/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

For Micron Technology (MU) stock investors, July 10 could become a key date to watch as a major shift in the global memory chip landscape arrives on Wall Street. South Korean semiconductor giant SK Hynix is preparing to begin trading in the U.S. market through a Nasdaq ADR listing and raise up to 45.45 trillion won ($29.43 billion), giving American investors direct access to one of Micron’s biggest rivals in the booming artificial-intelligence (AI) memory market.

SK Hynix is one of the world’s largest memory semiconductor companies, specializing in DRAM, NAND flash memory, and high-bandwidth memory (HBM), the advanced memory technology that has become a critical component for AI systems and data center GPUs.

SK Hynix’s growth has been closely tied to rising demand for AI accelerators, cloud data centers, and large-scale AI model training, putting it in direct competition with Micron Technology in the memory market.

The move comes at a critical time for Micron Technology, which has benefited from surging demand for HBM chips powering AI data centers. Micron recently highlighted strong demand momentum, record financial performance, and continued investment in expanding its manufacturing footprint as AI infrastructure spending accelerates. However, SK Hynix’s U.S. debut could reshape investor sentiment by giving Wall Street a new way to compare two of the world’s leading memory chip suppliers head-to-head.

Investors are left wondering whether capital will rotate toward SK Hynix as a fresh AI semiconductor play, or whether Micron’s strong AI exposure and improving earnings power will keep it the preferred memory stock. As July 10 approaches, investors will need to decide whether to buy the competition, stay with Micron, or position for a broader AI chip boom.

About Micron Technology Stock

Micron Technology is a semiconductor company that designs, develops, manufactures and sells memory and storage products globally, including DRAM, NAND flash memory, HBM, solid-state drives (SSDs) and other memory modules. Headquartered in Boise, Idaho, Micron operates multiple business units serving cloud/data center, mobile and client, automotive/embedded, and enterprise segments worldwide. Micron has reached $1.29 trillion market cap, putting it among the largest and most valuable players in the global semiconductor industry.

