/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

The artificial intelligence (AI) revolution has turned Nvidia Corporation (NVDA) into one of the most closely watched stocks on Wall Street, but the market leader now finds itself in an unusual position, delivering massive AI growth while its stock performance struggles to reflect that momentum.

Wedbush Securities describes the recent sell-off in major AI and tech stocks, including Nvidia, as a “Twilight Zone” scenario where strong long-term fundamentals are being overshadowed by short-term investor concerns. The firm believes the market is currently in an “air pocket stage” as companies invest heavily in AI infrastructure, with roughly $700 billion in Big Tech capital spending focused on AI buildouts while investors wait for clear monetization.

Wedbush argues that concerns over rising compute costs, memory pricing, and heavy AI spending are temporary and that the long-term expansion of AI applications will ultimately justify these investments. Wedbush Securities points to continued AI infrastructure demand and suggests that Nvidia’s growth potential remains far greater than what the current stock price implies.

The firm sees the current weakness as creating opportunities to own NVDA before the next phase of growth accelerates.

About Nvidia Stock

Nvidia is a global leader in accelerated computing and AI, renowned for pioneering the GPU that revolutionized gaming, data centers, and AI-driven computing. Headquartered in Santa Clara, California, Nvidia’s technology now powers everything from high-performance gaming and cloud computing to autonomous vehicles and generative AI applications. With a market cap of $4.7 trillion, Nvidia stands among the world’s most valuable companies, driven by its dominance in AI infrastructure and continued innovation in next-generation chip design.

Nvidia has been one of the greatest stock market success stories of the past decade, transforming from a leading graphics chip company into the backbone of the AI revolution. The stock’s long-term performance reflects this massive shift, delivering extraordinary gains as demand for GPUs, data centers, and AI infrastructure accelerated. Over the past five years, Nvidia shares have generated returns of 872.4%, while long-term investors have benefited from the company’s rapid earnings growth and dominant position in AI computing. The stock is also up 25.56% over the past year.

However, Nvidia’s stock has recently entered a period of volatility as concerns over AI infrastructure spending and valuation weighed on sentiment, with a 6.1% slump over the past month.

The recent sell-off does not necessarily reflect weakening fundamentals. Nvidia remains at the center of the AI ecosystem, with demand for its advanced chips continuing to support strong revenue and earnings growth.

Nvidia trades at 22.15 times forward earnings, which is currently a discount compared to industry peers and the historical average.

Solid Quarterly Performance

Nvidia delivered another blockbuster quarter with its most recent financial results for the first quarter of fiscal 2027 on May 20, 2026, reinforcing the company’s dominance in the rapidly expanding artificial intelligence infrastructure market. Strong demand for AI accelerators, networking products, and next-generation Blackwell systems helped Nvidia post record revenue and earnings while continuing to outperform Wall Street expectations.

For the quarter ended Apr. 26, 2026, Nvidia reported record revenue of $81.6 billion, up 85% year-over-year (YOY). Its net income surged 211% YOY to $58.3 billion. On a non-GAAP basis, earnings per share (EPS) increased 140% from the prior-year quarter to $1.87, ahead of expectations. Non-GAAP gross margin expanded sharply to 75%, compared to 60.8% in the same period last year, highlighting Nvidia’s continued pricing power and favorable AI product mix.

The Data Center business remained Nvidia’s primary growth engine, as its revenue climbed 92% YOY to a record $75.2 billion as hyperscalers, enterprises, and sovereign AI projects accelerated spending on AI factories and large-scale computing clusters. Further, Nvidia reported networking revenue of $14.8 billion, up 199% YOY. Meanwhile, Edge Computing revenue rose 29% YOY to $6.4 billion, supported by growth in gaming GPUs, autonomous driving platforms, robotics, and AI-enabled edge devices.

Management highlighted the rapid adoption of Blackwell systems and emphasized growing opportunities in agentic AI and enterprise AI infrastructure. CEO Jensen Huang described the current AI infrastructure buildout as “the largest infrastructure expansion in human history,” while also unveiling the new Vera Rubin platform and additional AI software and networking technologies aimed at expanding Nvidia’s ecosystem.

Furthermore, Nvidia provided extremely strong guidance for the second quarter of fiscal 2027. The company expects revenue of $91 billion, plus or minus 2%. Nvidia also guided for a non-GAAP gross margin of around 75%. Notably, management stated that the outlook assumes no contribution from China Data Center compute revenue, reflecting ongoing U.S. export restrictions.

