/Cloud%20Computing%20diagram%20Network%20Data%20Storage%20Technology%20Service%20by%20onephoto%20via%20Shutterstock.jpg)

Datadog (DDOG) is among the leading artificial intelligence (AI) beneficiaries investors have been watching closely this year. I'm certainly one such investor, given the company's surge of nearly 70% over the course of the past year and 90% year-to-date (YTD).

Indeed, the returns investors have seen before the recent tech-led selloff that has proliferated were even higher. Still, Datadog has been among the most resilient of its AI-related peers, now hovering right around the previous all-time high it set roughly one month ago.

The question for many in this market is whether this company's recent performance is indicative of its future potential returns. Analyst Yi Fu Li believes that could certainly be the case, placing a $330 price target on DDOG stock (up from $260 per share) and reiterating a “Buy” rating.

Let's dive into what this price target upgrade means and what this analyst thinks could drive the next leg higher for investors in Datadog moving forward.

Datadog's Strong Moat, Fundamental Strength

Among the key factors driving investor interest in Datadog, and other security and cloud companies for that matter, is the ongoing AI buildout. The idea that some companies have better moats than others in this space is one that's becoming increasingly pertinent for investors, and Datadog is one such name that is being called out as a moat-driven beast in the AI super cycle.

I like that idea, given the company's innovative nature and its sticky customer base. With Li pointing out that Datadog has put forward more than 100 new capabilities for automating operations (where most companies are headed), rising usage of AI agents within the context of security is going to likely drive a much bigger order backlog. Accordingly, there's a solid fundamental basis upon which Li and other analysts/market participants are choosing to buy this stock near all-time highs.

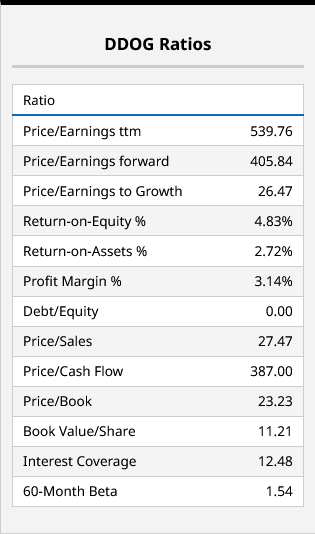

Concerning fundamentals, Datadog is far from cheap. In fact, many investors may consider this name overly pricey, with a forward price-earnings ratio of more than 400 times.

Now, Datadog is a company that's growing its earnings at a clip of around 80% per year, with strong free cash flow generation along the way. In other words, Datadog's earnings growth is highly accretive, and that's something most investors are looking for and demanding right now. So long as this remains the case, and the company's management team can continue to push for improved developer productivity and data observability, there's a case to be made that this robust earnings growth could translate into a reasonable multiple in a few years' time.

Of course, many investors clearly appear to be betting on outlandish earnings beats in the coming quarters that could accelerate such a move. For now, the jury is out on this idea. But Li isn't the only analyst who thinks Datadog could be fairly valued right now.

With that, let's dive into where the other analysts on the Street sit regarding Datadog right now.

What's the Consensus Around DDOG Stock Right Now?

