/Apple%20store%20and%20shoppers%20-%20by%20PhillDanze%20via%20iStock.jpg)

Tech leader Apple (AAPL) has implemented sweeping price increases across its MacBook and iPad product lines. CEO Tim Cook has stated that these increases were unavoidable as memory and storage costs continue to rise. According to Counterpoint Research, these costs have quadrupled in the past three quarters, as suppliers seek these components for AI servers. Apple often raises average selling prices by dropping the cheapest option, starting at higher storage levels, or pushing buyers toward Pro models.

While the market reasonably did not react favorably to the news, Morgan Stanley analysts still believe that Apple is well-positioned to weather this storm. Analyst Erik Woodring believes that this move is implemented to protect the company’s enviable gross margins. Woodring believes that if Apple’s demand remains inelastic, as history would suggest, these hikes could be an upside for both revenue and earnings. Therefore, although the move has spooked investors, it might reward the company in the longer term.

About Apple Stock

Apple designs and sells consumer devices, software, and digital services, with products like the iPhone, Mac, iPad, and wearables at the center of its business. The company is also pushing harder into AI, with Apple Intelligence expanding and new Siri features being tested, while Apple has reshaped parts of its AI strategy and leadership.

Recent moves show Apple using AI to improve its products and internal operations, alongside continued work on its hardware-and-services model. Headquartered in Cupertino, California, Apple is one of the most valuable companies in the world, commanding a $4.17 trillion market capitalization.

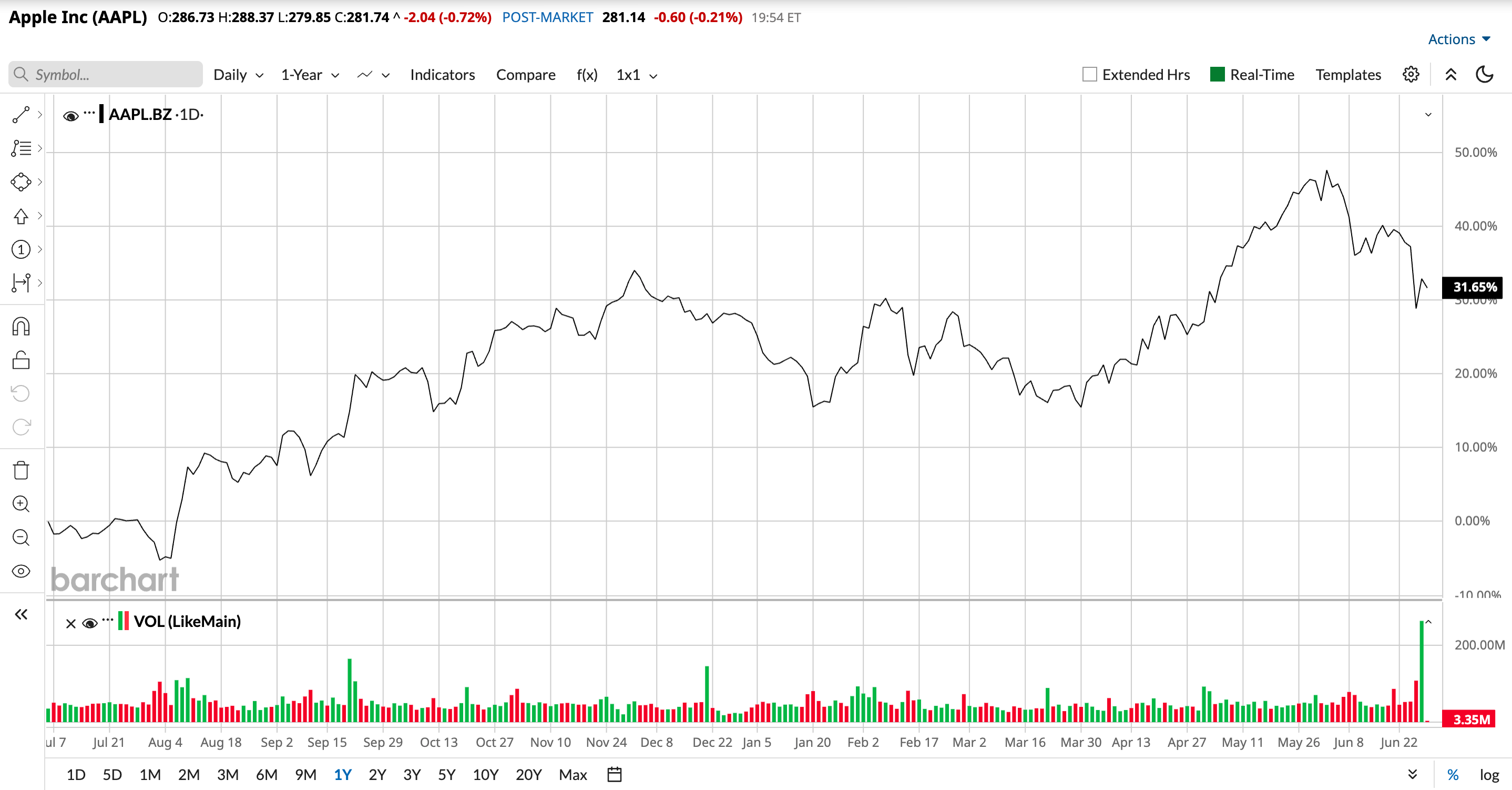

Over the past 52 weeks, Apple’s stock has gained 40.1%, while it has gained 3.63% year-to-date (YTD). Apple’s stock has risen over the past year as investors have rewarded strong revenue growth, especially in iPhone and Services, and the company’s continued AI rollout.

