/Facebook%20on%20a%20phone%20by%20geralt%20via%20Pixabay.jpg)

One of the most important stocks in the market (given its size), Meta Platforms (META), continues to be a stock I, and plenty of others, remain very bullish on long-term.

Much of that has to do with the company's rock-solid underlying business. A leading social media and online advertising giant, Meta's ecosystem, consisting of Facebook, Instagram, WhatsApp, and plenty of other key applications the vast majority of us use every day, makes this a company that passes the “toothbrush test” (we need to use it twice a day).

Of course, when a company like Meta gets to a certain size, some investors will balk at its valuation relative to its growth prospects. That's simply because of the law of large numbers—if the majority of the global population is already using a particular widget, a given company will need to either increase its value capture (raise prices or revenue without increasing its operating expenses) or see its share price decline.

That's why I think the company's recent announcement that Meta will be launching its new gaming app, named Pocket, is such a big deal.

What's This Announcement All About?

Meta announced this past week that it will be launching Pocket, a digital gaming app that will allow users to create so-called “gizmos.” These gizmos can be viewed as mini-games, expanding the investable universe (or the ability of creators to expand the gaming market), a move which many in the space have called both innovative, but also potentially dangerous.

Given the rise of online gaming and changing regulatory rules around what's allowed, many companies are looking to step into this market. Being able to create interactive games that are generated, at least in part, by artificial intelligence is a big deal.

Experts have noted that Meta's recent agreement to acquire Altma Sciences' technology via a non-exclusive license has driven this move. That said, I wouldn't be surprised to see Meta's core developer team take on a project to bring this work in-house over the long term. Indeed, given the company's history of creating and developing its own suite of applications, this seems like the logical next step.

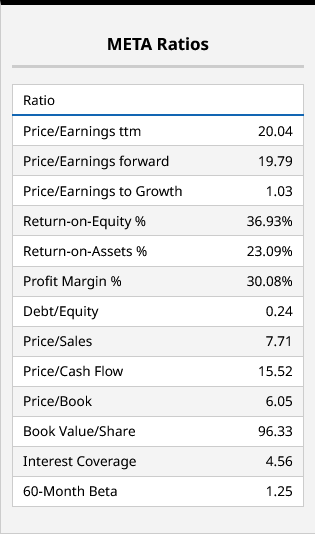

What Do Meta's Fundamentals Say About Its Stock Price?

Currently, Meta's stock price does look relatively cheap, at least compared to some of its mega-cap tech peers. Trading at right around 20 times trailing and forward earnings, there's a solid case to be made that this is a stock that's undervalued, at least compared to its long-term prospects.

This valuation does appear to reflect growing concerns among tech investors that companies like Meta will struggle to maintain cash flow growth, at least over the next five years. Much of that view has to do with the sheer capital spent on artificial intelligence technology and a rollout toward its own AI-driven applications.

Additionally, Meta's recent announcement that it is looking to offload some of its “excess compute” capacity doesn't bode well for the overall narrative around AI spend. Sure, the company's Pocket application is tied to AI and makes sense to me as an organic offshoot of its key investments in this high-growth space. On the other hand, it's also true that investors are clearly and deliberately requiring more in the way of up-front return when it comes to these investments.

At this stage of the game, I think most market participants are continuing to take a cautious view of some of the best blue-chip tech stocks. That's the only way I can personally understand this stock's valuation.

What Do Other Analysts Think of Meta's Growth Prospects?

As it turns out, I'm not the only prognosticator who thinks Meta is undervalued. In fact, the majority of analysts who cover this name happen to have the same view.

With a consensus price target of $823.30 per share, the market is implying META stock has around 40% upside from current levels. A high target of more than $1000 per share implies this stock could climb nearly 75% from current levels over the next year or so. Wouldn't that be an incredible return, though? Investors have seen such surges in the past.

This market looks a lot to me like the 2022 dip we saw from all-time highs. Whether Meta will be able to weather what appears to be a very vicious sentiment storm or not remains to be seen. But for now, this is a stock that does look very attractive at its current multiple, with its range of organic and acquisition-based growth drivers.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)