Verizon Communications (VZ) recently disclosed financial details of its new 50/50 international joint venture with BT Group, a partnership designed to combine the overseas enterprise operations of both telecom giants.

In a regulatory filing, the company estimated at least a $700 million second-quarter loss stemming from the reclassification of assets as “held-for-sale” in connection with the joint venture structure.

Additionally, VZ flagged up to $450 million in severance charges and about $250 million in asset-rationalization costs related to the deal.

Versus its year-to-date high, Verizon stock is down about 17% at the time of writing.

Is the BT Partnership Bullish for Verizon Stock?

The joint venture aims to allow both Verizon and BT Group to benefit from greater scale and the ability to leverage each other’s network infrastructure in international markets.

The strategic rationale centers on streamlining overseas operations, where neither firm individually commands the same dominance they hold domestically.

Verizon reportedly paid about $625 million for its stake in the venture with BT Group subsidiaries, signaling a meaningful capital commitment to the international enterprise segment.

Why Near-Term Charges Aren’t Bearish for VZ Shares

Investors must understand that the disclosed losses are primarily non-cash accounting reclassifications tied to the strategic restructuring, rather than an indication of deteriorating core business fundamentals.

This distinction has been somewhat lost in the market reaction, which was compounded by Verizon’s simultaneous removal from the Dow Jones Industrial Average ($DOWI) and replacement by Alphabet (GOOG) (GOOGL).

VZ shares slipped over 5% on the day these developments were announced, a notably large move for a company that has experienced only two moves greater than 5% over the past year.

How BT Shares Responded to the Verizon Deal

The partnership was positively received in London, where BT shares rose about 1.4% on the news.

Market participants in the UK are evaluating the “long-term benefits” of the collaboration despite acknowledging short-term restructuring costs.

The deal positions both firms to compete more fiercely in the global enterprise connectivity market where hyperscale cloud providers and satellite-based competitors like Starlink are intensifying competitive pressure.

How to Play Verizon at Current Levels?

Despite the near-term charges, Verizon’s fundamental outlook remains relatively intact.

The company recently raised its fiscal 2026 earnings per share (EPS) guidance to $4.95 to $4.99, beat expectations in Q1, and maintains a dividend yield of 6.42%.

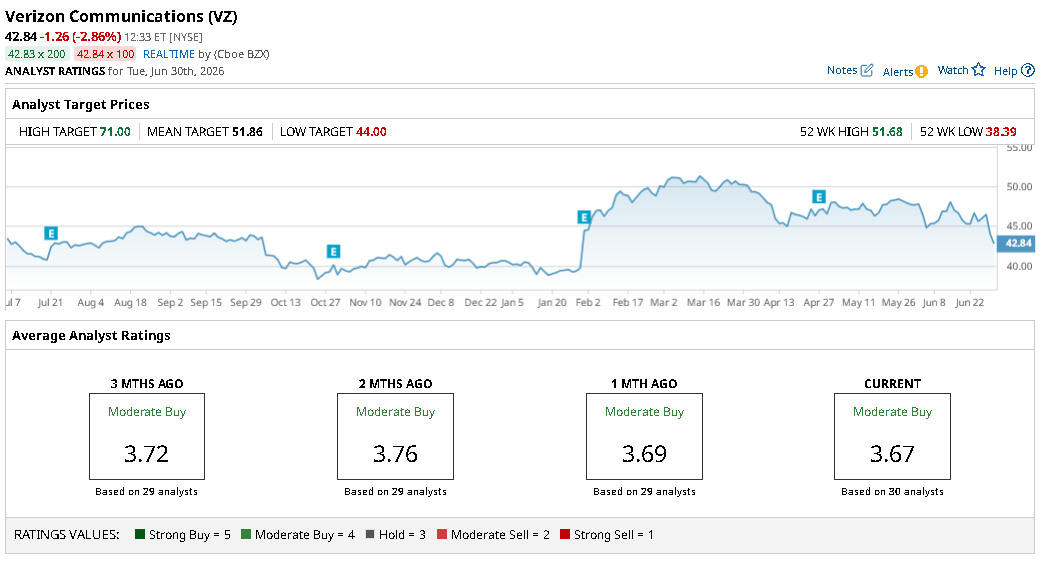

Investors should also take heart in the fact that Wall Street analysts continue to rate Verizon shares at “Moderate Buy,” with the mean price target of nearly $52 indicating potential upside of roughly 17% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)