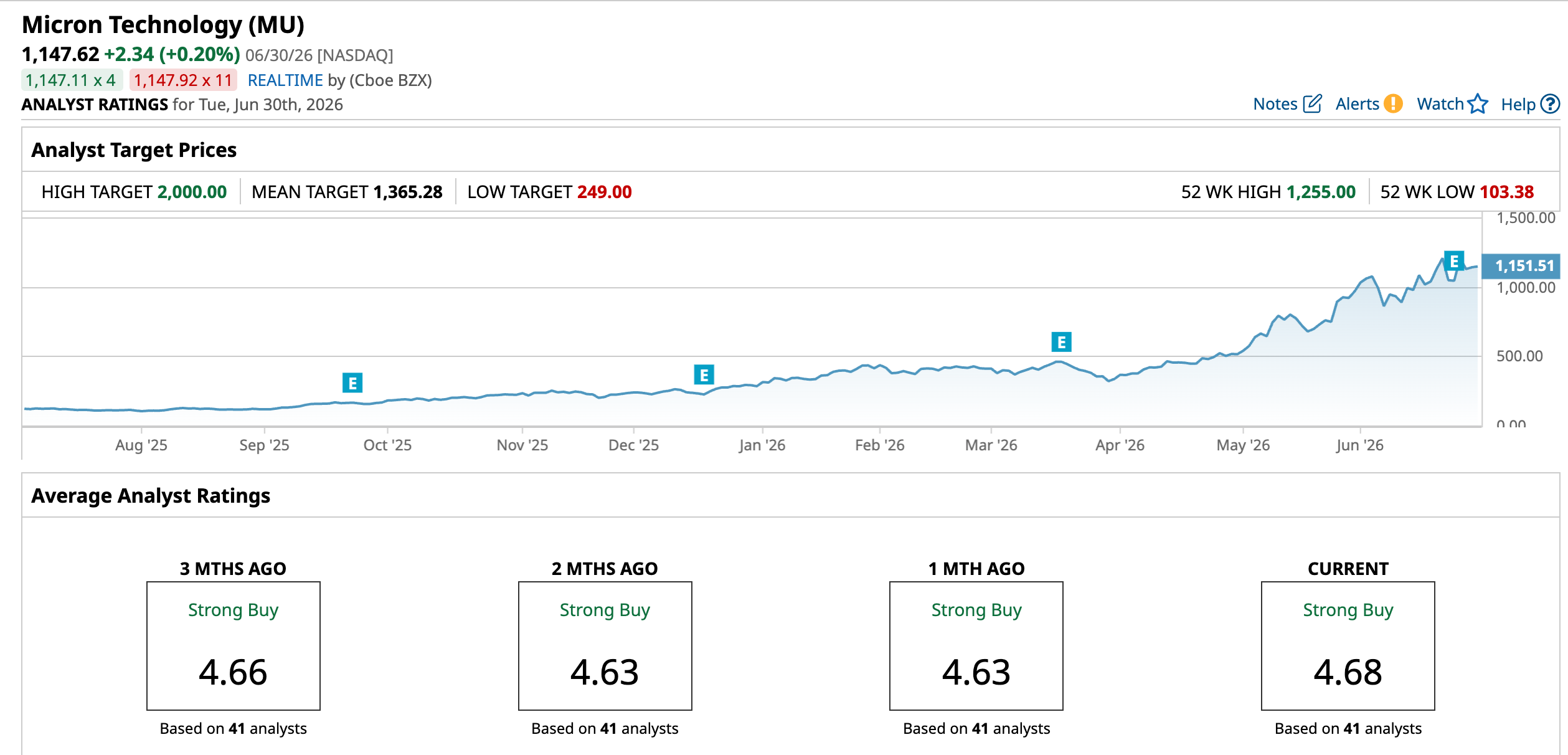

Driven by surging demand for HBM, data center expansion, and improving memory pricing conditions, Micron shares have posted substantial gains. The stock has traded near record levels, with a dramatic move to a high of $1,255 on June 25, driven by a strong third-quarter earnings report that blew past Wall Street expectations.

MU has remained one of the strongest semiconductor names, with 306.32% gains year-to-date (YTD) and 841% over the past 52 weeks, reflecting investor confidence that AI-driven memory demand could support stronger earnings and pricing power.

However, the recent price action has been much more volatile. After a sharp rally and a move toward record highs, Micron shares pulled back, falling 6.7% on June 26, only to rise by 1.14% in the following session. The stock is up 10.26% over the past five days.

The pullback does not necessarily signal a breakdown in Micron’s long-term story. Instead, investors appear to be balancing strong fundamentals against rising uncertainty, including increased competition from memory rivals such as SK Hynix.

However, the stock still seems to be trading at a discount compared to industry peers at 18.40 times forward price-to-earnings.

Blockbuster Q3 Results

Micron Technology delivered a solid third-quarter fiscal 2026 report on June 24, reinforcing the company’s position as one of the biggest beneficiaries of the artificial intelligence memory boom.

Micron reported record quarterly revenue of $41.5 billion, up from $9.3 billion in the same quarter a year ago, representing year-over-year (YOY) growth of 345.8%. Revenue also jumped from $23.9 billion in fiscal Q2 2026, highlighting the strength of the current memory upcycle. The company’s earnings recovery was even more impressive, with non-GAAP EPS rising to $25.11 from $1.91 in the prior-year quarter, which was above expectations, while non-GAAP net income increased to $28.9 billion from $2.2 billion in the prior-year period.

Profit margins expanded sharply as Micron benefited from strong pricing, tight memory supply, and rising demand for AI infrastructure. Non-GAAP gross margin reached 84.9% in Q3 FY2026, compared with 39.0% a year earlier, showing the significant operating leverage created by the memory recovery. Operating cash flow also surged to $25.4 billion, compared with $4.6 billion in fiscal Q3 2025, giving Micron greater financial flexibility to invest in next-generation memory production.

The biggest growth driver remains AI. Micron has been capitalizing on demand for HBM memory used in advanced AI systems and data centers, where limited supply and accelerating AI adoption have improved pricing power across the memory industry.

Furthermore, Micron provided a strong outlook for fiscal fourth quarter 2026, expecting revenue of $50 billion (plus or minus $1 billion), non-GAAP gross margin of about 86%, and non-GAAP EPS of $31 (plus or minus $1).

Also, the consensus EPS estimate of $71.74 for fiscal 2026 reflects an increase of 834.1%, while the EPS estimate of $151.06 for fiscal 2027 indicates a 110.57% rise YOY.

What Do Analysts Expect for Micron Stock?

