by a 40% surge in Azure and other cloud services.

Productivity and Business Processes revenue climbed 17% to $35.0 billion on gains from Microsoft 365, LinkedIn, and Dynamics, while More Personal Computing slipped 1% to $13.2 billion. Even with all that investment, Microsoft Corporation still sent $10.2 billion back to shareholders in the quarter through dividends and buybacks.

Growth Drivers Behind Microsoft

Microsoft Corporation is making sure it has the power it needs to keep Azure growing. The company signed a 20-year power deal with Chevron Corporation (CVX), through Chevron’s Energy Forge One unit, to build Project Kilby in West Texas. The site is expected to deliver about 2.67 gigawatts and will supply dedicated power to Microsoft Corporation data centers. Using equipment from GE Vernova (GEV) and Solar Turbines, a unit of Caterpillar (CAT), the project ranks among the biggest combined power and data center developments in the U.S.

Microsoft Corporation is also using Azure to go deeper into healthcare. Its partnership with the non-profit Mayo Clinic is focused on building an AI model made for healthcare, using Mayo Clinic’s de-identified clinical data, long-term patient insights, and care expertise together with Microsoft’s cloud and AI capabilities. The goal is to help with earlier diagnosis, more tailored treatment decisions, and better patient outcomes, which shows how Azure is moving into more complex and higher-value use cases.

On top of that, Microsoft Corporation is thinking about the people needed to support this buildout. The company expanded its partnership with North America’s Building Trades Unions to offer free AI literacy courses and industry credentials to skilled workers across North America. The program builds on an effort that has already trained 1,500 instructors and now uses union apprenticeship systems and LinkedIn Learning to connect workers to job paths in 34 states, helping make sure the labor side can keep up with Azure’s growth.

Analysts’ Take and Outlook

Microsoft Corporation reports earnings next on July 29. For the quarter ending June 2026, analysts expect earnings per share of $4.21, up from $3.65 a year ago, which is 15.34% growth. For the full fiscal year 2026, the consensus is $16.76 per share compared to $13.64 in fiscal 2025, a 22.87% increase.

Benchmark analyst Yi Fu Lee joined the bull camp in April 2026 with a “Buy” rating, calling Microsoft Corporation a "central player in AI" with a data advantage that Amazon.com, Alphabet (GOOG) (GOOGL), and even OpenAI cannot match.

Lee's argument comes down to the size and reach of Microsoft's product network: one billion Windows users, 300 million Office seats, LinkedIn's professional graph, GitHub's developer community, and Azure's enterprise footprint, all of which keep building on each other over time.

Wedbush analyst Dan Ives sees it the same way, giving an “Outperform” rating and holding a $575 price target. Ives points to the company's expanding AI revenue run rate and says Wall Street keeps underestimating Azure's growth story.

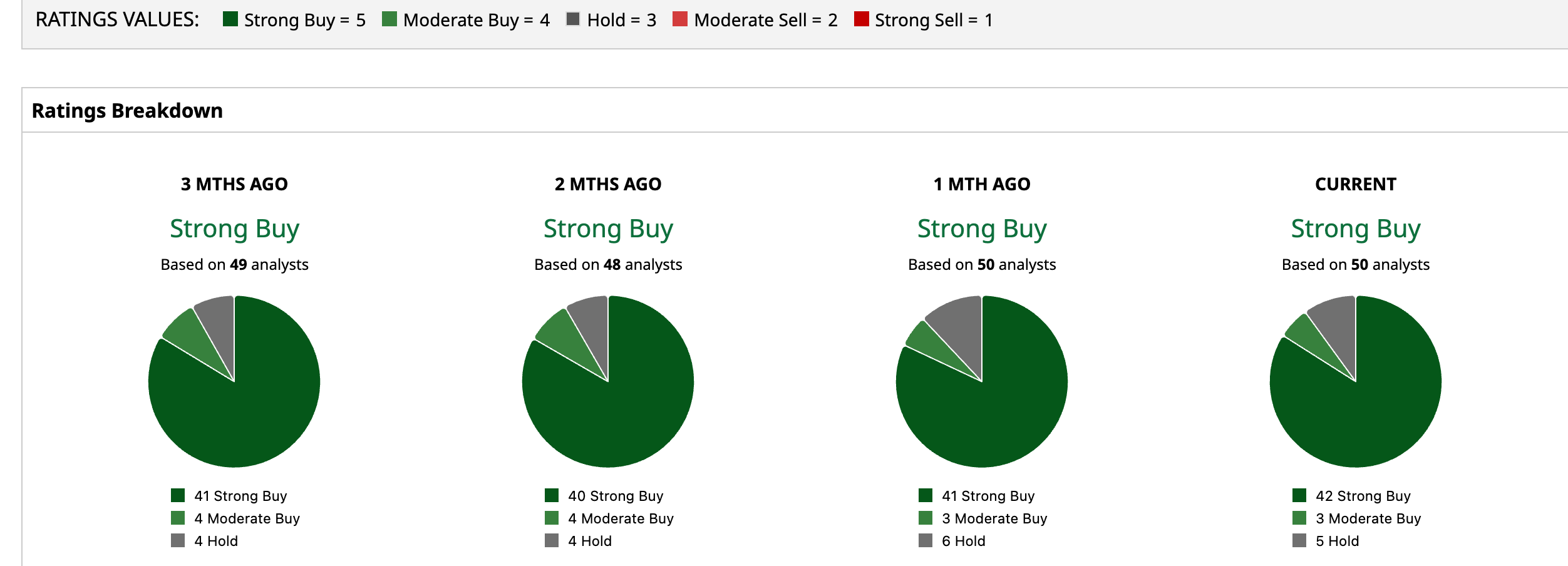

Across the board, analyst opinion is overwhelmingly positive. Of 50 analysts surveyed, a consensus gives MSFT a “Strong Buy,” and the average price target of $552.27 implies roughly 43% upside from current levels.

Conclusion

Microsoft still looks undervalued relative to the strength of its cloud and AI business, especially with Azure gaining share and analysts staying firmly bullish. Even with the stock’s recent pullback, the combination of rising cloud demand, strong earnings growth, and a deep pipeline of AI-driven catalysts suggests the market may be underpricing the story a bit. In the near term, shares are more likely to stay supported and trend higher if Microsoft keeps delivering on Azure and cloud growth, though volatility can linger because of heavy spending and a still cautious market.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)