/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20and%20cabinets%20full%20of%20hard%20drives%20inside%20large%20data%20center%20by%20IM%20Imagery%20via%20Shutterstock.jpg)

FuelCell Energy (FCEL) is a clean energy technology company operating as a global leader in molten carbonate and solid oxide fuel cell platforms, generating clean, reliable, on-site baseload power. The company has rediscovered itself, undergoing a decisive AI-transformation as it now positions its carbonate fuel cells as the answer to the power crisis in the global AI infrastructure. Its carbonate fuel cells generate power in the direct current (DC) form, delivering nearly 800 volts directly into AI servers, giving a critical advantage over the traditional grid.

Founded in 1969, it is headquartered in Danbury, Connecticut.

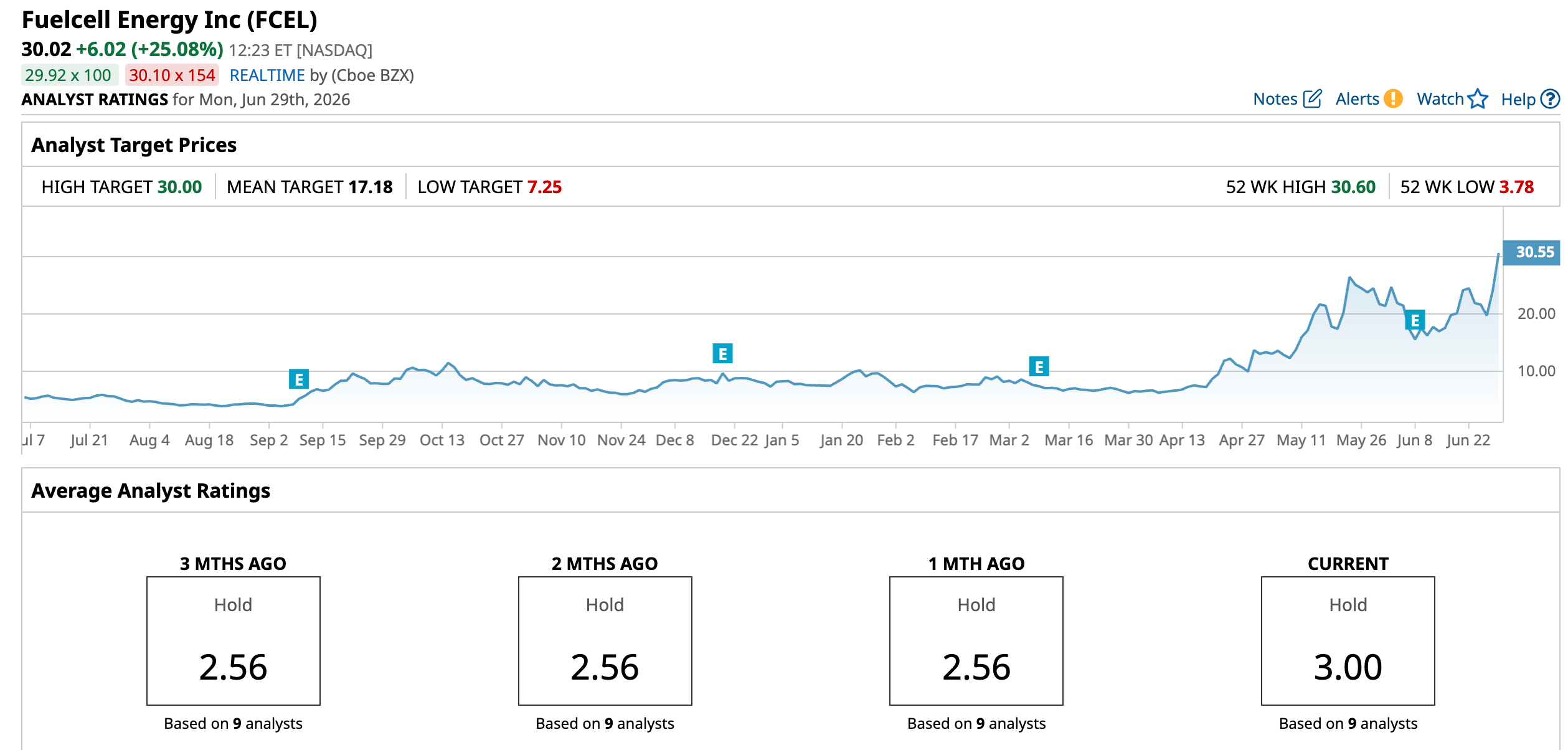

FuelCell Stock Outperforms Market

FuelCell’s 52-week range stands between $3.78 and $30.80, showing strong recovery from lows and gaining 431%, fueled by AI data center power demand optimism. The stock saw its biggest single-session surge of 20% in mid-May as investors' optimism surrounding AI data center power demand resulted in a broader fuel cell sector rally.

Compared to the Russell 2000’s (IWM) 21% gain in 2026, FCEL has largely outperformed the small-cap benchmark on an absolute basis. However, the stock’s extreme volatility, pre-profitability status, and widening quarterly losses demand careful risk management from investors.

FuelCell Shares Popped on Results

FuelCell posted its second-quarter results on June 8, posting a revenue of $35.6 million, down 5% year-over-year (YOY), while also missing estimates of $40.51 million. Earnings for the quarter totaled -$0.53 per adjusted share, also missing analyst estimates of -$0.43 per share. However, despite the dual miss, results were headlined by a 267% quarter-over-quarter surge in sales pipeline reaching 4 gigawatts, with data center representing 89% of total submitted proposals, resulting in a stock spike of 12.84% on results day.

