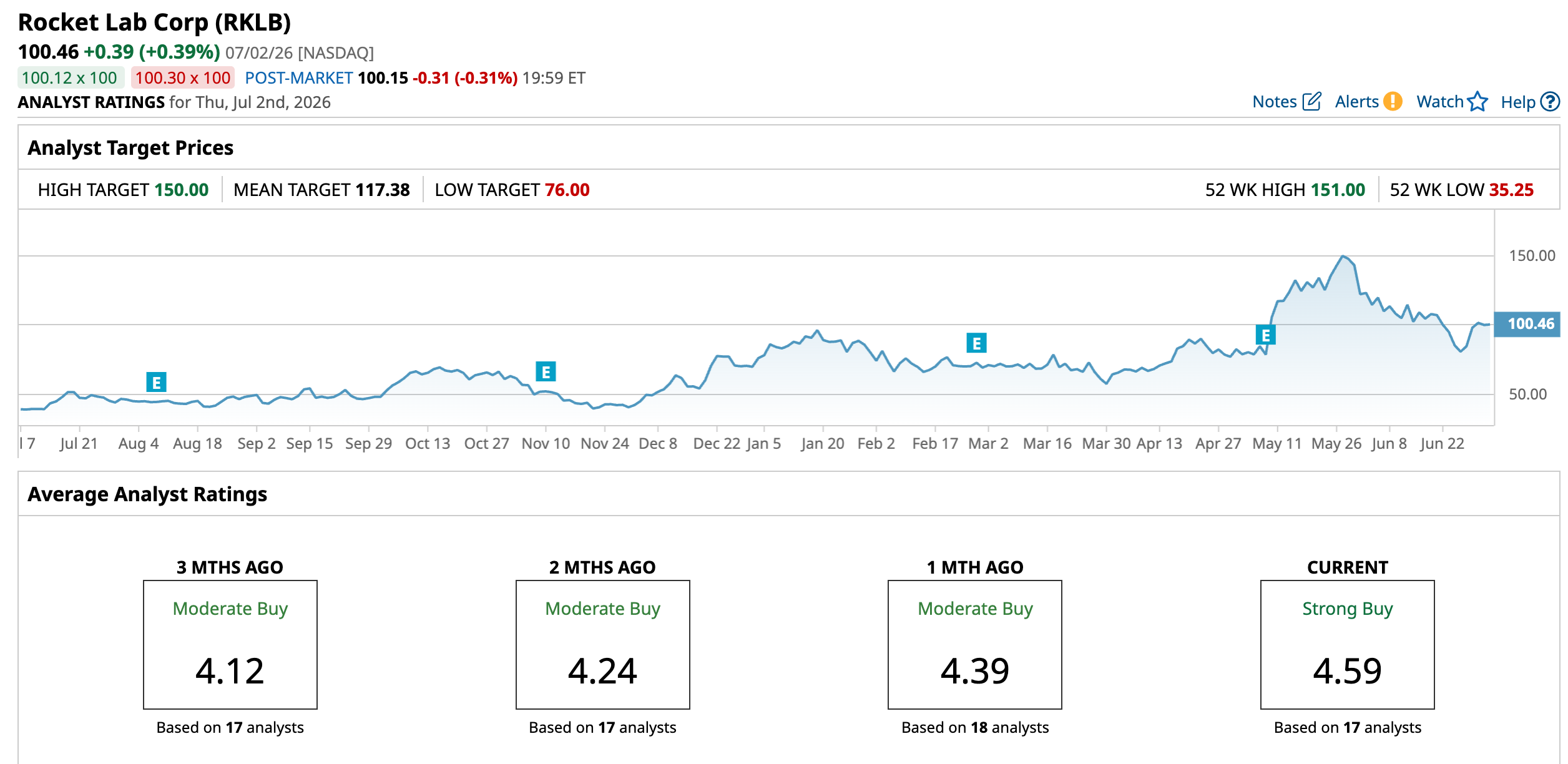

Space company Rocket Lab (RKLB) is standing at an interesting junction now, as the competition between commercial space exploration companies heats up after SpaceX’s (SPCX) blockbuster IPO. New Street Research analysts had already shown considerable faith in these companies, with Rocket Labs notable among them. New Street Research gave the company a bullish “Buy” rating and a Street-high $150 price target, which implies a 51.24% upside from current levels.

Rocket Labs recently announced a mega acquisition of the leading provider of global voice, data, and positioning, navigation, and timing (PNT) satellite services, Iridium Communications (IRDM). This gives the company an instant foothold in space-based applications, with a 500-plus-strong partner ecosystem to create a competitive, vertically integrated space company. The acquisition has the potential to unlock new markets for Rocket Labs by strengthening its vertical integration.

Last month, the company also launched another satellite into orbit for the Japan-based Earth observation company Synspective. This was Rocket Lab’s 12th launch of the year and took its overall launch tally to 91 missions.

About Rocket Labs Stock

Rocket Lab is a space company focused on building and launching rockets, developing spacecraft, and supplying satellite systems for commercial, government, and defense customers. It works across launch services, space systems, and related hardware, helping customers place payloads into orbit and support missions after launch.

Additionally, the company handles spacecraft assembly, testing, and integration, which gives it a broader role than a launch provider alone. Rocket Lab is headquartered in Long Beach, California, where a large part of its core operations is based. It has a market capitalization of $58.14 billion.

