/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

Apple (AAPL) was back in the spotlight on Monday after Loop Capital reiterated its "Buy" rating due to a report disclosing that the company was seeking deeper relations with Chinese suppliers in the supply chain. Specifically, Apple has lobbied U.S. authorities to approve the purchase of DRAM chips from Chinese memory maker ChangXin Memory Technologies (CXMT). If approved, the deal will help reduce hardware costs in the long term.

The news comes at a time when memory prices are a significant cost factor in the consumer electronics industry. Over the last 12 months, the memory prices have soared because of AI infrastructure investments that made the supply tight and forced Apple to raise the prices for several products, including the new MacBook Neo. If the company can find an additional memory provider, investors will be able to see a better supply situation and, consequently, a larger hardware margin.

About Apple Stock

Apple is the largest consumer electronics company in the world, offering smartphones, personal computers, tablets, wearable gadgets, and digital services. Founded in California and based in Cupertino, Apple currently has a market capitalization of nearly $4.17 trillion, making it the world's most valuable publicly traded company.

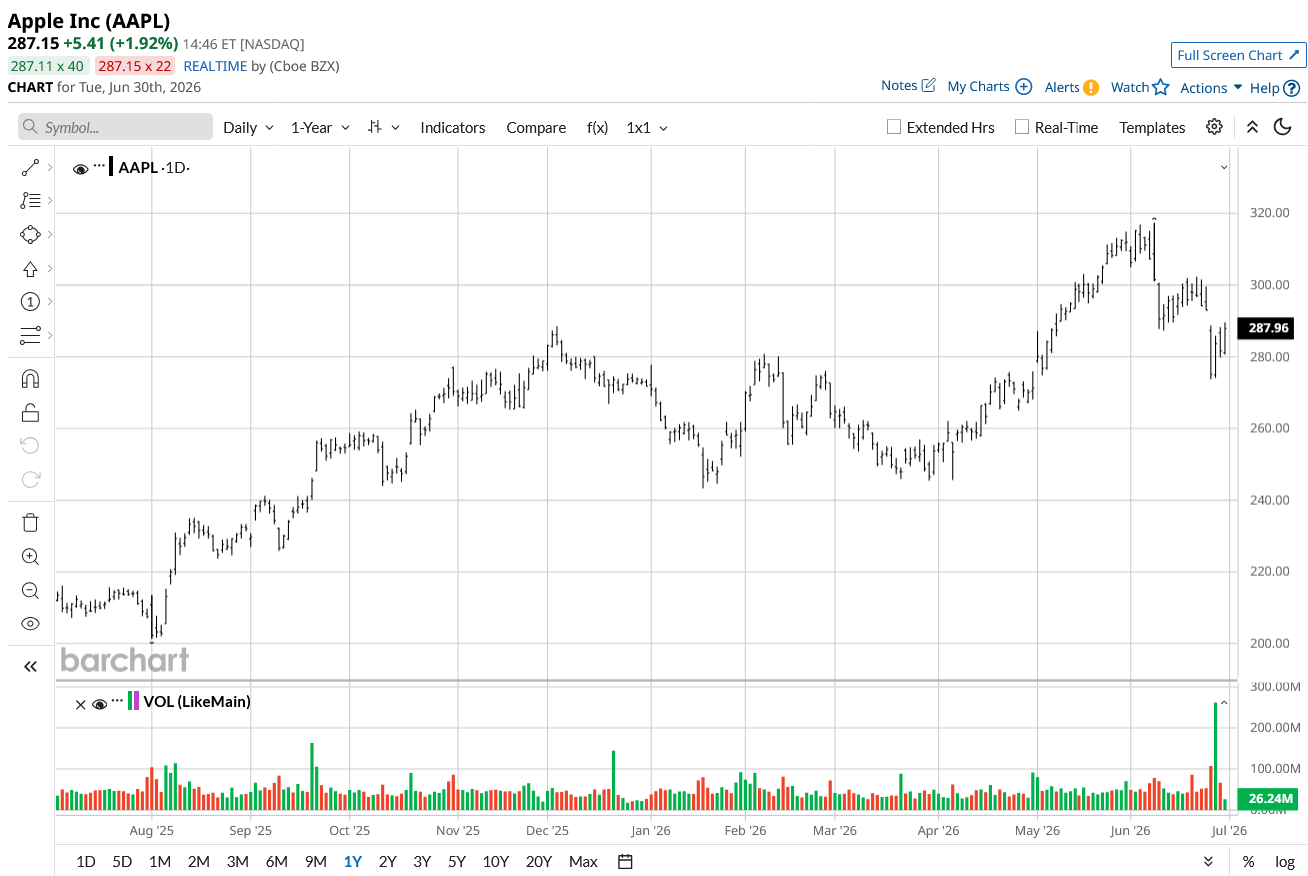

AAPL stock gained more than 43% since its 52-week low of $199.26 but still lagged its all-time high of $317.40 by around 11%. Although the stock declined 2% over the past week, it continues to outperform the broader market in the longer term due to solid earnings growth, increasing revenue from Services, and capital allocation through share buybacks.

As far as valuation is concerned, Apple continues trading at a premium. The stock trades at roughly 33x forward earnings and at about 10x sales. These multiples are above most of the hardware competitors, which speaks volumes about investors' readiness to pay a premium for Apple's recurring ecosystem revenue, profitability, and huge installed base. Although the valuation is far from being attractive, consistent earnings growth and leading returns on invested capital have historically justified the premium.

Apple continues paying dividends regularly. Recently, the company raised its quarterly payout by 4% to $0.27 per share and authorized another $100 billion share buyback program.

Apple Beats on Earnings

In the last reported quarter, Apple managed to post yet another excellent earnings release. Revenue rose 17% year-over-year (YoY) to a record March-quarter level of $111.2 billion, while diluted EPS jumped 22% to $2.01 and exceeded consensus estimates.

