/Solar%20Panels%20City%20by%20Fuyu%20Liu%20via%20Shuttershock.jpg)

A policy proposal out of Washington has suddenly put the solar industry back in the spotlight. Reports that the Trump administration is weighing a ban on new Chinese-made solar inverters over cybersecurity concerns lit a fire under solar stocks, with investors quickly betting that domestic and non-Chinese manufacturers could be the biggest winners. SolarEdge Technologies (SEDG) was among the names that caught the market’s attention, rallying as traders rushed to price in the possibility of a shifting competitive landscape.

The proposal, still being drafted by the Federal Communications Commission, follows similar restrictions introduced in Europe and reflects growing concerns that foreign-made energy equipment could pose risks to critical infrastructure. While officials stress the move is about protecting the power grid, the debate has also reopened questions about supply chains, trade tensions, and how much the renewable energy industry still depends upon Chinese components.

That naturally brings SolarEdge into the conversation. The company designs smart solar inverters, power optimizers, and energy management solutions that help homes and businesses generate, store, and monitor solar power more efficiently. If Chinese rivals face tougher regulatory hurdles, SolarEdge could find itself in a stronger competitive position. The optimism helped send SEDG stock up 5.56% on Tuesday. That pop adds to what has already been an impressive run for the photovoltaic products maker in 2026.

However, after the surge, it has recently given back some ground, leaving investors wondering whether this is simply a healthy breather or the beginning of another pullback. So, with policy shifts, cybersecurity concerns, and renewed momentum all colliding, is now the right time to snag SolarEdge’s shares, or should investors wait for the dust to settle? Let's take a closer look at how to play SEDG here.

About SolarEdge Stock

Founded in 2006 and headquartered in Herzliya Pituach, Israel, SolarEdge Technologies has grown into one of the world’s leading renewable energy technology companies. The company develops smart energy solutions that help generate, store, manage, and optimize electricity across residential, commercial, industrial, and utility-scale projects.

Its portfolio spans solar inverters, power optimizers, battery storage systems, EV chargers, grid services, and AI-powered energy management software, all designed to make clean energy more efficient and reliable. As demand for electricity continues to climb, SolarEdge is positioning itself at the heart of the global transition toward smarter, cleaner, and more resilient energy systems. Its market capitalization currently stands at $3.41 billion.