Even though the stock has shown some volatility of late, the market has been more focused on Apple’s earnings power, product cycle, and AI-driven upgrade potential. The company’s shares reached a 52-week high of $317.40 on June 8, but are down 11.24% from that level.

On a forward-adjusted basis, Apple’s stock is trading at a price-to-earnings (non-GAAP) ratio of 32.42 times, which is higher than the industry average of 23.91 times.

Apple’s Q2 Results Showed Resilient Demand, Strong Services Growth, and Steady AI Progress

Fueled by a surge in demand for its iPhone 17 lineup, Apple reported its best second-quarter results (the quarter ended in March). The company’s revenue increased by 16.6% year-over-year (YOY) to $111.18 billion, exceeding the $109.48 billion expected by Wall Street analysts. The majority of this growth was driven by a 21.7% YOY surge in iPhone sales to $56.99 billion and a 16.3% growth in Services revenue to $30.98 billion.

Apple is also recognizing higher profitability as its Services business grows (because it is high-margin). The company’s EPS for the second fiscal quarter was $2.01, up 21.8% YOY, and higher than the $1.92 that Street analysts had expected.

Wall Street analysts are robustly optimistic about Apple’s future earnings. For the current fiscal year, EPS is projected to surge 17.2% annually to $8.74, followed by a 9.5% growth to $9.57 in the next fiscal year. Analysts also expect the company’s EPS to grow by 19.8% YOY to $1.88 for the third quarter of fiscal 2026.

What Analysts Think About Apple’s Stock

Recently, analysts at Evercore ISI reiterated an “Outperform” rating on Apple and maintained a $365 price target despite the price hikes across its product lineup. Analysts noted that the company’s long-term memory supply deals expired during the quarter, leading it to rely more heavily on spot market prices. They also expect Apple to wait until the September iPhone 18 Pro launch to raise prices.

On the other hand, analysts at KGI Securities downgraded the stock from “Outperform” to “Hold” and gave a $315 price target, as the price hikes were announced. In contrast, BofA Securities analyst Wamsi Mohan reaffirmed a “Buy” rating on the stock and maintained a $380 price target, noting that Apple may still be able to defend its earnings even if memory costs continue to rise, stating that the price raise was already anticipated.