Analysts tracking Nvidia project the company’s EPS to climb 90.2% YOY to $8.69 in fiscal 2027 and grow another 34.3% to $11.67 in fiscal 2028.

What Do Analysts Expect for Nvidia Stock?

This month, Morgan Stanley reaffirmed its “Overweight” rating on Nvidia and kept its $288 price target, naming the chipmaker as its preferred pick within the processor industry. The firm highlighted Nvidia’s leadership across several key product categories and noted that the company continues to present one of the most attractive value opportunities in the semiconductor space.

Meanwhile, Truist Securities maintained its “Buy” rating on Nvidia with a $307 price target following the company’s announcement of multiple new AI-focused products at GTC Taipei, reinforcing confidence in Nvidia’s continued role as a leader in the AI infrastructure market.

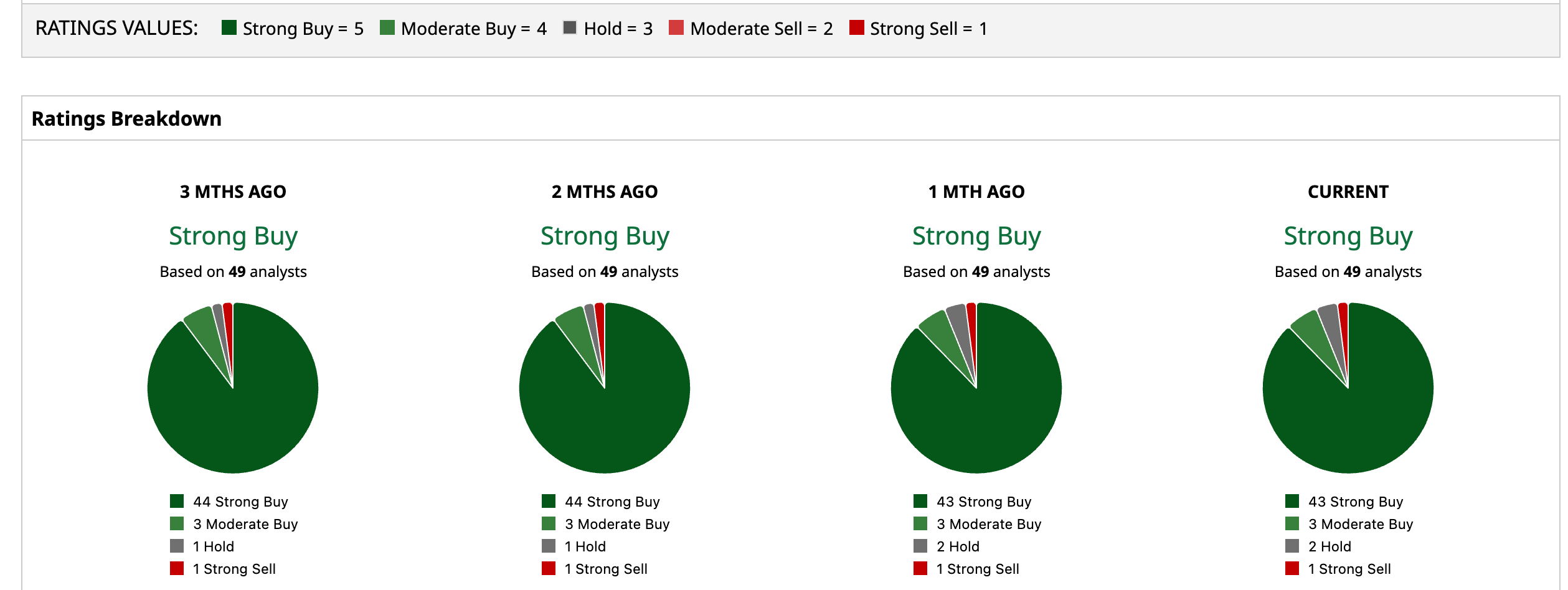

Wall Street’s bullishness is evident in NVDA having a consensus “Strong Buy” rating. Of the 49 analysts covering the stock, 43 advise a “Strong Buy,” three suggest a “Moderate Buy,” two analysts give it a “Hold” rating, and one offers a “Strong Sell” rating.

The average analyst price target for NVDA is $301.92, indicating a potential upside of 52.2%. Also, the Street-high target price of $500 suggests that the stock could rally as much as 152.1%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)