FuelCell Energy (FCEL), headquartered in Danbury, Connecticut, is a global leader in delivering sustainable, low-carbon fuel cell technology. Founded in 1969, the company designs, manufactures, installs, and services stationary fuel cell power platforms that utilize electrochemical processes rather than combustion to generate ultra-clean electricity and heat. Operating at the intersection of the hydrogen economy and decentralized power generation, FuelCell Energy provides baseload energy, microgrid reliability, and carbon capture solutions.

Recently, the company transformed its growth roadmap by targeting AI-driven data infrastructure, establishing its heavy-duty fuel cells as critical, independent utilities for massive tech-sector installations.

FuelCell's Historic Rally

FCEL stock's price reflects intense volatility coupled with a dramatic, catalyst-driven retail and institutional re-rating. The equity surged to $37.88 on Tuesday, hitting a new high for its 52-week trading range of $3.78 to $37.88. Fueled by aggressive short-covering and a fundamental pivot toward powering tech infrastructure, the stock has posted an explosive near-term recovery. However, structural capital requirements and persistent historical losses continue to weigh heavily on long-term equity valuations, leaving the asset with negative multi-year returns.

In comparison to the broader market, FuelCell Energy has delivered immense, highly speculative near-term alpha after years of deep structural underperformance. While standard equity indices experienced standard macroeconomic corrections, FCEL completely decoupled from index trends via targeted, independent contract wins. It provides concentrated exposure to the clean energy transition, though it remains highly sensitive to localized regulatory shifts and short-interest dynamics compared to diversified market averages.

FuelCell Energy's Q2 Results

FuelCell Energy reported financial results for its second fiscal quarter ended April 30, 2026, showcasing a transition phase characterized by short-term margin compression alongside massive pipeline expansion. Total quarterly revenue declined 4.9% year-over-year (YoY) to $35.59 million, slightly below Wall Street estimates due to timing dependencies in platform shipments. The net loss attributable to common stockholders widened to $78.71 million ($1.45 per diluted share), heavily impacted by a $42.6 million asset impairment at its Groton facility and elevated capital expenditures directed toward scaling manufacturing facilities.

Despite near-term bottom-line pressure, operational backlogs and forward-looking infrastructure indicators reached historic highs. The company's total order book stood at a robust $1.14 billion, anchored by multi-year generation and international service agreements. Crucially, management significantly accelerated its commercial roadmap by securing a massive, milestone 380-megawatt clean power agreement with Fit Energy to supply baseload infrastructure to AI data centers, alongside a $49 million export financing package. Backed by an active deployment strategy, management is targeting an annualized production run rate of 100 megawatts at its Torrington plant by late October 2026, establishing a strong path toward long-term monetization.

FuelCell's Stock Spikes on Another Upgrade and Export Win

FuelCell Energy shares skyrocketed almost 65% over three days following a dual wave of bullish institutional catalysts. The surge was ignited after the Export-Import Bank of the United States (EXIM) approved a $49 million non-dilutive financing package to fund clean energy exports to South Korea. Compounding this momentum, B. Riley upgraded the stock from “Neutral” to “Buy,” aggressively raising its price target from $13 to a Street-high $32, a potential downside of 3% from its market price.

The upgrade directly reflects heightened confidence in FuelCell’s massive data center pivot. The company recently secured a landmark agreement with Fit Energy USA to deploy up to 380 megawatts of clean, baseload power to support advanced AI computing infrastructure. B. Riley analyst Ryan Pfingst noted that the firm order strongly validates FuelCell's ability to monetize the data center sector, forecasting positive EBITDA generation for the company by the second half of 2027.

What’s the Verdict on FCEL Stock?