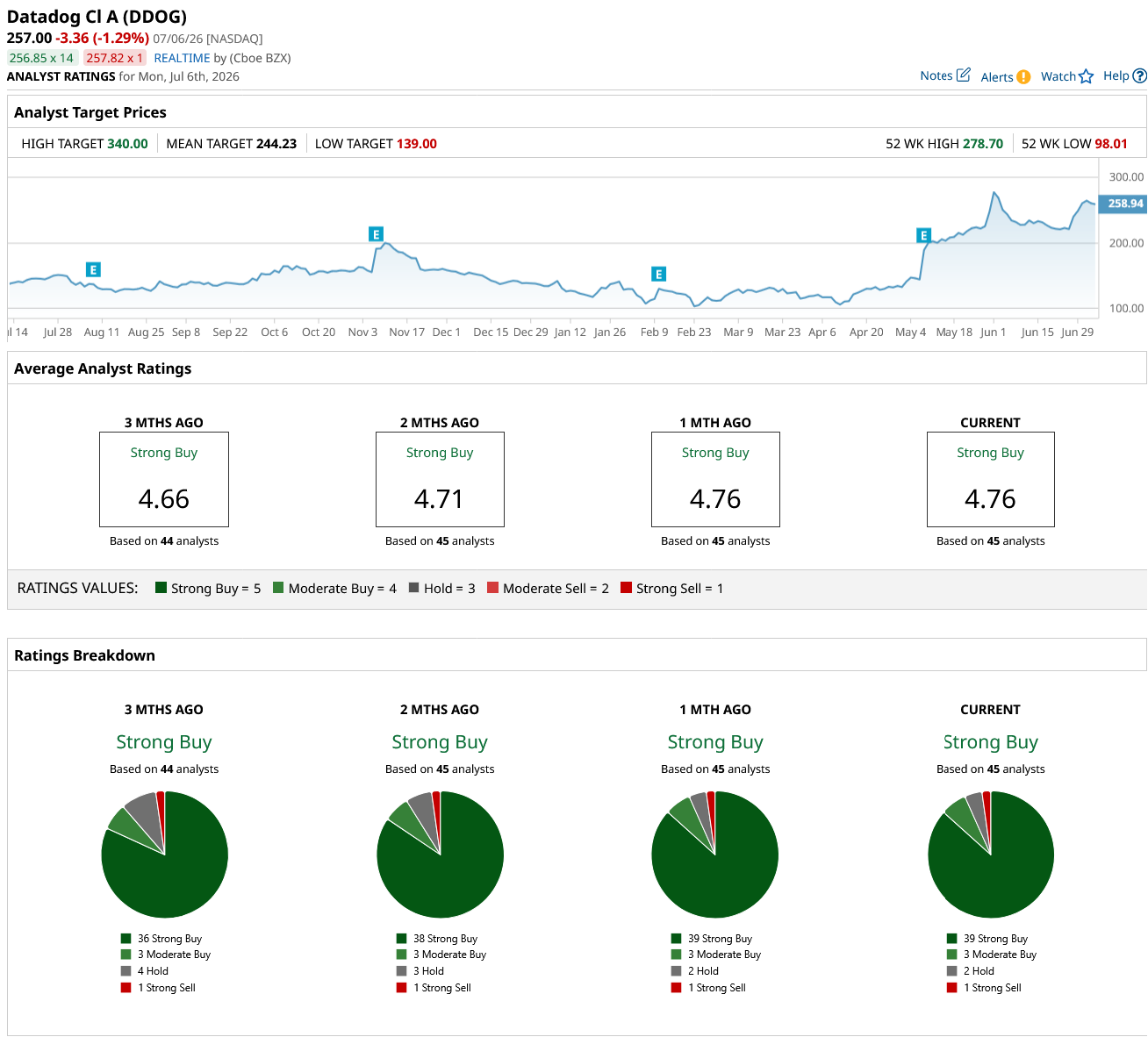

Currently, the mean target placed on Datadog by the 45 analysts who cover this name (pretty wide coverage) sits slightly below where shares of this tech giant are trading right now. In fact, given the speed and voracity of the move higher in DDOG stock, this is now a name that's around 4% above consensus levels.

Now, I think at least some of this has to do with analysts taking time to catch up to Datadog's recent move. Indeed, the price target increase Li put forward (from $260 to $330 per share, near the high of the Street) suggests to me that others are likely to follow suit. In other words, this could be a case of the “tail wagging the dog,” with analysts left scrambling to update their models and factor in what other investors are seeing.

Of course, given the incredible surge in DDOG stock of late, this is a move that some growth-at-a-reasonable-price investors may balk at. I can understand that. But where there's momentum in the market, there will be strategies that pile in. We'll have to see how long this rally goes on for, but for now, Datadog remains a top stock on my watch list.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)