Management mentioned double-digit growth in each geographic region. Record iPhone revenue came due to robust iPhone 17 line sales, while the Services sector recorded its best-ever revenue. They also noted healthy uptake of the newly released products, including the iPhone 17e, MacBook Neo, and M4 iPad Air.

The latest news related to China memory may be an interesting story in the long term. Traditionally, Apple used memory suppliers like Micron (MU), Samsung Electronics, and SK Hynix. An additional provider will give Apple more procurement flexibility while lowering the cost of components if the manufacturers from China become more competitive. Nevertheless, investors need to understand that there is a significant geopolitical risk. CXMT was recently included in the Pentagon's blacklist because of its military connections. It means that in case of any future procurements, Apple will face significant political pressure and reputational risks.

Overall, the lobbying effort of the company looks more like a strategic option than some operational change. Previously, Apple tried to source memory from Chinese YMTC and then abandoned this plan because of the political resistance. Whether this effort will come true or not will depend largely on the situation between the USA and China.

What Do Analysts Expect for AAPL Stock?

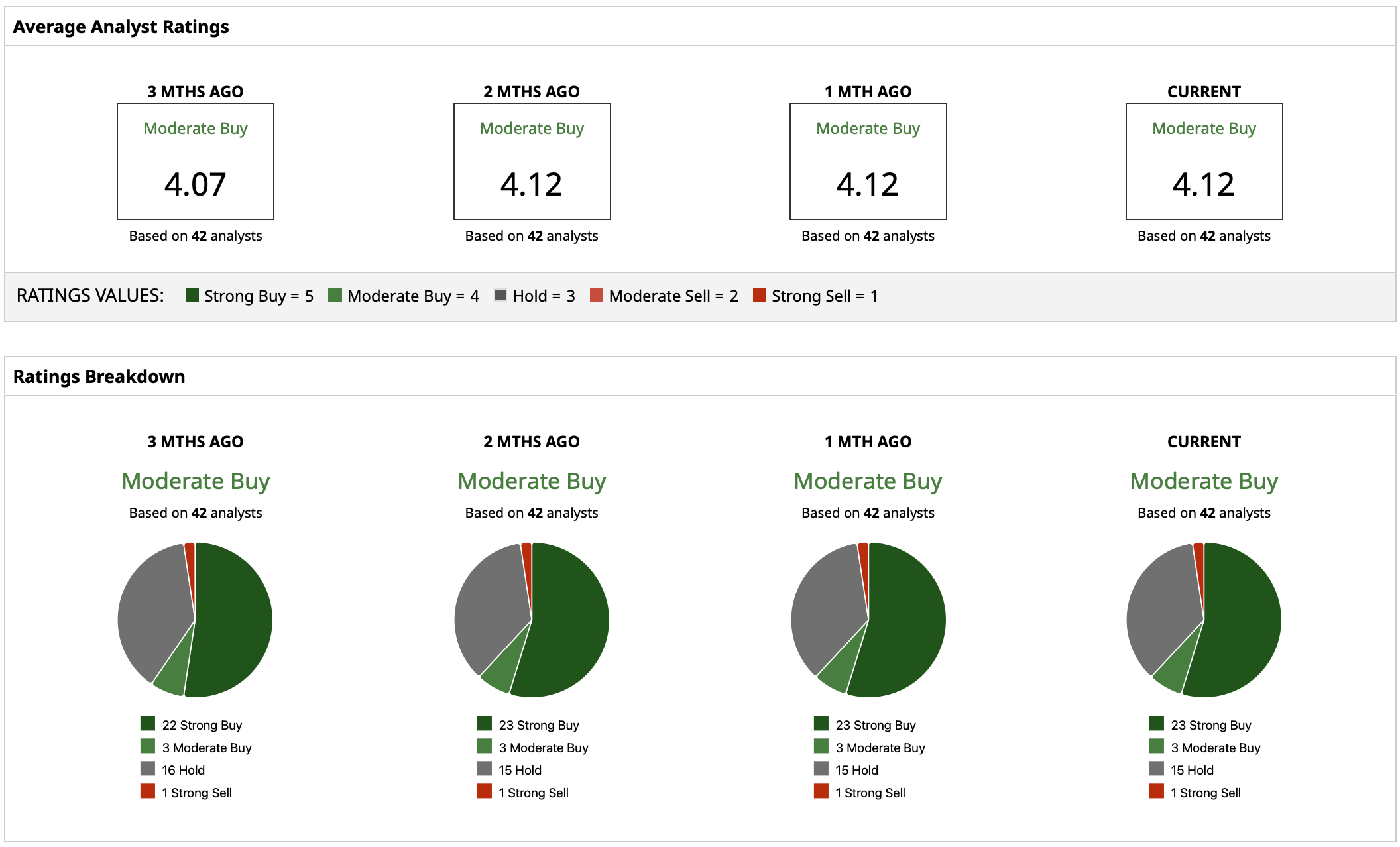

Despite its premium valuation, analysts remain quite positive towards AAPL stock, assigning a “Moderate Buy” rating consensus. They regard the company as one of the highest-quality technology names in large caps because of its unmatched ecosystem, recurring revenue from Services, and exceptional cash generation ability. Thus, Loop Capital's latest reaffirmation of its “Buy” rating is explained by the assumption that the efforts of Apple to diversify its supply chain will lead to profitability improvement over time.

Currently, the average analyst price target for AAPL stock is $314.40. This target implies 10% upside potential from the current stock price of $287. The most optimistic target is $400, while the lowest is $235. It means that although the analysts are quite positive about Apple, they do not share the same opinions about potential upside after multiyear gains of the company.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)