Net loss widened to $78.7 million, from $38.8 million reported in the same quarter last year, significantly influenced by a $42.6 million non-cash impairment charge for the Groton project. FuelCell ended the quarter with a cash reserve of $440.9 million, enough to fund its expansion projects.

The Torrington, Connecticut manufacturing hub is eyeing 500 MW annualized capacity, requiring $200-$275 million investment in the next 24 months, while two carbon capture modules have made way to ExxonMobil’s (XOM) Rotterdam facility. Management is closely watching positive EBITDA post-Torrington plant expansion, with a future expansion plan of 1 gigawatt capacity as demand increases.

Jefferies Upgrades FuelCell

FuelCell Energy stock jumped 20% after Jefferies analyst Julien Dumoulin Smith upgraded the stock from “Hold” to “Buy” rating while raising its price target to $24, citing the landmark Fit Energy deal as the pivotal moment to shift FuelCell’s investment thesis from speculative to executable. The 380 MW agreement includes an initial deployment of 30 MW backed by an immediate non-refundable deposit, implying an approx. $90 million in near-term revenue at $3,000 per kilowatt per ITC, marking FuelCell’s first tangible pipeline conversion into a contracted backlog.

Dumoulin Smith pointed out that FuelCell trades at 8x its estimated EV/EBITDA, a steep discount to its peers, Bloom Energy (BE), which trades at 19x multiple. This allows investors to own a share in the data center power market at a fraction of peer valuations. Now combines with a 5 GW pipeline conversion and 500 MW Torrington expansion, Jefferies sees a clear pathway to continued backlog conversion ahead.

Should You Buy FCEL?

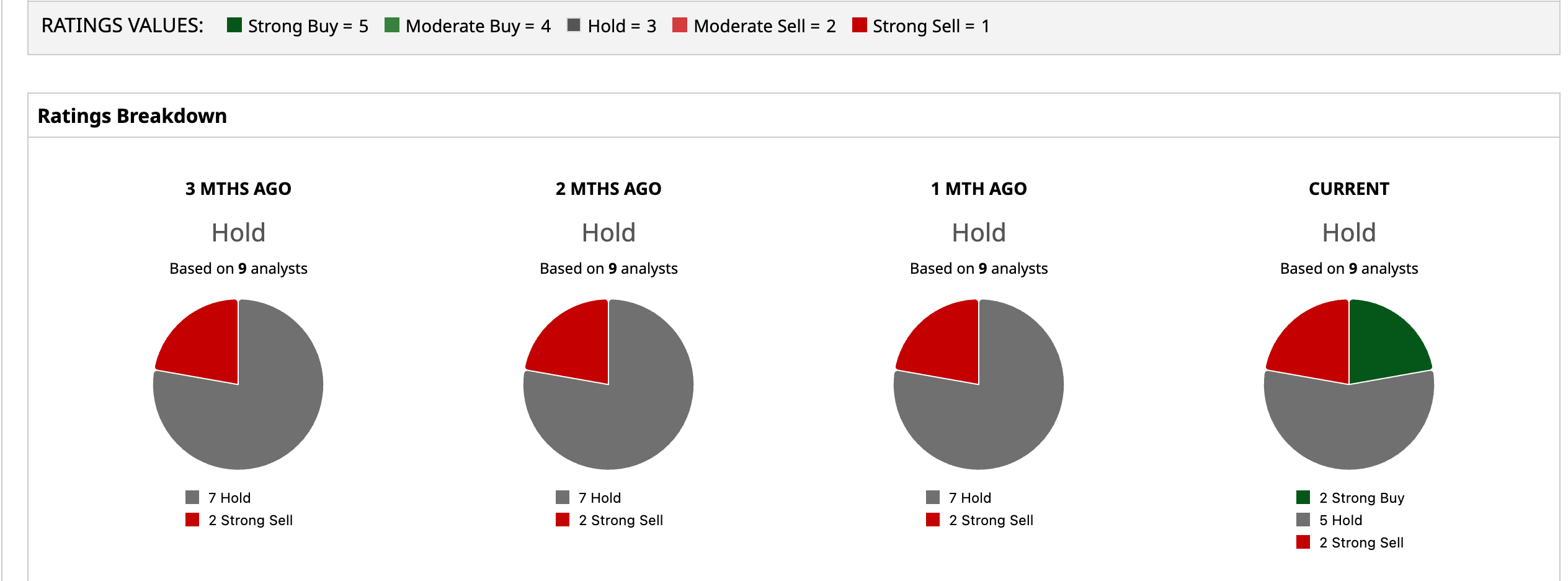

With Jefferies upgrade and $24 price target marking FuelCell’s first tangible pipeline conversion to contracted backlog, the bull case for FCEL is gaining solid institutional backing for the first time. However, Wall Street remains cautious with a consensus “Hold” rating on nine analyst ratings, comprising two “Strong Buy” ratings, five “Hold” ratings, and two “Strong Sell” ratings with a mean price of $17.18, implying a downside of 42.8% from current market levels.

For high-risk appetite investors, FCEL’s 5 GW pipeline and AI data center power positioning offer asymmetric upside, but pre-profitability status combined with a divided analyst community demands a cautious approach on the stock.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)