/The%20Adobe%20logo%20on%20a%20smartphone%20screen%20by%20filins%20via%20Adobe%20Stock.jpeg)

Software giant Adobe (ADBE) just experienced some exciting insider activity. Recently, Director David Ricks acquired 10,000 shares of ADBE common stock in an open-market purchase at a weighted-average price of $194.51 per share. This represents an investment of approximately $1.95 million and hikes Ricks’ direct ownership by roughly 130%.

Such confidence from insiders is a good sign for a company that has faced pressure, as investors fear that generative AI will replace SaaS tools. However, Adobe is trying to incorporate more AI into its operations to stay buoyant. This includes a definitive agreement to acquire Topaz Labs, an AI-powered photo and video enhancement tool. This Emmy Award-winning firm has earned its popularity among photographers and filmmakers.

As the company tries to shrug off AI-related fears, we take a closer look…

About Adobe Stock

Adobe is a global software company best known for tools that help people create, edit, and manage digital content. Its products span creative software, document services, and enterprise platforms for marketing and customer experience. The company has also been leaning more into artificial intelligence, adding generative features, and expanding partnerships to improve how businesses create and deliver content.

Adobe continues to focus on cloud-based services and workflow automation, which are central to its growth strategy. Headquartered in San Jose, California, it has a market capitalization of $87.34 billion.

Investors have grown more cautious about Adobe’s growth outlook and competitive position. There have been growing worries about AI disrupting traditional SaaS demand, intensifying competition from peers and newer creative tools, analyst downgrades, and concerns about leadership transition following CEO Shantanu Narayen’s planned departure announcement.

Over the past 52 weeks, Adobe’s stock has declined 42%, while it is down 37.2% year-to-date (YTD). The company’s shares reached a 52-week low of $190.12 on June 18, but are up 15.6% from that level.

The sell-off has also made the stock cheaper than its peers. On a forward-adjusted basis, Adobe’s price-to-earnings (non-GAAP) ratio of 9.0 times is lower than the industry average of 24.60 times.

Adobe Q2 Earnings Topped Estimates

For the second quarter of fiscal 2026 (quarter ended May 29), Adobe’s total revenue increased by 12.7% year-over-year (YOY) to $6.62 billion, which is higher than the $6.46 billion that Wall Street analysts had expected. This was based on subscription revenues increasing by 13.7% from the prior-year period to $6.42 billion.

Total Adobe ARR at the end of the quarter was $27.10 billion, including approximately $480 million from its newly acquired brand-visibility firm, Semrush. The company also had an RPO of $22.27 billion and a cRPO of 67%. Adobe’s Q2 non-GAAP EPS was $5.96, up 17.8% YOY and exceeding the $5.83 that Street analysts expected.

For the current fiscal year, Adobe expects total revenue in the $26.50 billion to $26.60 billion range, with ending ARR growth projected at 10.2% YOY. Its total non-GAAP EPS is expected to be in the $24.35-$24.45 range.

Wall Street analysts are optimistic about Adobe’s future earnings. They expect the company’s EPS to climb by 13.3% YOY to $4.86 for the current quarter. For fiscal 2026, EPS is projected to surge 15.1% to $19.80, followed by a 12.8% growth to $22.33 in fiscal 2027.

What Do Analysts Think About Adobe’s Stock?

This month, JPMorgan analysts lowered the price target from $420 to $340, while maintaining an “Overweight” rating on the stock. JPMorgan noted Adobe is increasing investment to seize the bigger long-term AI opportunity, even if that means sacrificing some near-term ARR growth.

DA Davidson analysts lowered the price target from $300 to $250, while maintaining a “Buy” rating. In light of the leadership changes at the company, DA Davidson analysts said the changes could open the door to major strategic shifts aimed at protecting Adobe’s market share and expanding into AI opportunities.

KeyBanc analysts, on the other hand, lowered their price target on Adobe to $195 from $235 while maintaining an “Underweight” rating on the stock. KeyBanc’s Jackson Ader said that although the headline figures beat expectations, the gains looked less impressive once the Semrush acquisition was included. He added that organic results and guidance were solid, but not outstanding.

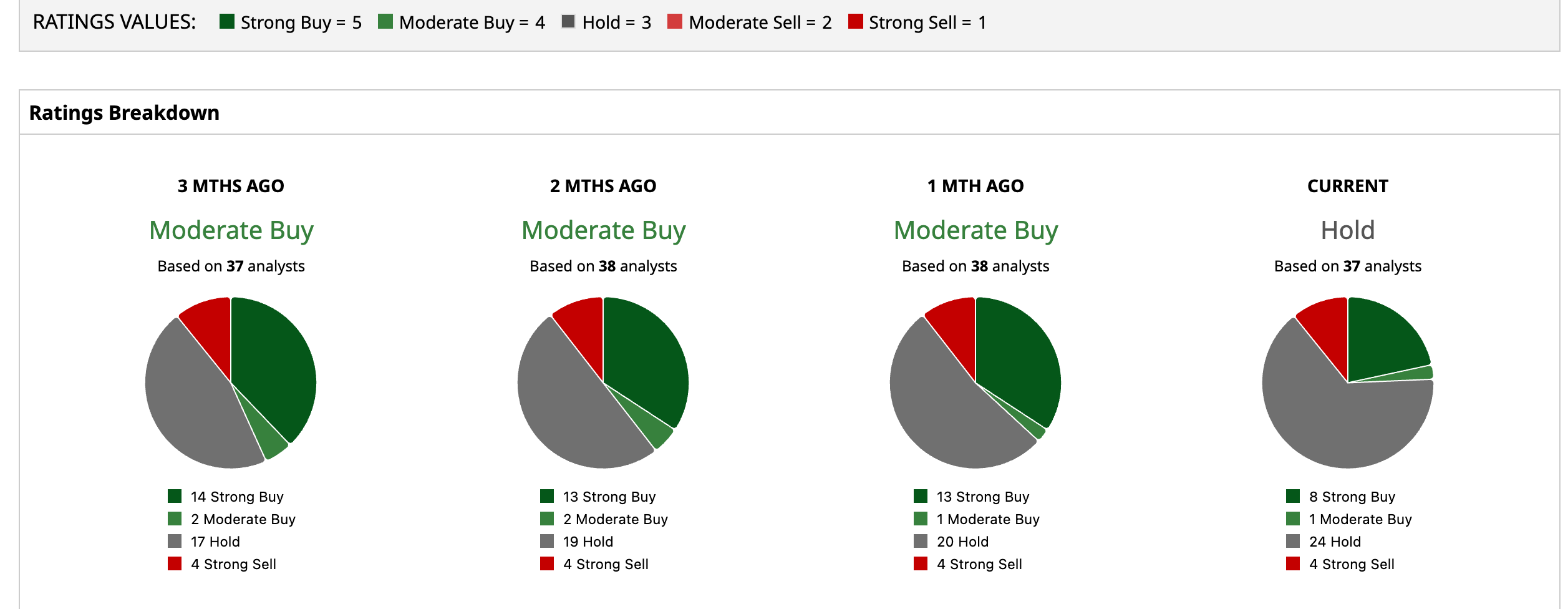

Wall Street analysts are taking a cautious stance on Adobe’s stock now, with a consensus “Hold” rating overall. Of the 37 analysts rating the stock, eight analysts gave a “Strong Buy” rating, one analyst suggested “Moderate Buy,” while a majority of 24 analysts are playing it safe with a “Hold” rating, and four analysts gave a “Strong Sell” rating. The consensus price target of $269 represents a 22.4% upside from current levels. The Street-high price target of $460 implies a 109.4% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)