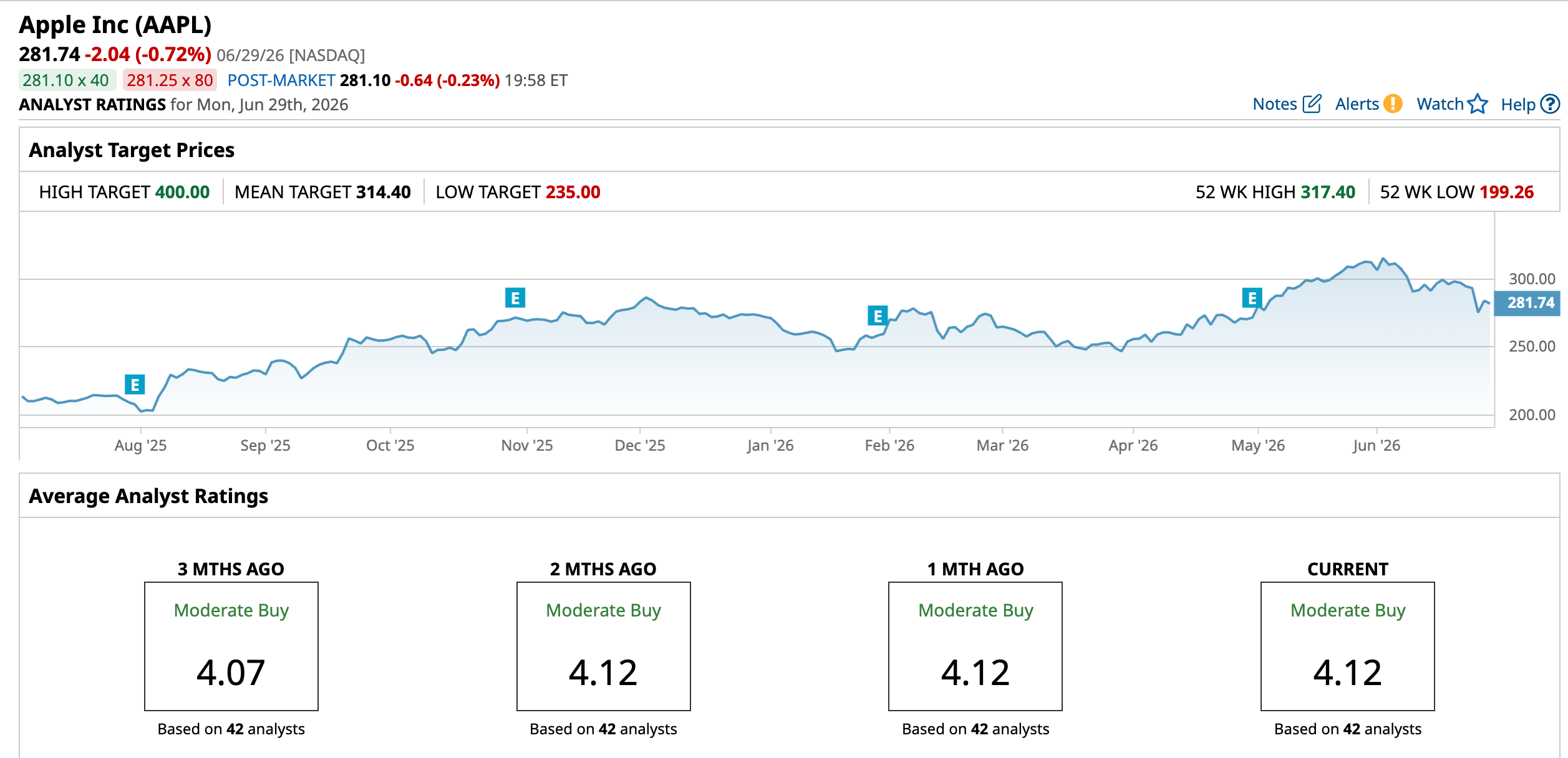

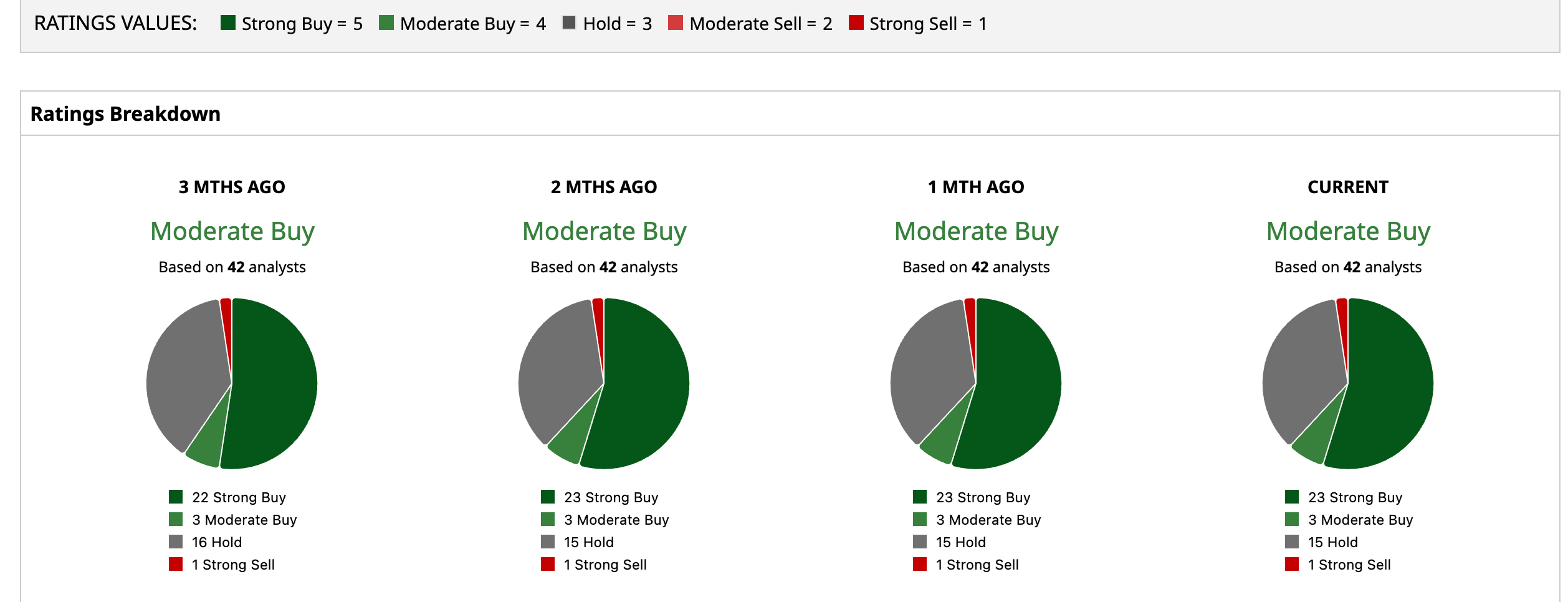

Apple has long been a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 42 analysts rating the stock, 23 have given it a “Strong Buy” rating, three a “Moderate Buy,” 15 a “Hold,” and one a “Strong Sell.” The consensus price target of $314.40 represents an 11.6% upside from current levels. Moreover, the Street-high price target of $400 implies a 42% upside for the next 12 months.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)