/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Wells Fargo analyst Aaron Rakers raised his price target on Advanced Micro Devices (AMD) stock to $615 on Tuesday, June 30, maintaining an “Overweight” rating on the chipmaker.

The new target implies roughly 14% upside from recent trading levels, making it one of the more bullish positions among Wall Street analysts covering the stock.

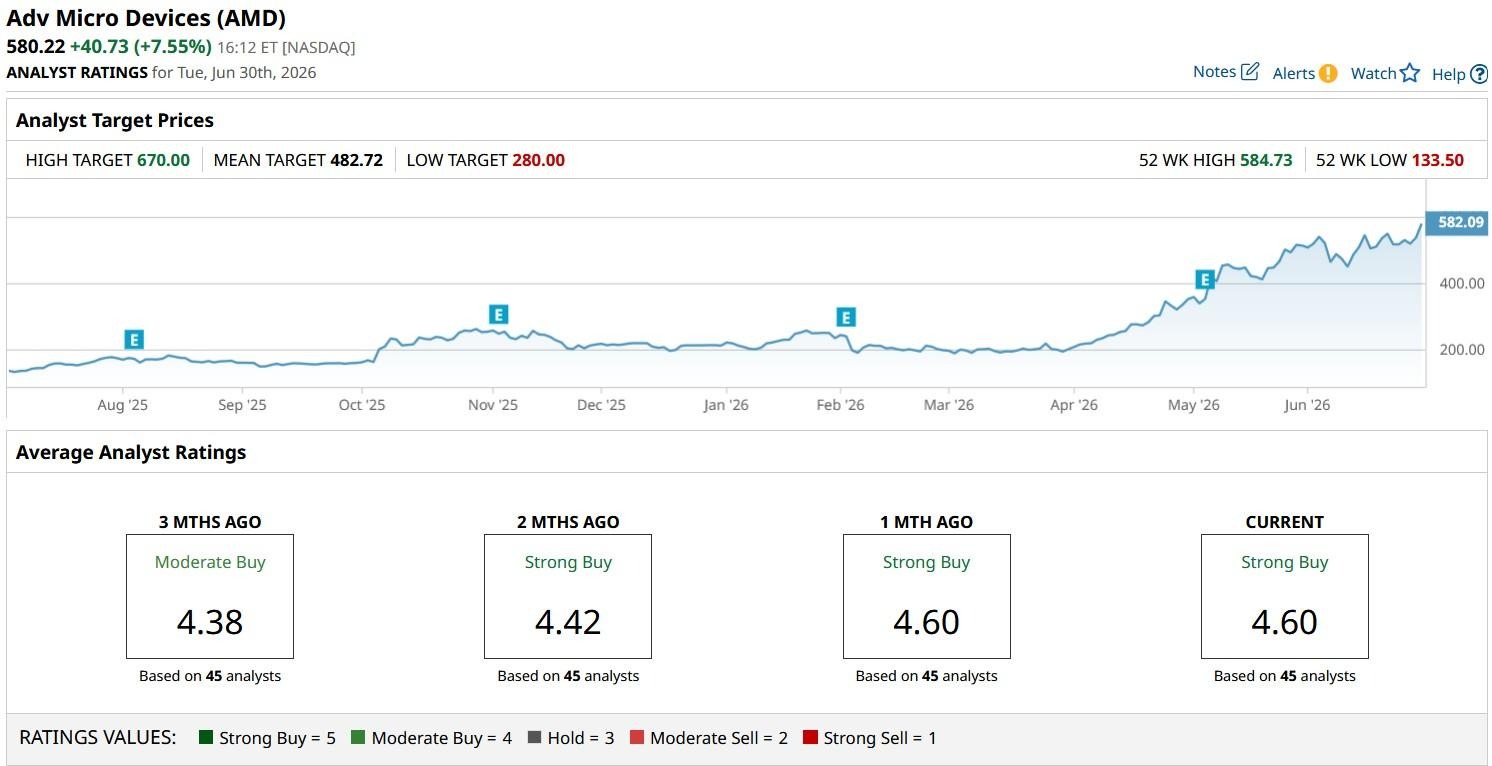

AMD shares responded positively, gaining nearly 8% today, and are now up an overall 170% year-to-date.

Why Does Wells Fargo Remain Bullish on AMD Stock?

The core thesis behind the price target increase centers on AMD’s growing role in AI infrastructure, particularly as the industry transitions from AI model training toward AI inference workloads.

Rakers expects this shift toward running AI applications in real-world environments to materially increase demand for AMD’s high-core-count EPYC server CPUs alongside its Instinct AI-focused GPUs, allowing the company to compete more aggressively with Nvidia.

The analyst sees AMD’s server CPU business generating some $16 billion in revenue this year, representing a 68% year-over-year increase, followed by growth to $20.5 billion in 2027 and $25 billion in 2028.

What Rakers Expect From AMD’s GPU Business

On the GPU side, Rakers forecasts data center GPU revenue of $15.6 billion in 2026, growing to $40.6 billion next year and nearly $63 billion in 2028, reflecting accelerating adoption of artificial intelligence computing hardware across cloud providers and enterprises.

These projections underpin his earnings estimates of $13.40 per share in 2027, roughly 3% above Wall Street consensus, and $18.75 per share in 2028, about 8% above consensus.

He further believes AMD has the potential to approach $20 per share in peak earnings, a level that could be reached earlier than the company itself has guided.

What Else Could Drive AMD Shares Higher?

A key product cycle catalyst supporting the bull case is AMD’s next-generation 2nm EPYC Venice chips, which entered production in late May 2026 with volume shipments expected in the second half of the year.

Customer validation and ramp activity for Venice is reportedly running ahead of any prior EPYC generation, signaling strong market pull.

Pricing strength is also contributing to the outlook, as buyers increasingly opt for “more powerful” EPYC variants that carry better margins for AMD.

Other Wall Street Analysts Disagree with Rakers on AMD

However, the upgrade comes with important caveats regarding valuation and competition. AMD shares currently trade at about 85x forward earnings, making it roughly four times more expensive than Nvidia (NVDA).

NVDA continues to dominate the AI accelerator market and is expanding into the CPU business through its Vera platform, meaning that AMD must execute successfully across both processor and graphics segments to gain meaningful market share.

That’s partly why other Wall Street analysts believe AMD is trading at a stretched valuation at the time of writing.

While the consensus rating on Advanced Micro Devices remains at “Strong Buy,” the mean price target of $483 signals significant potential downside from current levels.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)