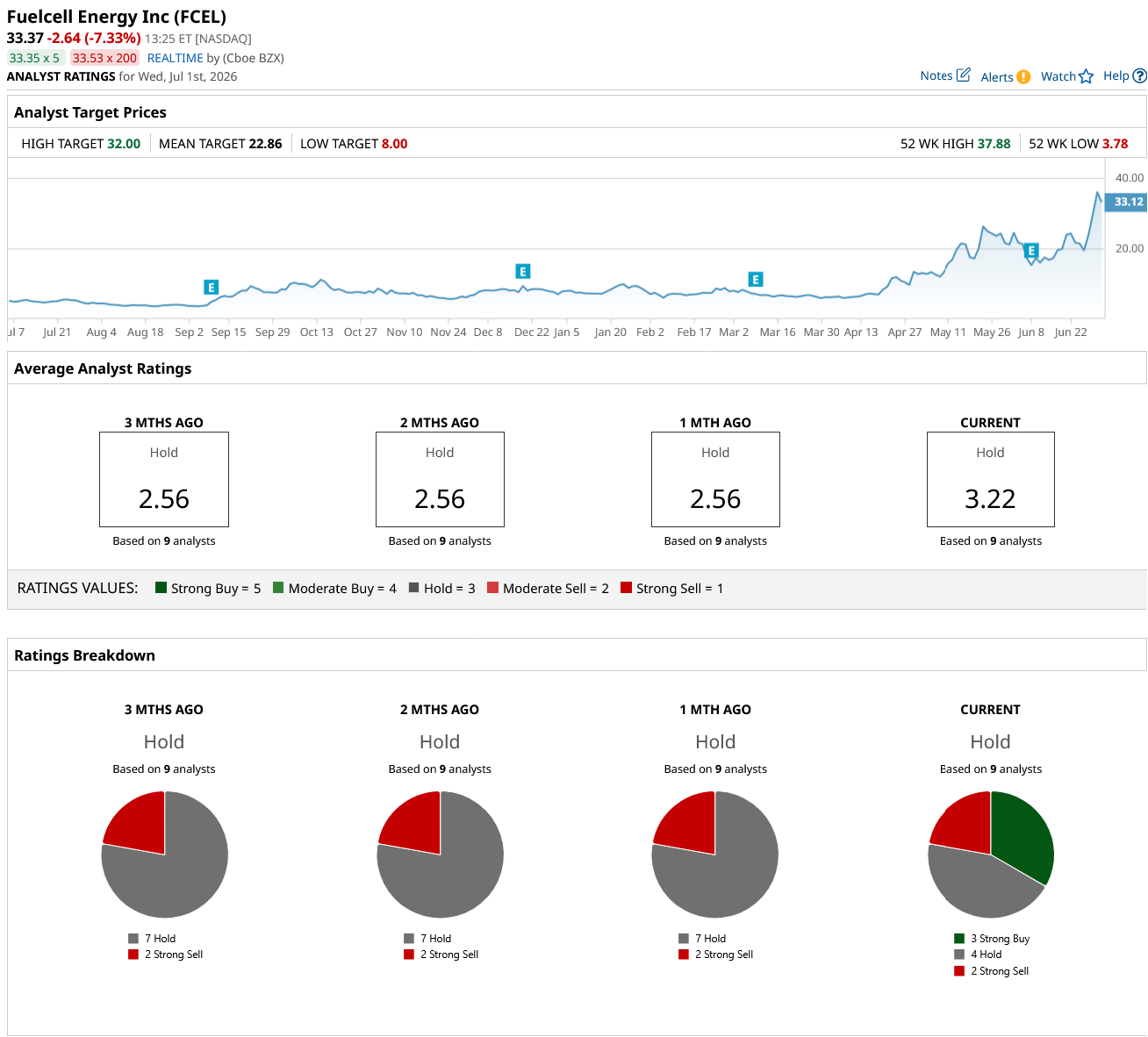

The massive data center pivot and B. Riley’s aggressive upgrade validate FuelCell Energy’s emerging role in the AI infrastructure boom; this momentum builds directly on top of an upgrade from Jefferies just days prior. However, broader Wall Street remains highly skeptical, maintaining a cautious consensus "Hold" rating on FCEL stock. Across nine analyst evaluations, sentiment is sharply split between three "Strong Buy," four "Hold," and two "Strong Sell" ratings. With a mean price target of $22.86, the stock faces a steep 32% projected downside from its current overheated market price.

Until massive pipeline agreements convert into consistent profitability, FCEL stock remains a highly speculative vehicle.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)