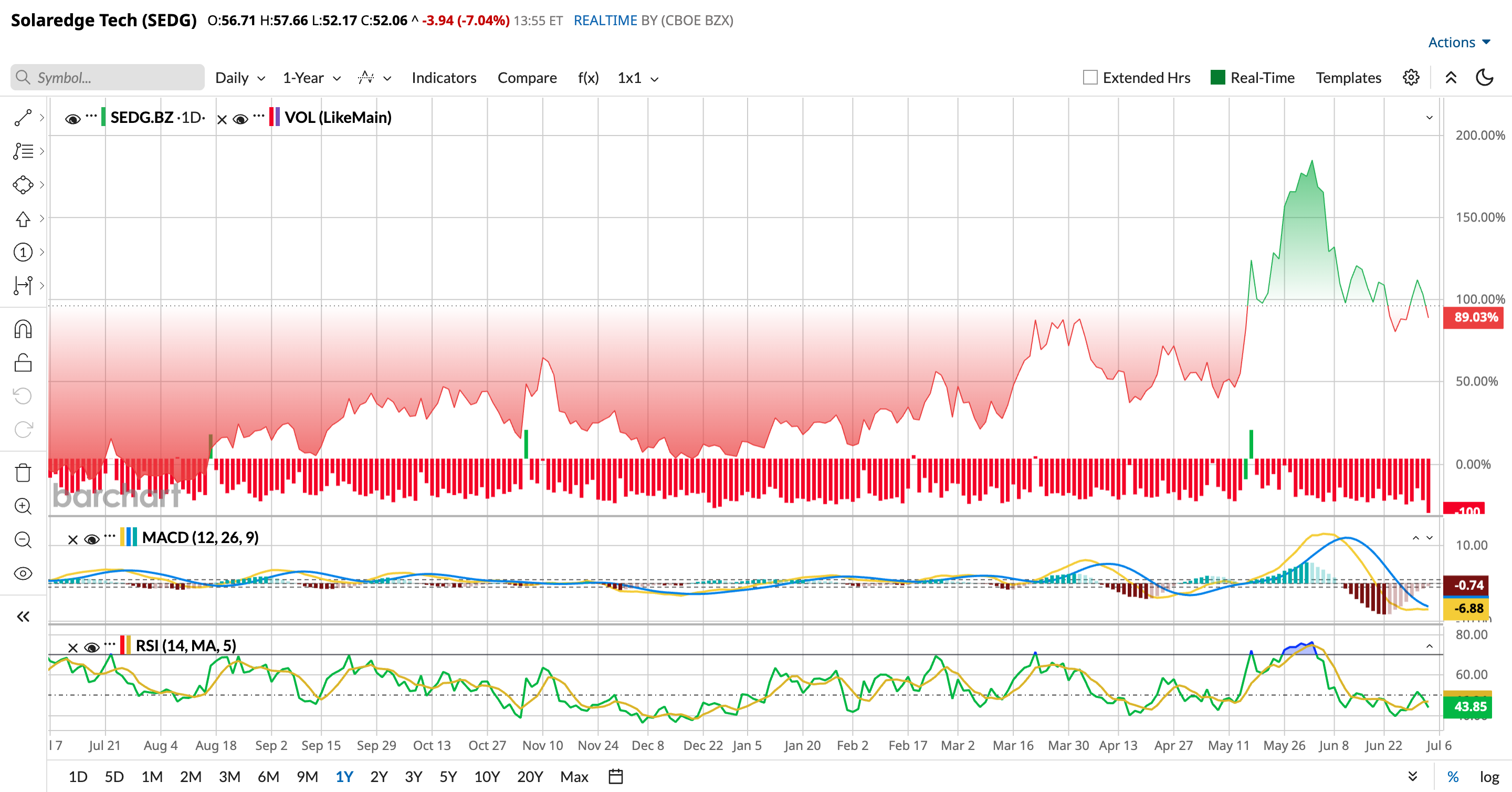

SolarEdge’s shares have been volatile over the past year. After reaching a 52-week high of $81.25 in May, SEDG stock has retreated 36%, proving that even the strongest rallies need to catch their breath. Yet, zooming out tells a far more encouraging story.

The stock has staged an impressive recovery from its February low of $29.43 and is now up 122.12% over the past 52 weeks.

The latest catalyst came from reports that the Trump administration is considering restrictions on Chinese solar inverters, a move that could tilt the competitive landscape in favor of domestic players like SolarEdge.

At the same time, investors are warming to another powerful story – the growing need for solar and other alternative energy sources to help meet AI data centers’ soaring electricity demand – a trend SolarEdge has already identified as a major growth opportunity.

Technically, sentiment has turned more cautious after SEDG’s strong run. The 14-day RSI has retreated to 44.24 from overbought levels seen in early June, indicating the stock's momentum has cooled. Meanwhile, the MACD oscillator has flashed a bearish crossover, with the MACD line very near the signal line as both continue to trend lower. The histogram has flipped into negative territory, suggesting sellers are gradually gaining the upper hand and near-term momentum may remain under pressure.

Valuation offers a brighter spot. Based on its forward price-to-sales ratio, SEDG still looks attractively priced at 2.45 times sales – well below both its sector peers and its own historical average.

A Snapshot of SolarEdge’s Q1 Numbers

On May 6, this global leader in smart energy technology reported its financial results for the first quarter ended March 31. SolarEdge generated revenue of $310.5 million, down 7.4% year-over-year (YOY). Even so, the results topped Wall Street’s expectations. Plus, the company generated revenue from roughly 50.5 thousand inverters, 2.4 million power optimizers, and 331 MWh of batteries for PV applications, underscoring that demand for its core products remains intact.

Profitability also showed meaningful improvement. On a non-GAAP basis, SolarEdge posted a loss of $0.43 per share, a notable improvement from the $1.14 loss reported a year ago, although it still came in weaker than analysts had expected. Excluding a one-time expense of about $14 million, the adjusted loss would have been closer to -$0.20 per share. Meanwhile, adjusted gross profit nearly quadrupled to $68.3 million, while adjusted gross margin expanded to a healthy 23.5%, signaling that the company’s cost-cutting efforts and operational improvements are beginning to pay off.

Operating cash flow came in at $24.4 million, while free cash flow edged up to $20.7 million. Just as importantly, SolarEdge ended the quarter with $246.2 million in cash and investments, net of debt, giving it a stronger financial cushion as it navigates the recovery.

Management also struck an optimistic tone for the current quarter, guiding for revenue between $325 million and $355 million and a non-GAAP gross margin of 23% to 27%.