Although SK Hynix’s upcoming U.S. market debut has introduced a new layer of uncertainty for Micron investors, Wall Street sentiment toward Micron remains broadly positive as analysts continue to raise their price targets, reflecting confidence in the company’s AI-driven growth opportunity.

This month, DA Davidson raised its price target on Micron Technology to a Street high of $2,000 from $1,500 while maintaining a “Buy” rating, citing improved visibility in the semiconductor cycle and strong AI-driven memory demand.

Also, Rosenblatt raised its Micron Technology price target to $1,500 from $1,200 while keeping a “Buy” rating, citing strong earnings, improving margins, and sustained AI-driven memory demand. The firm highlighted Micron’s expanding gross margins, expected to reach about 86%, and noted that DRAM and NAND supply constraints could continue through 2027.

Plus, Needham raised its Micron Technology price target to $1,650 from $1,550 while maintaining a “Buy” rating.

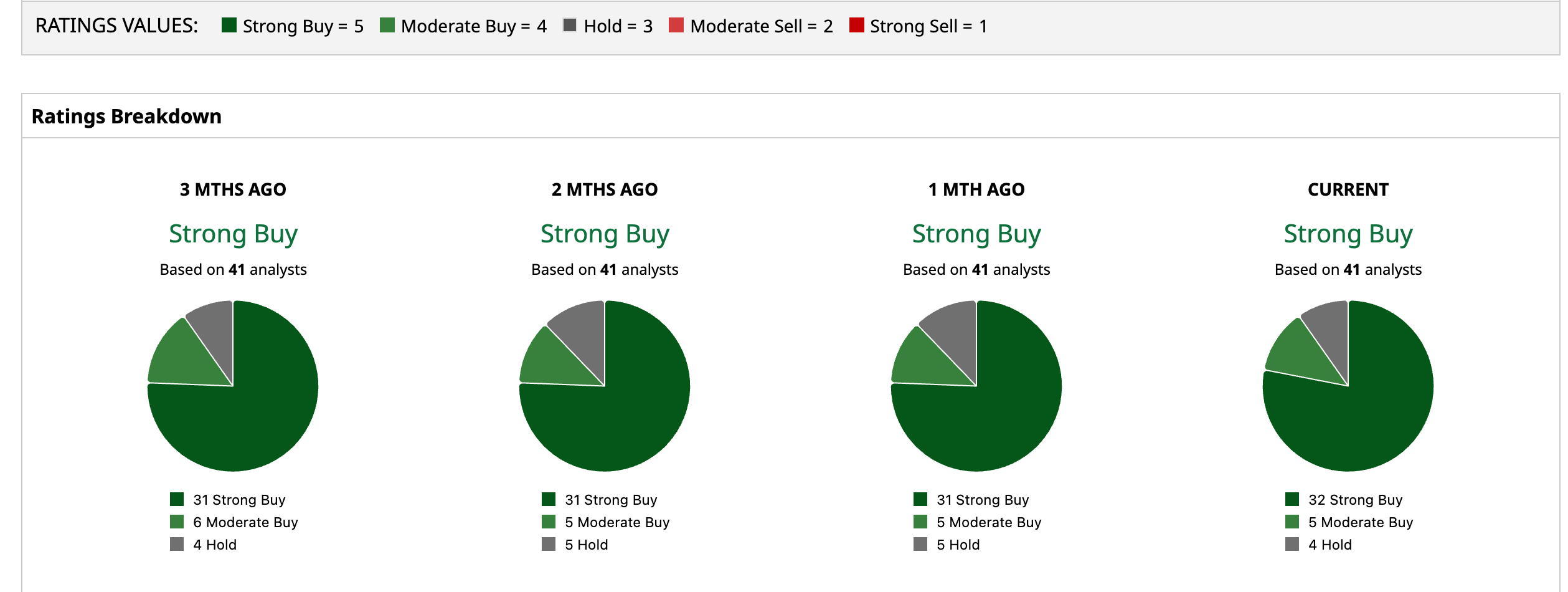

Overall, MU has a consensus “Strong Buy” rating. Of the 41 analysts covering the stock, 32 advise a “Strong Buy,” five suggest a “Moderate Buy,” and four analysts are on the sidelines, giving it a “Hold” rating.

While the average analyst price target of $1,365.28 suggests an upside of 19.1%, DA Davidson’s Street-high target price of $2,000 suggests that the stock could rally as much as 74.5%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)