Over the past 52 weeks, the stock has gained 181.6%, and it is up 44% year-to-date (YTD). Rocket Lab’s stock has climbed over the past year as investors have rewarded faster launch activity, stronger revenue growth, and a growing backlog of contracts.

However, the stock also dropped 18.54% over the past month, as Rocket Lab has been pressured by profit-taking after a strong run and broader rotation out of speculative growth names. The company’s shares had reached a 52-week high of $151 on May 27, but are down 33.5% from that level.

Rocket Labs’ performance has hiked its valuation to astronomical heights compared to its peers. On a forward-adjusted basis, its price-to-sales ratio of 63.59 times is considerably stretched compared to the industry average of 1.91 times.

Rocket Lab Q1 Results Highlight Strong Momentum in Space Systems and Launch Operations

In the first quarter, Rocket Lab's earnings were record-breaking. The company completed orbital launches and hypersonic test missions, introduced the Gauss satellite electric propulsion system, and was selected to support the U.S. Department of Defense's Space-Based Interceptor program.

The company’s revenue increased 63.5% year-over-year (YOY) to $200.35 million. Its backlog reached a record $2.20 billion, up 20.2% sequentially, while its GAAP gross margin reached a record 38.2%. The company managed to reduce its non-GAAP operating loss from $35.81 million to $18.99 million YOY.

For the current year, Wall Street analysts expect Rocket Lab to report a 23.7% YOY reduction in its loss per share to $0.29, while for the next year, loss per share is expected to decline by 34.5% to $0.19.

What Are Analysts Saying About Rocket Labs’ Stock?

In addition to the faith shown by New Street Research analysts, Rocket Lab has received praise from other Wall Street analysts following its Iridium acquisition announcement. Recently, Cantor Fitzgerald analyst Andres Sheppard reiterated the “Overweight” rating on the stock, reflecting sustained long-term confidence in its performance. Analysts at Bank of America also maintained a “Buy” rating on the stock and raised the price target from $105 to $115.

Roth Capital’s Suji Desilva boosted his Rocket Lab price target to $130 from $100 and kept a “Buy” rating. He said the deal improves Rocket Lab’s competitive standing and gives it a strong advantage versus rivals like SpaceX and Amazon (AMZN), which are also expanding their space-based businesses. The analyst expects Rocket Lab to expand its satellite-based services, which could generate more recurring revenue from long-term contracts rather than relying mainly on one-off launches or sales.

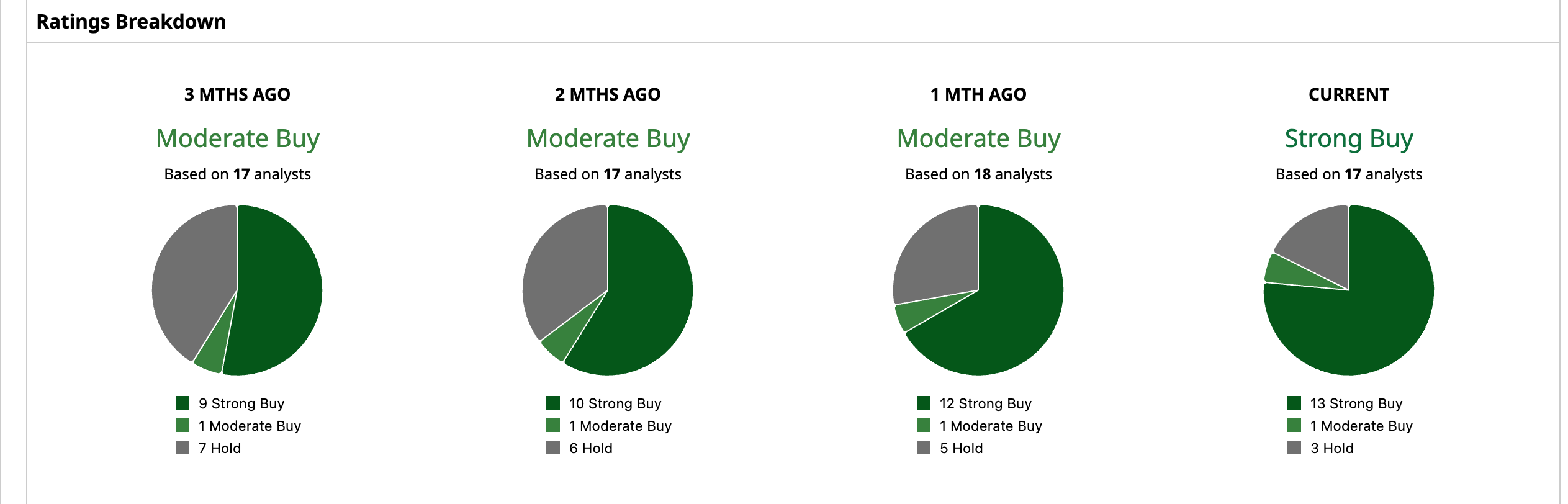

Rocket Lab has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 17 analysts rating the stock, a majority of 13 have given it a “Strong Buy” rating, one a “Moderate Buy,” and three a “Hold.” The consensus price target of $117.38 represents a 16.8% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)