Wall Street expects the recovery to continue, forecasting losses to shrink by 69.1% YOY to -$1.12 per share in fiscal 2026 before the company swings back to a profit of $0.34 per share in fiscal 2027.

What Do Analysts Expect for SolarEdge Stock?

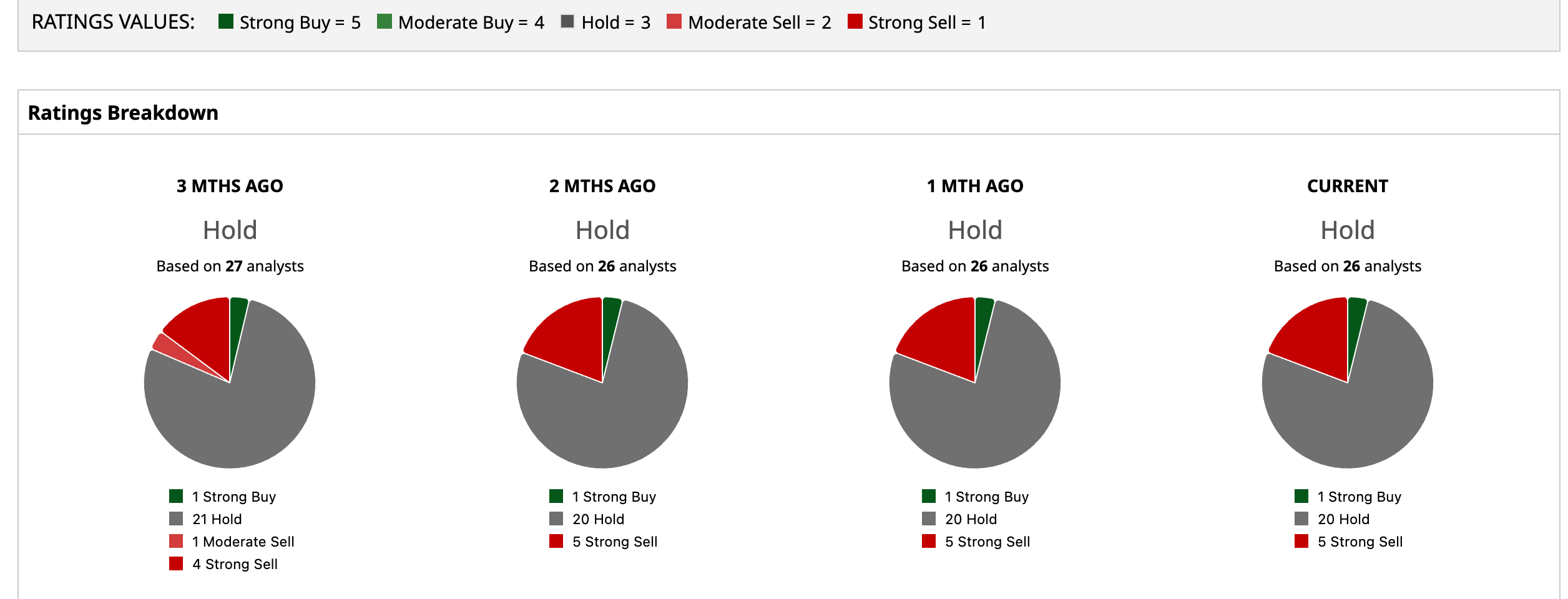

Overall, Wall Street is taking a wait-and-see approach to SolarEdge, assigning the stock a consensus “Hold” rating. Of the 26 analysts rating the stock, just one analyst rates it a “Strong Buy,” 20 advise a “Hold,” while the remaining five analysts are outright skeptical, recommending a “Strong Sell” rating.

SEDG stock trades above the mean price target of $41.30, but the Street-high target of $85 implies the stock could rise as much as 53.1%.

Final Thoughts on SEDG Stock

SolarEdge looks like a stock that’s caught between a promising future and a market that still wants proof. The policy headlines are clearly working in its favor, its financials are improving, and the AI-powered energy story could become a meaningful long-term tailwind.

On the flip side, the recent rally has already priced in some of that optimism, while the technical charts suggest the stock may need more time to reset. So, chasing the latest pop may not be the smartest move. Instead, patient investors may want to keep SEDG on their watchlist and consider buying on pullbacks.

If the proposed regulations move forward and SolarEdge continues to improve its business, the current pullback could end up being just a temporary pause rather than a sign that the rally is over.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)